The Daily Breakdown takes a closer look at Domino’s Pizza, as it valuation cools but even as the company cooks up growth.

Interested in more Deep Dive content? Check out our latest research.

Deep Dive

Domino’s Pizza, founded in 1960, is one of the world’s largest pizza chains, operating company-owned and franchised stores across the US and international markets. With a market cap of about $10.4 billion, the company generates revenue through its store operations, franchise network, and supply chain segment while offering pizza, wings, sandwiches, pasta, desserts, and other menu items.

At one point, Domino’s was a stock market darling. From 2009 through 2021, the stock posted 13 consecutive annual gains, climbing 12,959% over that span. For those keeping score, that works out to a 45.5% compound annual growth rate.

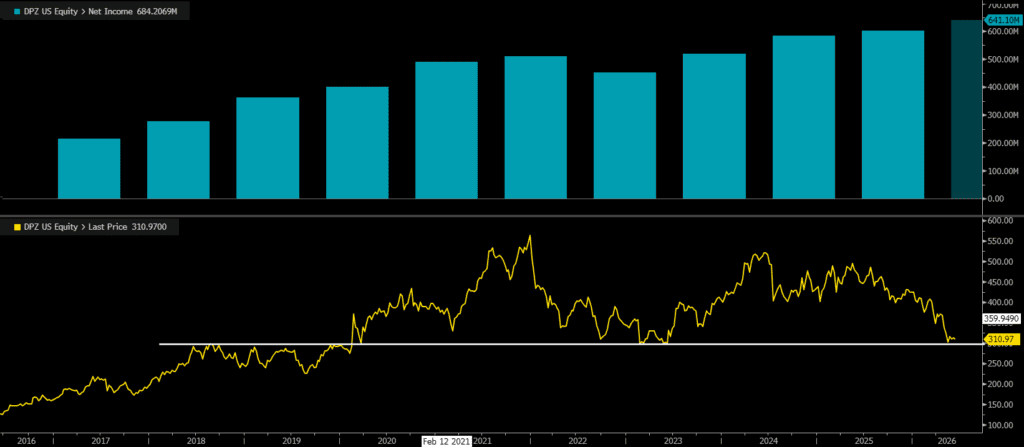

But since then, the stock has lost momentum. DPZ has posted two down years in the last four and has yet to reclaim its 2022 highs. So while this pizza maker has crushed the S&P 500 since the 2008-09 financial crisis, it has lagged over the last few years.

We have annual net income at the top of the chart, and at the bottom, we have DPZ’s stock price. Notice how the stock peaked alongside profits, but failed to recover even after net income pushed to new highs. Also note how the stock is hovering near a pivotal technical area: $300 was notable resistance before the 2020 breakout, then became key support in 2022 and 2023.

Future Growth Projections

Analysts expect consistent high-single-digit earnings growth and mid-single-digit revenue growth over the next several years. According to Bloomberg, analysts project the following:

- Earnings Growth: 9.2% in 2026, 9.4% in 2027, and 8.9% in 2028

- Revenue Growth: 5.5% in 2026, 3.4% in 2027, and 4.3% in 2028

Analysts currently have a consensus price target of ~$411 on DPZ stock, implying about 32% upside to today’s stock price.

Want to receive these insights straight to your inbox?

Diving Deeper — Valuation

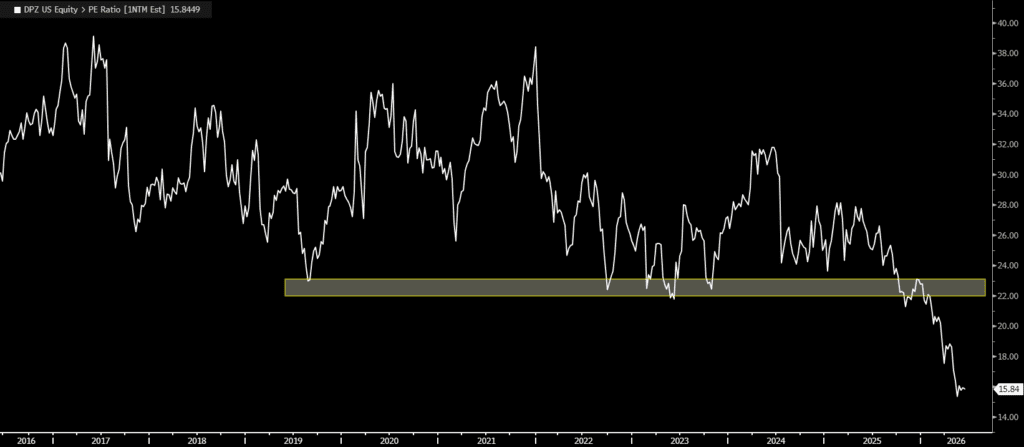

As for valuation, the stock had previously found a trough around 22 to 23 times forward earnings. That’s no longer the case, with DPZ now trading at its lowest forward P/E ratio of the last decade. Bulls will argue this makes Domino’s a value play, while detractors will argue it’s a value trap.

Risks

The main risks for Domino’s include softer consumer spending, intense competition, and margin pressure from higher food and labor costs. DPZ also relies heavily on franchisees, so store-level profitability, franchisee financial health, and execution consistency are key risks, while international exposure adds currency, geopolitical, and local-demand uncertainty. Longer term, Domino’s must keep its digital-ordering advantage, delivery speed, and value proposition strong as consumers become more price-sensitive and third-party delivery options evolve.

The Bottom Line

Domino’s checks a few boxes for investors who like to blend fundamental and technical analysis: earnings are expected to grow at a high-single-digit pace, the stock trades at its lowest forward P/E ratio in a decade, and shares are hovering near a historically important technical level.

At the same time, DPZ has clearly lacked momentum in recent years, and the latest decline is a reminder that valuation alone does not always provide the support investors expect. For bulls, the setup may look like a quality business trading at a more reasonable price; for bears, the concern is that slowing momentum, consumer pressure, and cost headwinds could keep the stock from reclaiming its prior highs.

Disclaimer:

Please note that due to market volatility, some of the prices may have already been reached and scenarios played out.