FICO stock has been crushed, falling more than 50% from its highs. The Daily Breakdown digs into to see what’s going on.

Before we dive in, let’s make sure you’re set to receive The Daily Breakdown each morning. To keep getting our daily insights, all you need to do is log in to your eToro account.

Deep Dive

Fair Isaac Corporation — ticker symbol “FICO” — operates in two main segments: Software, which provides decision-management solutions and the modular FICO Platform, and Scores — a concept consumers are likely more familiar with — which delivers credit-scoring products to businesses and consumer-facing scores through myFICO.com subscriptions.

The company has faced a brutal one-two punch, as AI disruption worries and increased competitive pressure have culminated in the stock’s pummeling. Shares have fallen 26% this week alone and are down more than 50% from the record high in December 2024.

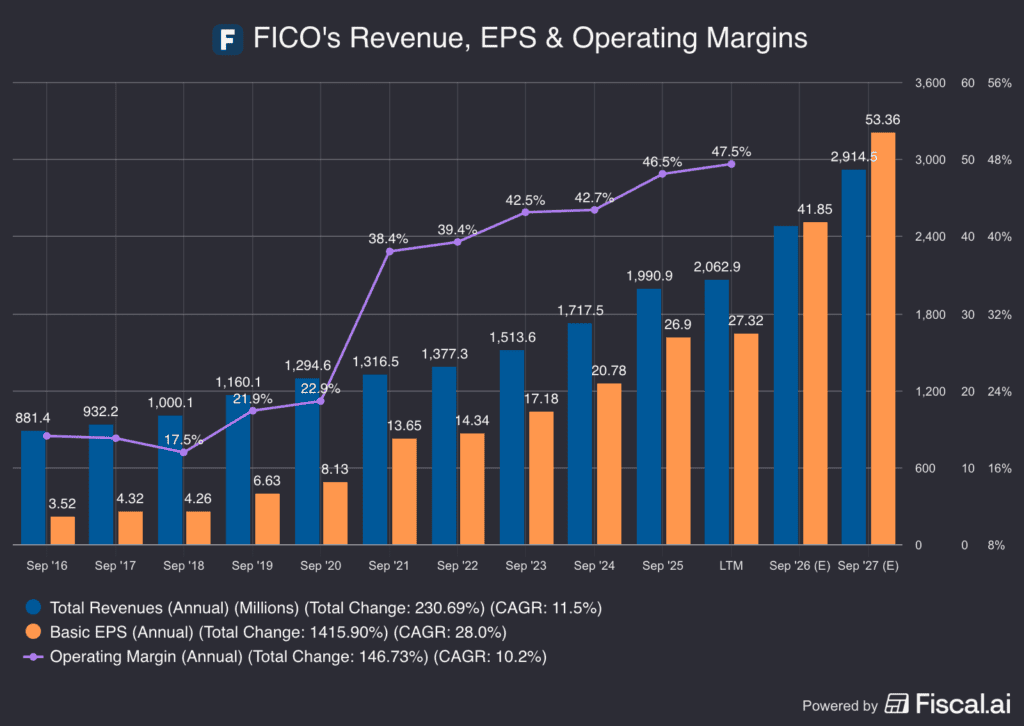

Despite the stock’s tumble, the fundamentals have been holding up:

Notice how revenue (blue) and earnings (orange) continue to trend higher, while estimates for fiscal 2026 and 2027 also point to further growth. Meanwhile, operating margins (purple) have been drifting higher over the years and have — at least so far — avoided being squeezed lower, which is a main concern amid AI disruption and competitive concerns.

Future Growth Projections

According to Bloomberg, analysts project the following:

- Earnings Growth: 40% in 2026, 26.7% in 2027, and 18.7% in 2028

- Revenue Growth: 25.5% in 2026, 16.8% in 2027, and 12.5% in 2028

Analysts currently have a consensus price target of ~$2,068 on FICO stock, implying about 87% upside to today’s stock price.

Want to receive these insights straight to your inbox?

Diving Deeper — Valuation

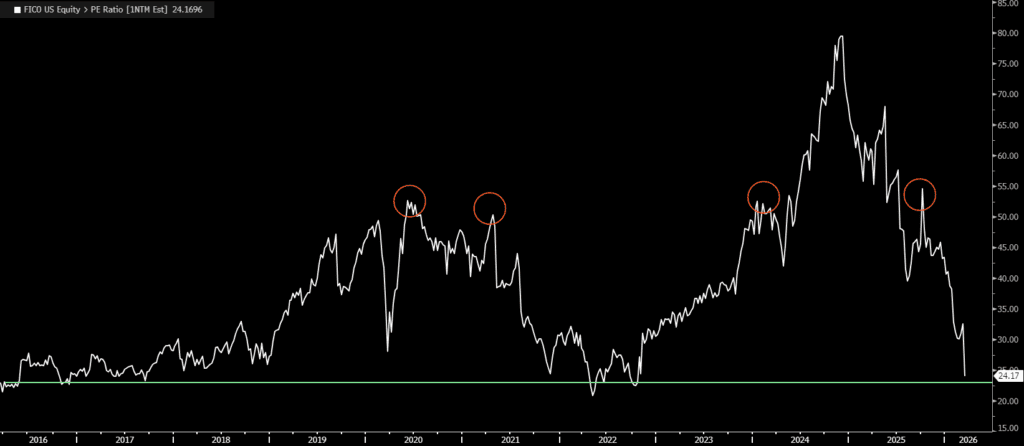

Looking at the forward price-to-earnings ratio for FICO reveals an interesting setup. When the forward P/E gets above 50, shares tend to be overvalued. However, now trading at roughly 24 times earnings, FICO stock is approaching a 10-year trough. The worry here is that the stock will suffer further valuation compression due to dampened sentiment and worries about its competitive advantage in key markets. Regardless, the valuation has come down significantly while key metrics like revenue and profit continue higher.

Risks

One of FICO’s key risks involves rising competitive and pricing pressure in mortgage credit scores, where FHFA’s “lender choice” framework opens the door for loans delivered to Fannie/Freddie to use either a Classic FICO model or VantageScore 4.0, increasing the risk of share loss and/or price concessions. This is a key business for Fair Isaac.

AI is another swing factor: it can strengthen Fair Isaac’s decisioning software, but it also lowers barriers for rivals to build “good enough” underwriting and fraud tools, potentially compressing differentiation and pricing over time. Even if fundamentals stay solid, investor sentiment could remain depressed if markets view mortgage competition as structural and AI as accelerating commoditization until FICO proves it can defend pricing and sustain share while monetizing AI-led upgrades. Beyond that, Fair Isaac faces the same market-wide, economic-related risks as many other sectors and industries.

The Bottom Line

Fair Isaac looks like a classic battle between solid fundamentals and weak sentiment — though that sentiment has soured for good reason. While the business is still growing, the valuation has reset sharply. That brings both opportunity and risk, as the stock now more accurately accounts for current risks, but could be vulnerable to further valuation compression until the company shows it can navigate mortgage competition, defend its edge against AI-driven disruption, and keep growth on track.

Disclaimer:

Please note that due to market volatility, some of the prices may have already been reached and scenarios played out.