Lithium stocks are back in the spotlight after a brutal two years, and one of the more interesting stories in the Australian lithium space is Vulcan Energy (VUL.ASX). It’s not riding the same price cycle as the rest. It’s playing a different game altogether, one built around geothermal energy, low cost, net-zero lithium from brines and Europe’s push for clean supply chains.

While most lithium companies spent 2025 cutting costs and shelving projects, Vulcan went the other way, signed up some of the biggest names in the European auto industry as customers and kept building. Let’s find out why, and if Vulcan Energy is a good investment.

- Vulcan Energy is an ASX stock available at eToro.

- Vulcan is fully funded after securing a AUD$3.9 billion financing package and has started construction on its flagship Lionheart project in Germany.

- Major customers are already locked in, including Stellantis, Umicore, LG Energy Solution and Glencore, covering more than 70% of expected output.

- According to Bloomberg’s Analyst Recommendations, Vulcan Energy has 5 buy ratings, 0 holds, and 0 sells. The average analyst price target is AUD$7.40, signalling approximately 100% upside from current levels.

Explore Vulcan Energy

What is Vulcan Energy?

Vulcan Energy is developing a lithium project in Germany’s Upper Rhine Valley. But it’s not a mine in the traditional sense. Most lithium comes from one of two sources. Hard rock mining, think big open-pit mines in Western Australia, or extracting it from salty underground water known as brine, is commonly used in South America and China. Both traditional methods are energy-intensive and leave a significant environmental footprint.

More recently, the industry has been shifting towards a faster, cheaper method called adsorption-type direct lithium extraction (A-DLE), which pulls lithium from brine in hours rather than months using a special adsorbent material. It currently makes up around 10% of global lithium production, but it’s increasingly the method of choice, with major players like Rio Tinto backing it heavily, because of its low cost of production.

Vulcan uses this approach, but takes it a step further. It taps into hot, lithium-rich brine deep beneath the surface. Using A-DLE, it extracts battery-grade lithium and reinjects the brine back where it came from. At the same time, it captures the geothermal heat to generate renewable energy. No blasting, no diesel, just lithium and clean energy from the same source

The project’s flagship, known as Lionheart, is targeting 24,000 tonnes per year of lithium hydroxide at full capacity, enough to supply around 500,000 EVs annually. First production is targeted for 2028.

Vulcan’s ambition is to be the first company in the world to produce lithium with net-zero fossil fuel use. That also means lower water usage and land disturbance compared to traditional methods, as well as lower production costs.

Fun Fact: Vulcan is backed by Gina Rinehart’s Hancock Prospecting, Australia’s richest person. Vulcan was actually Rinehart’s first lithium investment, before her bigger moves into Liontown and Azure Minerals.

Source: Vulcan Energy

Why ASX Lithium Stocks Are Back in Focus

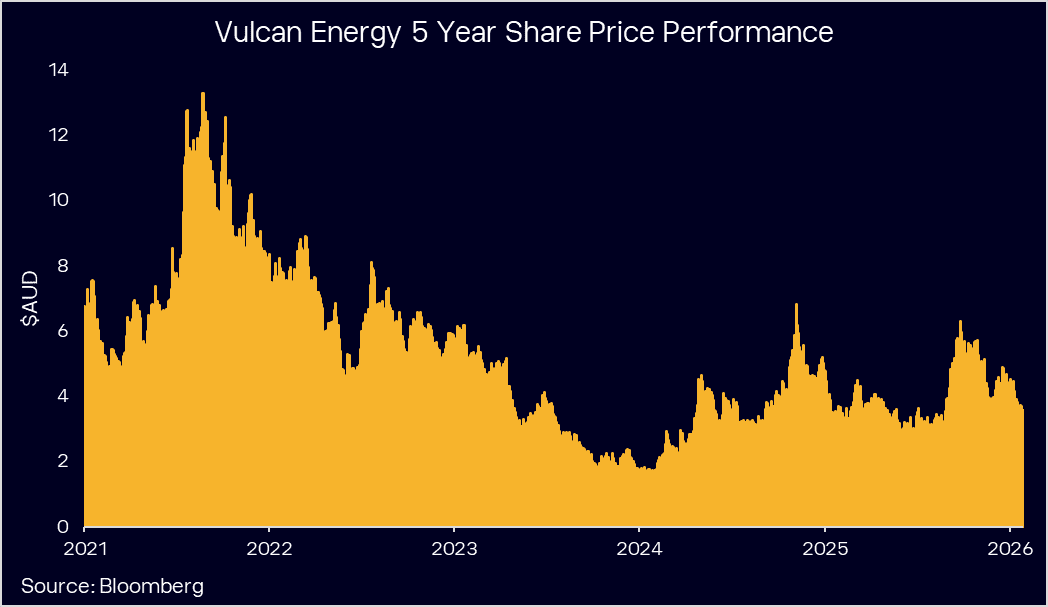

The broader lithium sector has rebounded since late 2025. Lithium prices surged over 50% in the back half of the year, EV sales have remained solid globally, and excess supply appears to be working through the system. Vulcan shares have participated in that rebound, up around 100% from their 2024 lows, though still well off the highs above AUD$13 hit back in 2021.

For Vulcan, 2025 was a breakout year operationally and financially. The company secured a €2.2 billion (AUD$3.9B) funding package to finance Phase One of the Lionheart project, one of the largest for a strategic raw material project in Europe. Off the back of that, Vulcan’s board gave the green light to start building, known in the industry as a Final Investment Decision (FID), placing it in rare territory. Very few lithium projects globally have reached FID in recent years, which gives Vulcan a significant head start heading into the next upcycle.

Long-term supply deals are locked in with Stellantis, LG Energy Solution, Umicore, and, most recently, Glencore, which signed on for 36,000 to 44,000 tonnes of lithium over an initial eight-year period. All agreements are binding, meaning customers have to buy the lithium and that kind of customer list is hard to argue with.

Construction kicked off in December with a groundbreaking ceremony at the main extraction plant in Landau, and the company has signed contracts with major engineering and technology partners to deliver Phase One. It’s also mapping out Phase Two, which is expected to require materially lower capex thanks to learnings and tech efficiency gains.

Beyond the company-specific milestones, there’s a bigger structural tailwind at play. Europe is desperate to onshore lithium supply to support its EV goals and reduce dependency on China. Vulcan ticks every EU policy box: local, low-emissions, and strategic. That’s helped it win regulatory fast-tracking, public grants and significant private sector buy-in.

What strengthens Vulcan’s position further is its proprietary extraction technology, VULSORB, which has already been successfully piloted and is ready for commercial rollout. This matters because, outside of Rio Tinto and Eramet, Vulcan is one of the few Western lithium companies with in-house adsorption-type direct lithium extraction (A-DLE) technology. Most others still rely on Chinese providers, which are now facing export restrictions. Vulcan owns its tech outright, giving it an edge most peers don’t have, at a time when the investment community is looking for “briners over miners” in lithium.

*Past performance is not an indicator of future results

Vulcan Energy Financial Health Check

We might talk about a valuation of a company, its dividend yield or how to analyse the business. But Vulcan isn’t a traditional business in that sense, given it won’t be generating revenues until 2028. So, instead, we’re going to look at whether the company is well-funded and what its runway looks like.

The short answer is yes. The €2.2 billion (AUD$3.9B) financing package secured in December covers the full construction of Phase One, backed by the European Investment Bank, German state-backed lenders, government grants, and industrial partners including HOCHTIEF, which committed €169 million. The company also raised approximately AUD$710 million from investors at AUD$4.00 per share. Vulcan spent €14.9 million in the December quarter, primarily on drilling and early construction works. That spend will ramp significantly through 2026 and 2027 as construction accelerates, but the funding is in place to cover it.

The company does generate modest revenue from its existing geothermal plant, which produced around 6.1 GWh of renewable power in the quarter, generating €1.6 million in gross revenue. It’s small, but it’s real operating income from an asset that validates the geothermal model.

One thing worth watching is how Vulcan tracks against its budget. A €2.2 billion project build is complex, and cost overruns are always a risk for first-of-kind projects. If costs blow out, the company may need to raise additional capital, which would dilute existing shareholders. For now, though, the project is fully funded, and construction is underway. Vulcan reports full-year results on the 26th March.

One major shift in this lithium cycle is that institutional capital is increasingly backing brine projects over hard rock. Brines tend to have lower operating costs and longer project lives, making them more resilient through commodity cycles. Rio Tinto’s USD$17 billion commitment to brine assets through its Arcadium Lithium acquisition is a strong signal about where the industry sees long-term value. Vulcan, as a low-cost brine project with in-house tech in the heart of Europe, fits squarely into that narrative.

Should you Buy, Hold or Sell Vulcan Energy?

Vulcan’s model is different, and that’s both its edge and its biggest risk. Vulcan needs to execute geothermal energy, lithium chemistry and reinjection all in one integrated loop.

The December quarter provided a reminder of this with one of the company’s well sidetracks having to be abandoned after geological instability, resulting in a €7.8 million write-down. A follow-up well was drilled successfully in January, but it’s a reminder that the technical challenges are real.

Production is still a few years away, so if lithium prices slump again or sentiment turns, margins could come under pressure. And with strict environmental rules in Germany, any community pushback could delay timelines.

But ultimately, Vulcan is offering something very few others can: low cost, net-zero lithium from brines, made in Europe, at commercial scale. At a time when automakers and policymakers increasingly want cleaner, locally sourced inputs, that’s a powerful position to be in. And it’s not just about production. Vulcan plans to license its VULSORB technology globally. If that gains traction, it opens a new revenue stream that sits outside traditional mining, think tech royalties on top of commodity sales.

According to Bloomberg’s Analyst Recommendations, Vulcan Energy has 5 buy ratings, 0 holds, and 0 sells. The average analyst price target is AUD$7.40, signalling approximately 100% upside from current levels.

Vulcan Energy is not a simple lithium price play. It’s a structural, policy-aligned play on the future of clean supply chains. Europe’s carmakers are in a scramble for local battery materials, and Vulcan is one of the only producers setting up shop inside the gates. When everyone else is importing lithium halfway across the world, proximity matters.

There’s plenty of work ahead, but the pieces are falling into place. Keep an eye on construction milestones, Phase Two economics, and any movement on DLE tech licensing. The blueprint is there; now it’s about execution.

How to buy Vulcan Energy shares on the ASX

Explore Vulcan Energy

Vulcan Energy (VUL) is listed on the Australian Stock Exchange (ASX). Investors can buy shares through online brokerages including eToro.

eToro Service ARSN 637 489 466 operated by eToro Asset Management Limited ABN 51 122 005 396 AFSL 319738 and promoted by eToro AUS Capital Limited ACN 612 791 803 AFSL 491139. Investing in shares via a managed investment scheme does not result in direct ownership of the underlying assets. The scheme has legal ownership, the investor has beneficial ownership i.e. the shares are held on your behalf. As the scheme has legal ownership, you have no rights in the securities, including voting rights. Shares are non transferable. Your capital is at risk. Refer to the Product Disclosure Statement and Target Market Determination (PDS and TMD) before transacting. See full disclaimer.