SOFI stock has been hammered from its highs, yet its growth estimates remain promising. The Daily Breakdown digs into the dip.

Interested in more Deep Dive content? Check out our latest research.

Deep Dive

It’s been a volatile run for SoFi Technologies, with shares down almost 40% so far this year. Even so, the stock is still up about 50% over the past year and even traded below $5 as recently as May 2023. So what’s the story behind this roughly $20 billion bank?

SoFi Technologies is a digital financial services company that offers banking, lending, investing, and other money-management products through a single app. It positions itself as a one-stop platform aimed at helping members borrow, save, spend, invest, and protect their money.

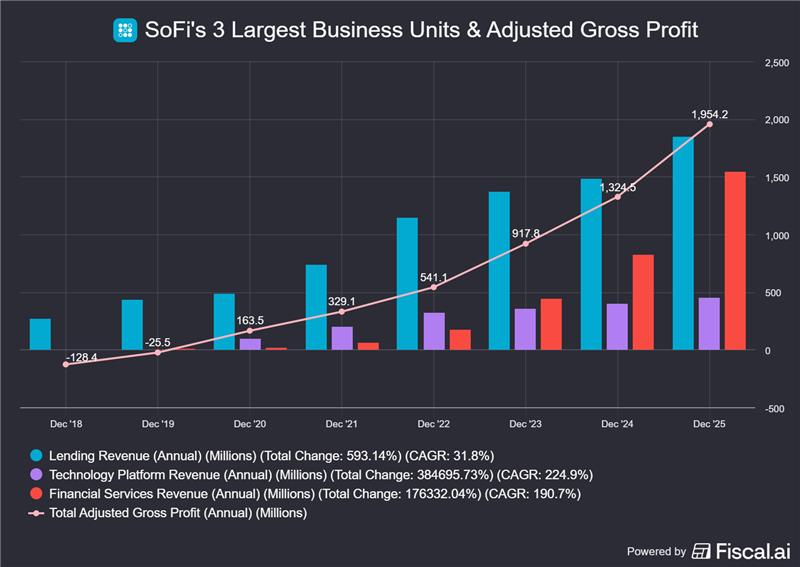

When SoFi began trading publicly in 2020, the stock opened around $11 before quickly climbing into a wide trading range of roughly $14 to $24. The ensuing bear market then dragged shares into the single digits, with the stock falling as low as $4.24. Despite that volatility, the business has continued to grow. As shown above, SoFi’s three largest businesses have expanded each year, while total adjusted gross profit has also continued to climb.

Future Growth Projections

As far as analysts are concerned, that growth should continue into the future, too. According to Bloomberg, analysts project the following:

- Earnings Growth: 56% in 2026, 32% in 2027, and 23.5% in 2028

- Revenue Growth: 30.1% in 2026, 21.3% in 2027, and 13.9% in 2028

Analysts currently have a consensus price target of ~$23.88 on SOFI stock, implying about 47% upside to today’s stock price.

Want to receive these insights straight to your inbox?

Diving Deeper — Valuation

Valuing younger companies with strong growth can be difficult. In SoFi’s case, though, that growth has helped make the valuation more reasonable:

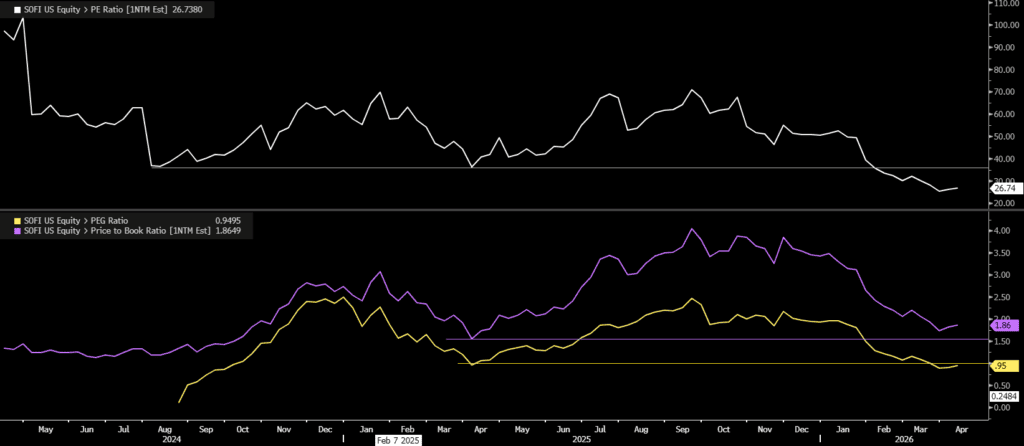

The forward P/E ratio is now near a multi-year low of roughly 26.5x, while the price-to-book ratio — a common measure for bank stocks — is below 2x and near the 2025 low, (even though the stock price is up about 90% from that period).

Lastly, SoFi’s PEG ratio — which measures valuation relative to expected earnings growth — is back below 1.0. A common rule of thumb is that a PEG ratio around 1.0 suggests a stock is fairly valued, below 1.0 may indicate undervaluation, and above 1.0 can imply the stock is expensive relative to its growth.

Risks

Some of SoFi’s main company-specific risks include its heavy exposure to personal lending and credit performance, reliance on deposits and capital-markets funding to support loan growth, and regulatory and compliance risk tied to operating a national bank. Parts of the business, particularly student lending, are also sensitive to interest rates and government policy. Like all banks and lenders, SoFi would also face broader recession risk, including weaker loan demand and higher credit losses.

The Bottom Line

The bull case is that SoFi is still growing, its ecosystem is maturing, and after such a steep drop from the highs, the valuation is far easier to stomach. The bear case is that this is still a consumer lender and bank facing credit, recession, funding, and regulatory risks. So while the selloff has helped de-risk the stock, investors still need confidence that growth can outweigh those headwinds.

Disclaimer:

Please note that due to market volatility, some of the prices may have already been reached and scenarios played out.