Millions of people across the world will book flights, hotels and road trips over the Easter break this year, and there’s a good chance they’re booking it through a company owned by Booking Holdings, one of the most dominant travel businesses on the internet. More than a billion room nights were booked through Booking Holdings’ platforms last year. If you’ve ever searched for a hotel, rental car or restaurant online, chances are you’ve used one of their brands without even realising it.

Despite delivering record revenue, record free cash flow and stellar profits in 2025, shares are down nearly 24% year-to-date in 2026 as investors weigh up whether AI could disrupt the way the world books travel. So will AI kill this travel giant or does its recent sell-off create an opportunity? Let’s find out.

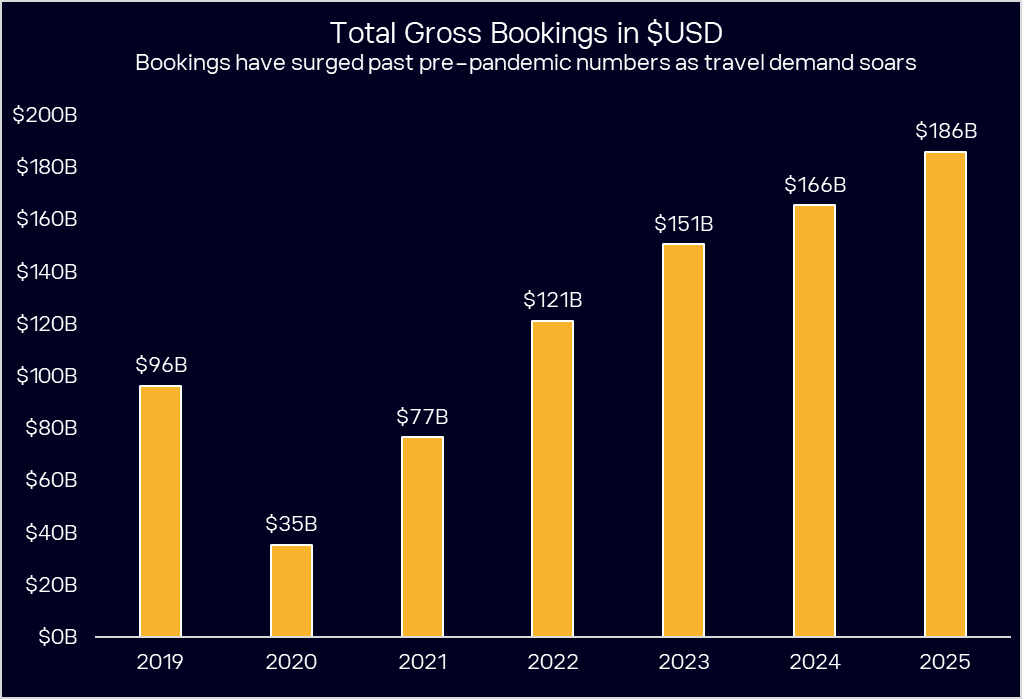

- Booking sold 68 million airline tickets and processed USD$186 billion in gross bookings in 2025, proving it’s far more than just a hotel platform.

- At 15x forward earnings with USD$9.1 billion in annual free cash flow, the market may be pricing in a worst-case scenario that hasn’t arrived.

- According to Bloomberg’s Analyst Recommendations, Booking Holdings has 32 buy ratings, 9 holds, and 0 sells, with an average price target of USD$5757.72 signalling a potential upside of 40% from its last closing price.

View Booking.Com

The Basics: What is Booking Holdings and what companies does it own?

Booking Holdings was founded in 1997 as Priceline.com and rebranded in 2018. It’s headquartered in Norwalk, Connecticut, employs around 24,300 people and operates five consumer-facing brands: Booking.com, Priceline, Agoda, KAYAK and OpenTable. The company sits at the centre of global online travel, connecting travellers with hotels, flights, rental cars, restaurants and experiences across more than 200 countries.

How big is Booking Holdings?

The business itself is massive. In FY2025, room nights hit 1.24 billion, doubling in the last four years, with car rentals also doubling over the same period and airline tickets growing rapidly off a smaller base. Total gross bookings reached USD$186 billion for the year. The business generates roughly 90% of its revenue outside the United States, which makes it a truly diversified tech platform.

Booking operates what it calls a “Connected Trip” vision, where the goal is to have travellers book their entire trip (accommodation, flights, car, restaurants, activities) through one platform. Connected Trip transactions grew in the high 20% range in 2025 and now represent a low double-digit share of total bookings, which tells you this cross-sell strategy is gaining real traction.

What is Booking.com’s Genius loyalty program?

They’ve also got a stellar loyalty platform. Booking’s Genius loyalty members at Level 2 and 3 now represent over 30% of the active customer base but account for more than 50% of all room nights booked. These loyal users also have a meaningfully higher direct booking rate, which means they bypass paid advertising channels entirely and that customer loyalty is worth its weight in gold.

Fun Fact: Booking sold 68 million airline tickets in 2025. That’s roughly 186,000 tickets booked every single day through a platform most people only associate with hotels.

Who are Booking Holdings’ competitors?

The online travel booking space has three major players, Booking Holdings, Airbnb and Expedia.

Booking is the biggest of the three. Airbnb dominates the short-term rental and alternative accommodation space, but it is moving further into services and experiences. While Expedia competes across hotels, flights and packages through brands like Vrbo, Hotels.com and Trivago.

Booking is arguably the most diversified, with exposure across hotels, alternative accommodation (8.6 million listings globally), flights, car rentals, restaurants via OpenTable and experiences.

How will AI impact Booking Holdings?

But the real competitive conversation in 2026 isn’t just these names, it’s AI. It’s getting smarter each day, and the question is whether AI agents like ChatGPT, Google’s Gemini or other large language models could eventually cut out the online travel agencies altogether, acting as a “super travel agent” that books directly with hotels and airlines on a traveller’s behalf. This fear is a big reason why Booking’s stock has sold off, and it’s not going away any time soon.

Booking’s own CFO has pushed back firmly on this risk, pointing out the enormous complexity involved in payments (100+ methods, 50+ currencies), regulatory compliance across 200+ countries, customer service and inventory management. He used a live example of asking an LLM to cancel a Dubai flight during the Middle East conflict, and the AI simply couldn’t action it. So it can actually partner with the biggest names in AI like ChatGPT or Gemini, because these platforms need someone to actually fulfil the booking, handle payments, manage customer service, and deal with cancellations.

Rather than sitting still, Booking is building its own agentic AI tools through its Connected Trip platform, with internal startups working on personalised, end-to-end trip experiences that cover pre, during and post-trip phases. The early results from AI are already showing up in the financials. Customer service costs fell in absolute terms in 2025 despite roughly 10% booking growth, delivering about a 10% reduction in cost per booking while maintaining satisfaction scores. That’s a tangible, bottom-line impact from AI. It shows that AI can improve this business, rather than kill it.

Booking Holdings financial performance: revenue, EBITDA and free cash flow

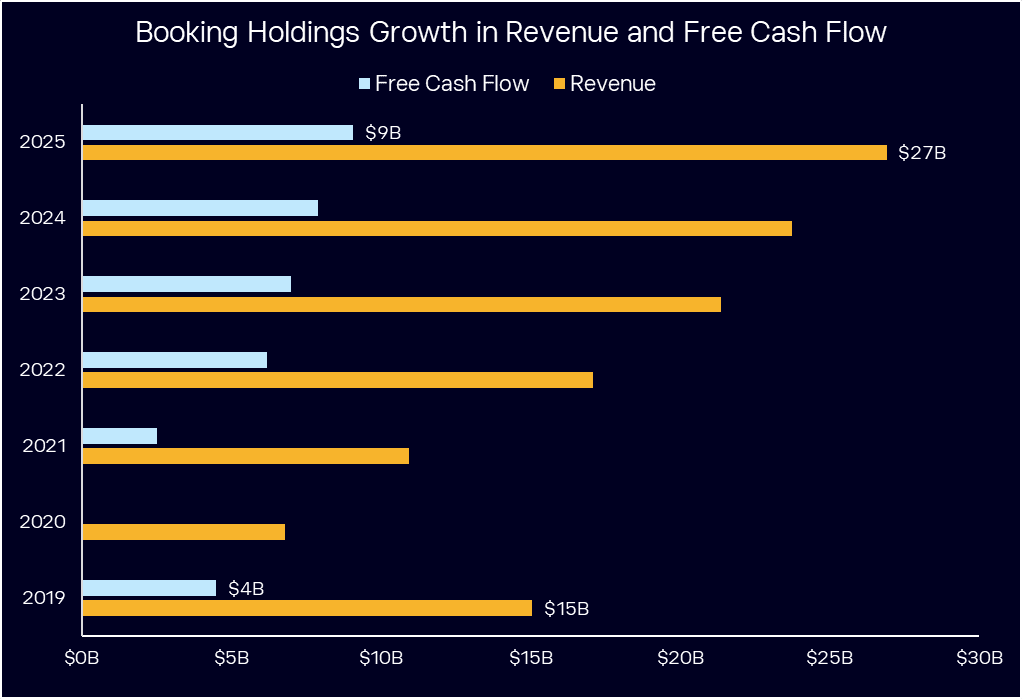

FY2025 was a standout year, with continued growth across the business. Revenue came in at USD$26.9 billion (up 13%), adjusted EBITDA hit USD$9.9 billion (up 20%, with margins expanding to 36.9%), and free cash flow was USD$9.1 billion for the year.

The growth is coming from everywhere, too. In Asia, Agoda is leading the charge with deep localisation across markets like Korea and India. In the US, room night growth accelerated from low single digits in the first half of 2025 to low double digits by the fourth quarter, and Europe remains the stronghold, with steady high single-digit growth and a dominant position through its Genius loyalty program.

Booking has been quietly running a cost transformation program that stripped out roughly USD$550 million in annual costs by the end of 2025, beating its own targets. Those savings went straight into future growth, investing around USD$700 million back into growth areas like GenAI, its Connected Trip platform, expansion across Asia and the US, and taking OpenTable international. That reinvestment is expected to generate about USD$400 million in fresh revenue.

Booking sets its own internal growth targets of 8% annual revenue growth and 15% EPS growth, and in 2025, it beat both. Looking ahead, 2026 guidance points to around 9% revenue growth, mid-teens EPS growth, and further margin expansion, showing the company isn’t slowing down any time soon.

They recently announced a 25-for-1 stock split effective April 6 and hiked its quarterly dividend by 9.4% to USD$10.50 per share, a yield of just over 1%. Stock splits don’t change the fundamentals, but they do make the stock more accessible to everyday investors and tend to generate positive sentiment. Its share price will change from USD$4,000 to around USD$160.

Buy, Hold or Sell? Should you invest in Booking Holdings?

Shares are up 70% in the last five years, but have fallen 23% so far in 2026, showing that the market has clearly priced in a meaningful risk around AI disruption.

That has dragged down its valuation, with Booking is trading at 15x around forward earnings, which would be considered cheap for a business growing revenue at 8 to 9% annually, with 20%+ EBITDA growth and nearly USD$10 billion in free cash flow.

The bullish case is that Booking has a proven ability to cross-sell (the airline business grew 37% in 2025 to 68 million tickets, and attractions grew around 80%), its cost transformation is delivering real savings, margins are expanding, and the company is returning capital to shareholders through dividends and buybacks. The agentic AI risk is clearly there, but Booking is positioning itself as a partner rather than a victim in that transition.

What are the risks with Booking Holdings?

The main risks to watch are the pace of AI adoption in travel, particularly AI agents, potential margin pressure from reinvestment spending, and the broader macro environment, which has turned noticeably tougher. Oil prices have risen sharply in 2026 amid geopolitical tensions, and the probability of rate cuts from central banks is fading, with the Reserve Bank of Australia even raising rates recently. That higher-for-longer rate backdrop tends to weigh on consumer discretionary spending, including travel.

According to Bloomberg’s Analyst Recommendations, Booking Holdings has 32 buy ratings, 9 holds, and 0 sells, with an average price target of USD$5757.72 signalling a potential upside of 40% from its last closing price. (Pricing is prior to stock split)

For investors, the central question is whether the market has overpriced AI disruption risk on an otherwise strong business, or whether that risk is yet to fully materialise. The financial track record is compelling, but the macro environment and pace of AI adoption in travel remain genuine uncertainties. As always, investors should consider their own circumstances before making any investment decision.

View Booking.Com

*Data Accurate as of 1/04/2026

*Sources: Bloomberg and Booking Holdings Investor Relations

eToro Service ARSN 637 489 466 operated by eToro Asset Management Limited ABN 51 122 005 396 AFSL 319738 and promoted by eToro AUS Capital Limited ACN 612 791 803 AFSL 491139. Investing in shares via a managed investment scheme does not result in direct ownership of the underlying assets. The scheme has legal ownership, the investor has beneficial ownership, i.e. the shares are held on your behalf. As the scheme has legal ownership, you have no rights in the securities, including voting rights. Shares are non-transferable. Your capital is at risk. Refer to the Product Disclosure Statement and Target Market Determination (PDS and TMD) before transacting. See full disclaimer.