The Daily Breakdown takes a closer look at Micron, which has more than quadrupled over the past 12 months. Is this boom or bust?

Before we dive in, let’s make sure you’re set to receive The Daily Breakdown each morning. To keep getting our daily insights, all you need to do is log in to your eToro account.

Interested in more Deep Dive content? Check out our latest research.

Deep Dive

With a one-year gain of more than 300%, Micron has quietly amassed a market cap of roughly $430 billion. The company makes memory and storage semiconductors, including DRAM — which accounts for the majority of its business — as well as NAND flash and SSDs used in data centers, PCs, smartphones, autos, and industrial devices. In simple terms, Micron sells the chips and storage products that help devices store data and run applications faster.

As for what’s behind the stock’s huge gains this year? AI.

Micron is benefiting from that tailwind sinceAI servers require far more high-bandwidth memory (HBM) and storage than traditional computing systems. That demand is driving sales of products like HBM and data center DRAM, where Micron has direct exposure.

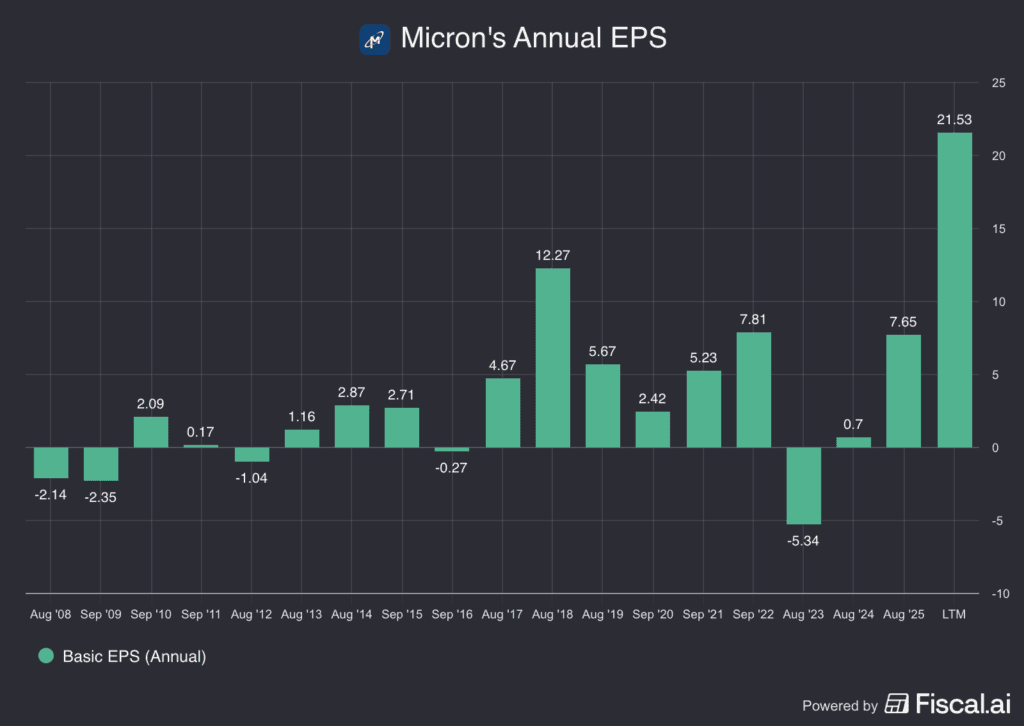

Case in point: Micron blew past estimates when it reported on March 18. Earnings of $12.20 per share topped estimates of $9 a share, while revenue of $23.9 billion rose 196% year over year and beat expectations of $19.7 billion. Notably, management’s outlook for the current quarter also came in ahead of consensus estimates.

Right now, Micron is operating in one of its boom phases, but this business has long been defined by boom-and-bust cycles. The chart above illustrates that clearly with Micron’s earnings, highlighting the current upswing alongside prior sharp downturns. Put simply, the business has not historically delivered long-term consistency. So the question is: Is this time different?

Future Growth Projections

Micron’s fiscal year ends in August, (meaning fiscal 2026 runs through August 31, 2026, and fiscal 2027 begins on September 1). According to Bloomberg, analysts project the following:

- Earnings Growth: 570% in 2026, 67% in 2027, and -14% in 2028

- Revenue Growth: 176% in 2026, 52% in 2027, and -1.5% in 2028

Analysts currently have a consensus price target of ~$536 on MU stock, implying about 46% upside to today’s stock price.

Want to receive these insights straight to your inbox?

Diving Deeper — What’s the Catch?

Micron generated $37.4 billion in revenue last year, but analysts expect that figure to reach $104.1 billion in fiscal 2026. Adjusted earnings per share of $8.30 in 2025 are projected to surge to $55.50 in 2026. Despite that growth, the stock trades at just 4 times forward earnings estimates. Yes, 4x. So what’s the catch?

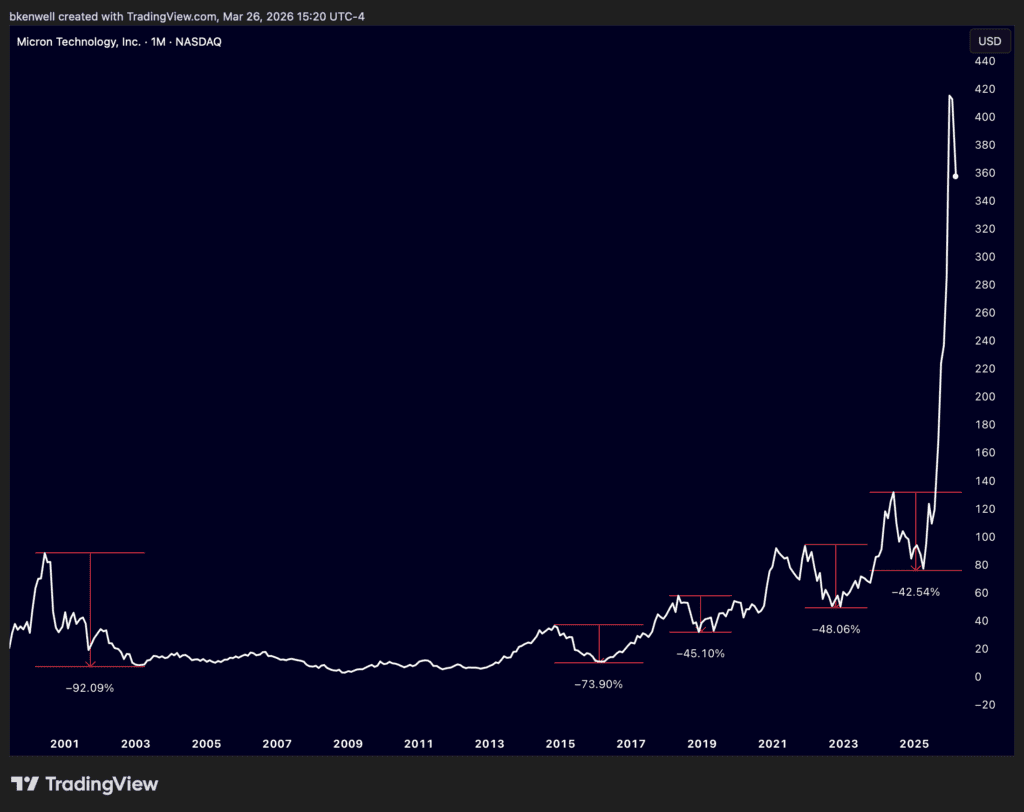

It comes back to Micron’s boom-and-bust cycles (highlighted in the stock price above). Wall Street has been reluctant to award the stock a premium valuation because of concerns around cyclicality and pricing pressure. Put another way, Micron has gone through periods where demand is enormous, supply is tight, and pricing power rises dramatically. But when demand cools or supply outpaces it, that pricing power can deteriorate just as quickly — boom, then bust.

That dynamic helps explain why investors have historically been hesitant to pay a large premium for the stock.

Micron’s biggest risks are the classic memory-chip risks, now amplified by AI. Its business is highly cyclical, so DRAM and NAND pricing can swing sharp. At the same time, its AI opportunity depends on strong execution in HBM and other higher-cost products, where manufacturing complexity, longer production cycles, and fierce competition all matter.

Beyond that, Micron remains exposed to geopolitical and regulatory pressure, including trade restrictions and the ongoing impact of China-related constraints on certain products and customers. The company is also spending heavily on capacity and advanced-node production, so any slowdown in demand, drop in utilization, or delay in scaling new fabs and technologies could weigh on profitability and returns.

The Bottom Line

Micron is one of the clearest AI beneficiaries in semis, with demand for memory helping drive explosive growth in revenue and earnings. The bull case is that AI and HBM are making Micron’s business more durable than in past cycles, while the bear case is that it remains a memory company, where supply, pricing, and demand can shift quickly. The key question for investors is whether this cycle is truly different — or whether the next downturn — the “bust” — becomes a when-not-if scenario.

Disclaimer:

Please note that due to market volatility, some of the prices may have already been reached and scenarios played out.