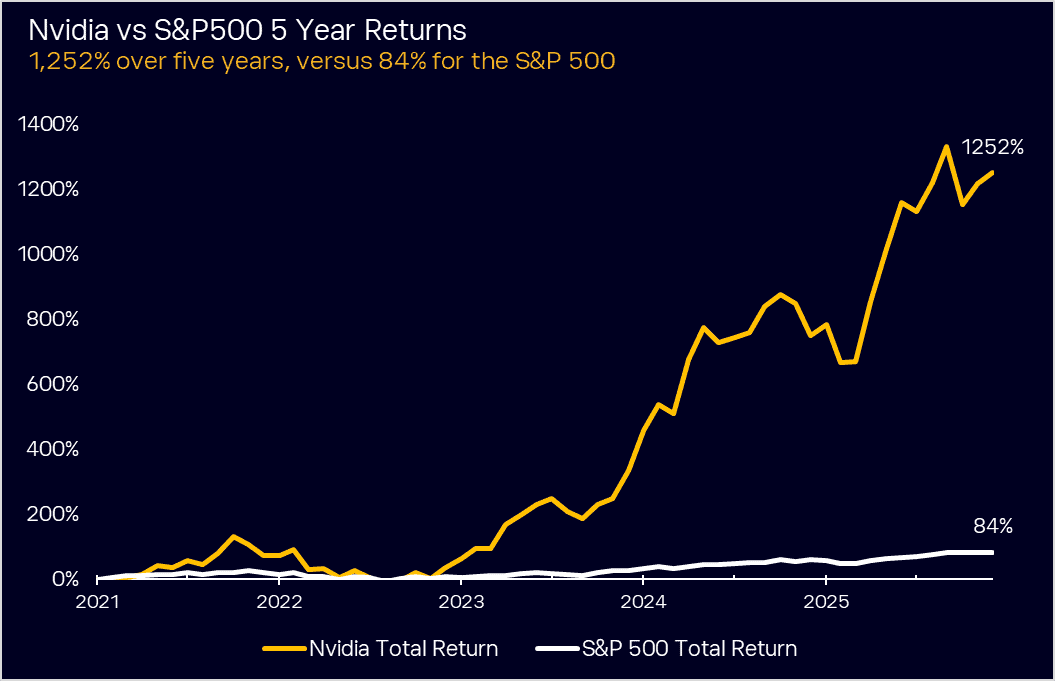

Nvidia stock has become one of the most searched investments of 2026 — and for good reason. Unless you’ve been hiding under a rock for two years, you’ll be well aware of the transformative potential of Artificial Intelligence (AI) across just about every industry, with ChatGPT a key catalyst of mainstream adoption. Within that time, arguably the biggest beneficiary from the AI boom, Nvidia, has become the world’s largest stock, surpassing tech titans Microsoft and Apple, reaching a market cap of USD$4.7 trillion. After continuously delivering outstanding numbers, can the golden child of AI keep delivering and continue to grow? Let’s find out.

- Nvidia has grown its revenue by more than 1,000% in three years, driven by insatiable demand for its AI chips from the world’s biggest tech companies.

- Nvidia has over USD$500 billion in combined Blackwell and Rubin revenue visibility through 2026, with substantial deliveries still ahead, suggesting the growth story is far from over.

- Nvidia has 78 buy ratings, 4 holds, and 1 sell, with an average price target of USD$263.26 signalling a potential upside of 35% from its last closing price.

View Nvidia Corp

What does Nvidia actually do and why does AI need it?

Nvidia designs and sells graphics processing units (GPUs), a field it has been pioneering since the late 1990s, when it introduced the GPU for gaming applications. Graphics processing units were originally designed to render video game graphics, but their ability to handle thousands of calculations simultaneously made them the ideal engine for training and running AI models. When ChatGPT exploded onto the scene in late 2022, the world suddenly needed an enormous amount of computing power, fast, and Nvidia was the only company with the chips, the software, and the scale to deliver.

Today, Nvidia’s data centre business generates 91% of its total revenue, a seismic shift from just three years ago when gaming accounted for 45%. Its two flagship chip families, Hopper and the next-generation Blackwell, are the most sought-after products in the technology industry. Hyperscalers, including Microsoft, Amazon, Alphabet, and Meta are spending hundreds of billions of dollars on AI infrastructure, and the vast majority of that spending flows directly to Nvidia.

Nvidia is arguably the poster child of the AI trade, and everyone wants to partner with them. It is a key partner in the USD$500 billion Stargate Project alongside Microsoft, Oracle, and SoftBank, and has struck a landmark deal with OpenAI to deploy 10 gigawatts of Nvidia systems, with up to USD$100 billion committed in support.

Beyond AI infrastructure, it has partnered with Eli Lilly on AI-driven drug discovery, with Uber on autonomous vehicles, and with Nokia and T-Mobile on next-generation 6G networks. Its recent partnership with Meta marks the first major deployment of Nvidia’s stand-alone CPUs for back-end servers, opening the door to the roughly USD$30 billion annual CPU market and adding a meaningful new revenue stream beyond GPUs. Nvidia is becoming embedded infrastructure across some of the world’s largest industries, and that matters enormously for its long-term growth runway.

Fun Fact: You might be surprised to know that CEO Jensen Huang has been focusing on AI for over a decade as he saw GPUs playing a more significant role in the adoption of machine learning technology. That long-term conviction is a big reason Nvidia was so perfectly positioned when the AI boom arrived.

*Past performance is not an indication of future results.

Who are Nvidia’s competitors?

Nvidia is by far and wide the dominant force in the chip-making space. Nvidia commands an estimated 85% share of the AI accelerator market, and analysts expect it to retain over 90% of GPU market share for the foreseeable future. That dominance is reinforced not just by its chips, but by CUDA, its proprietary software platform that developers, researchers, and enterprises have spent years building their AI workloads around. Switching away from Nvidia means re-engineering software that has taken years to build, which is why even customers developing their own chips still rely on Nvidia for the bulk of their computer needs.

AMD is the most credible challenger, holding around 5% of the AI accelerator market today, but closing the gap is a little like trying to catch a moving train. Its data centre segment generated USD$16.6 billion in revenue in 2025, up from USD$12.6 billion the prior year, and it has struck a 6-gigawatt GPU agreement with OpenAI for its MI450 chips beginning in the second half of 2026. Intel remains a more distant third, with its AI accelerator roadmap considered behind both Nvidia and AMD and unlikely to be truly competitive until around 2028 to 2029.

The more interesting competitive threat comes from Nvidia’s own customers. Microsoft, Meta, Amazon, and Alphabet collectively account for roughly half of Nvidia’s revenue, and all four are developing proprietary AI chips to reduce their reliance on Nvidia over time. These in-house solutions are used internally for now and are unlikely to displace Nvidia in the near term, but they represent a long-term risk worth watching.

The company enabling much of that in-house chip development is Broadcom, which holds an estimated 60 to 80% of the AI ASIC market (essentially custom-built AI chips) and generated USD$20 billion in AI revenue in fiscal 2025, growing to a projected USD$50 billion in fiscal 2026. Broadcom doesn’t compete with Nvidia directly, but it is the engine behind Google’s and Meta’s custom chips, built to handle specific AI tasks at a lower cost than Nvidia’s. It is the quiet enabler of Nvidia’s biggest long-term risk.

Nvidia’s financials in 2026: how strong are the numbers?

The numbers Nvidia has been putting up are genuinely difficult to contextualise. In fiscal year 2026 (which ended January 2026), Nvidia generated USD$215 billion in revenue, up 65% from the year prior. For context, that is roughly the entire revenue of McDonald’s, Nike, Netflix, and Spotify combined, in a single year.

Nvidia has just reported its Q4 FY2026 results. Revenue of US$68.13 billion for the quarter beat estimates of around US$65.9 billion, data centre revenue hit a record US$62.3 billion against expectations of US$60.4 billion, and adjusted EPS of US$1.62 cleared the US$1.53 consensus. Profit for the quarter reached US$43 billion, and to put that number in context, that’s more than Nvidia’s entire annual revenue as recently as 2023. For a business to grow at this scale, given its size, it’s truly remarkable. Gross margins of 75.2% came in ahead of forecasts, helping to remove any lingering doubts about profitability at scale as the Blackwell platform matures.

Q1 FY2027 revenue guided to a midpoint of US$78 billion, comfortably ahead of the US$72.78 billion Wall Street was expecting. The Q1 guidance also assumes zero China data centre revenue at all, meaning any easing of export restrictions would be pure upside that isn’t yet priced in.

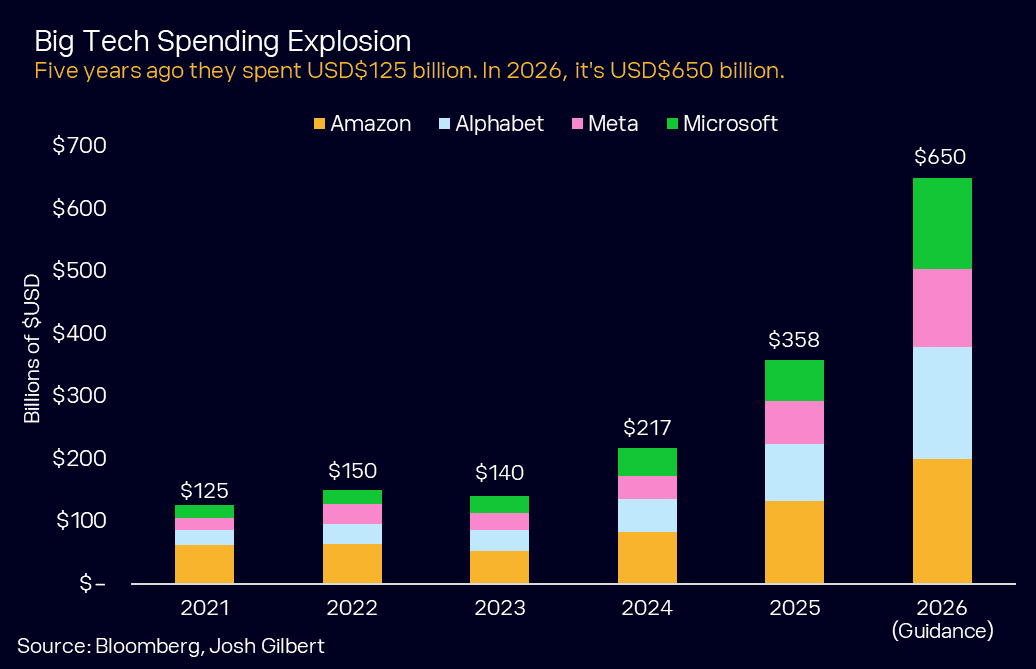

The AI race is accelerating, and Big Tech’s capex commitments have exploded dramatically. Amazon, Alphabet, Meta, and Microsoft combined spent USD$125 billion on AI infrastructure in 2021. By 2025 that had nearly tripled to USD$358 billion, and in 2026 they are collectively expected to spend USD$650 billion. Nvidia remains the key beneficiary of that spending. That’s evidenced in the numbers, with networking revenue surging 263% year-on-year to a record US$11 billion. Ultimately, building out AI at this scale isn’t just about buying chips, it’s about rewiring entire data centres from the ground up.

Since ChatGPT’s emergence, Nvidia’s data centre revenue has grown nearly 13 times over. The AI race is accelerating, big tech is spending at an unprecedented pace, and Nvidia remains the company that everyone has to go through to build their tech.

* Past performance is not an indication of future results.

Is Nvidia stock a buy in 2026?

The question now is whether a company worth USD$4.6 trillion can keep growing.

Since high-quality data centres are part of the core infrastructure in every country, NVIDIA’s runway isn’t short. However, it won’t all be one way for Nvidia. Competition will rise, especially given the sheer demand we will see. Export restrictions remain a meaningful headwind for China’s revenue. Gross margins may come under pressure as it ramps up its more complex configurations. And if AI capex ever decelerates, Nvidia, with 91% of its revenue tied to data centres, would feel it quickly.

Its forward earnings multiple of 27x is modest for a business growing revenue at 60 to 70% per year with net profit margins above 50%. The S&P 500 currently trades at 23x expected earnings, and Nvidia sits right in line with peers like Alphabet (27x) while trading below Apple (31x) despite delivering growth rates several multiples higher. The valuation isn’t cheap in absolute terms, but the growth rates and revenue visibility more than justify the premium.

According to Bloomberg’s Analyst Recommendations, Nvidia has 78 buy ratings, 4 holds, and 1 sell, with an average price target of USD$263.26 signalling a potential upside of 35% from its last closing price.

Management has flagged over USD$500 billion in combined Blackwell and Rubin backlog through 2026, with an estimated USD$350 billion still to be delivered. The next-generation Vera Rubin platform, due in the second half of 2026, is expected to offer significantly better inferencing and training performance at a lower cost per token than Blackwell, setting up another product cycle that hyperscalers are already lining up for.

Investors will need to ask themselves if they’re happy to sit on the sidelines while the company builds the infrastructure powering the next decade of technology. For those willing to pay today’s valuation for tomorrow’s infrastructure, Nvidia offers the strongest combination of market leadership, execution track record, and revenue visibility in the AI chip market.

View Nvidia Corp

*Data Accurate as of 23/02/2026

*Sources: Bloomberg and eToro

eToro Service ARSN 637 489 466 operated by eToro Asset Management Limited ABN 51 122 005 396 AFSL 319738 and promoted by eToro AUS Capital Limited ACN 612 791 803 AFSL 491139. Investing in shares via a managed investment scheme does not result in direct ownership of the underlying assets. The scheme has legal ownership, the investor has beneficial ownership, i.e. the shares are held on your behalf. As the scheme has legal ownership, you have no rights in the securities, including voting rights. Shares are non-transferable. Your capital is at risk. Refer to the Product Disclosure Statement and Target Market Determination (PDS and TMD) before transacting. See full disclaimer.