Amazon is one of those businesses that barely needs an introduction. Most of us use it, and many businesses in the world rely on its cloud platform. It is the fifth largest company in the world by market cap and one of the most dominant businesses ever built.

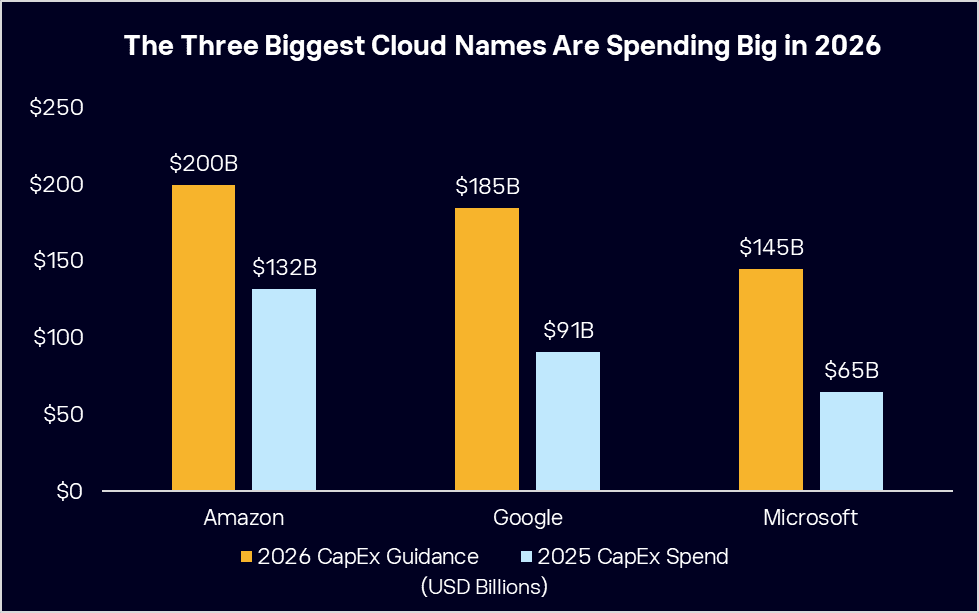

Q4 results in February showed strong top-line growth, but it was the spending that rattled investors. Amazon guided to USD$200 billion in capital expenditure for 2026, for some context, that capital expenditure guidance would be the largest single-year capex by any individual company in history, and the bulk of it is going straight into AI and cloud infrastructure. That is more than the GDP of most countries, spent in a single year. So is that spending justified, or will it be a costly mistake? Let’s find out.

- Over 85% of global IT spending still happens on company-owned servers. Amazon is spending big to make sure it’s leading with a view this will change to cloud.

- AWS backlog has hit USD$244 billion, advertising revenue is up 22%, and its chip business could rival Nvidia with a standalone run rate of USD$50 billion.

- According to Bloomberg’s Analyst Recommendations, Amazon has 77 buy ratings, 5 holds, and 0 sells, with an average price target of USD$283.23 signalling a potential upside of 18% from its last closing price.

View Amazon

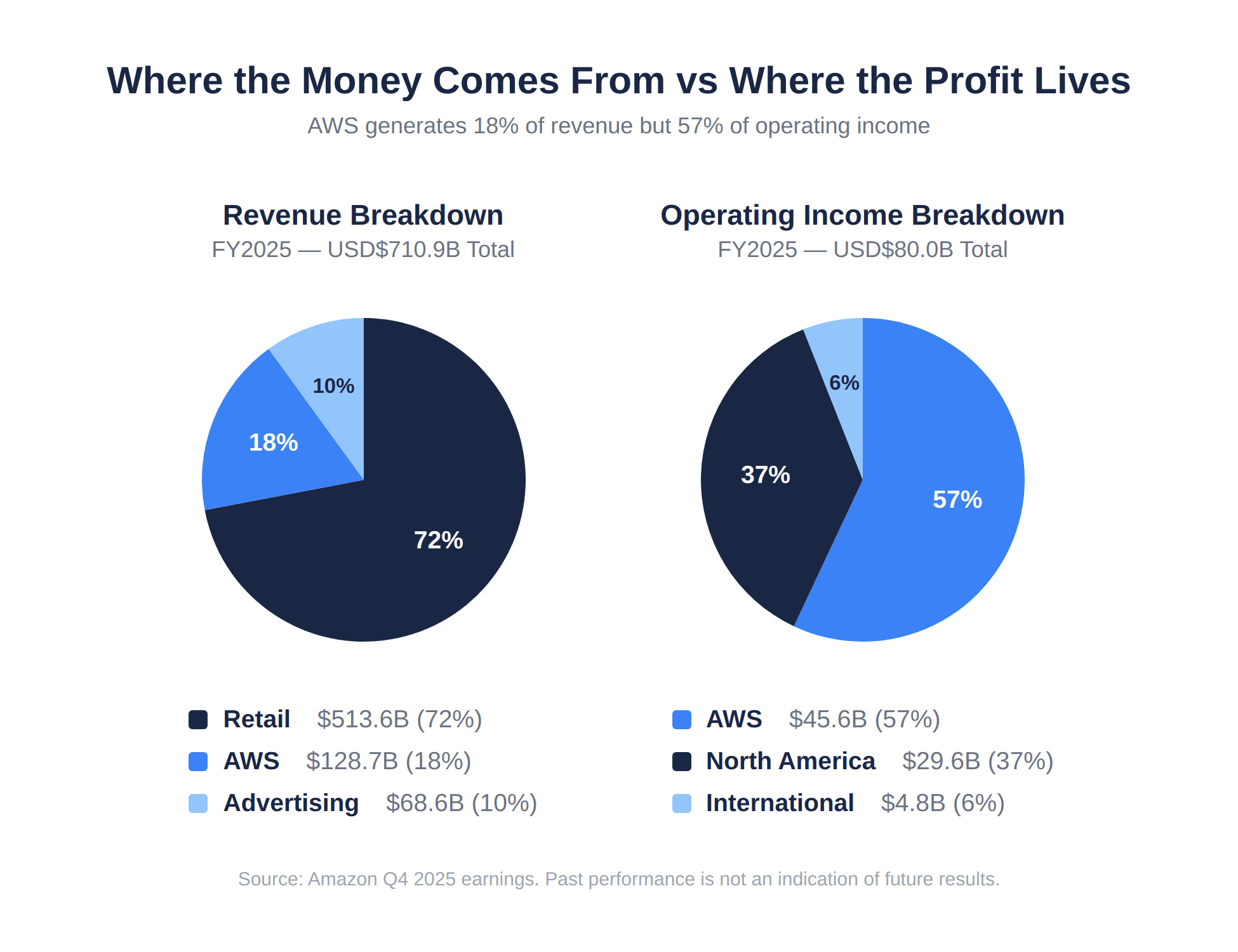

Amazon operates across three core segments. The first is its retail and e-commerce business, which is what most people know it for. It serves more than 240 million Prime members worldwide, and that membership base is central to the business model. Prime creates a loyalty loop that keeps customers coming back, whether it is for same-day delivery, streaming, groceries, or everyday essentials.

AWS: The Engine Behind Amazon’s Profits

The second is Amazon Web Services (AWS), its cloud computing division and the engine behind most of Amazon’s profits. AWS generates only 18% of revenue but contributes 57% of operating income thanks to considerably higher margins. It’s also the largest cloud platform in the world with around 32% market share, generating roughly USD$142 billion in annualised revenue. More of the top 500 US start-ups use AWS as their primary cloud provider than the next two providers combined. Its customer list includes names such as OpenAI, Visa, the NBA, BlackRock, and the US Air Force.

Amazon Advertising Revenue: The Hidden Growth Driver

Then there is advertising, which has quietly become one of the most important parts of Amazon’s business. This often surprises people, but Amazon is now the third-largest digital advertising platform in the world behind Google and Meta. Amazon’s ad revenue hit USD$21.3 billion in Q4 alone, up 22% year on year, and the company is increasingly turning those site visits and Prime Video views into ad dollars that help underpin its massive profitability.

Beyond these three pillars, Amazon is building what could become the next generation of growth engines. Its custom AI chip business already exceeds a USD$20 billion annual run rate and is growing at triple-digit percentages. It is also developing Kuiper, a satellite internet project, and holds strategic investments in companies like electric vehicle maker Rivian.

Fun Fact: Amazon has over one million robots working across its fulfilment network, making it one of the largest employers of robots on the planet.

Amazon vs the Competition: AWS, Nvidia, and Retail Rivals

In cloud computing, the competition is fierce. Microsoft’s Azure and Google Cloud are both scaling aggressively, and with AWS, the three are collectively expected to spend close to USD$600 billion on AI infrastructure in 2026 alone. That is more than double what they spent the year before.

What is interesting, though, is that despite the market treating Amazon’s USD$200 billion capex guide as the most alarming number of the lot, Amazon is actually the least capital-intensive of the three big cloud names relative to revenue. Its capex-to-revenue ratio from 2025 sits at around 18.5%, compared to roughly 26.7% for Google, and 22.9% for Microsoft. Amazon is spending the most in absolute terms, but it is doing so off the largest revenue base, which arguably gives it more room to absorb the investment.

AWS also carries a significant competitive advantage in its commercial backlog, which now sits at USD$244 billion, up 40% year on year and 22% quarter on quarter. That is future contracted revenue that gives Amazon a level of visibility its competitors struggle to match.

In retail, competition is heating up. Walmart is ramping up its online efforts and Chinese apps such as Temu and Shein are making gains, particularly at the lower end of the market. But Amazon’s push into categories such as groceries and everyday essentials is building the kind of purchase frequency and cross-selling behaviour that is difficult for rivals to replicate.

Amazon is increasingly positioning its chip business as more than just internal, and one that could rival the world’s biggest, Nvidia. CEO Andy Jassy recently suggested the company could begin selling chips to third parties, estimating the standalone business would have a run rate of around USD$50 billion. At scale, Amazon expects its own chips to save tens of billions in capex per year and deliver several hundred basis points of operating margin advantage over relying on third-party silicon for inference. It is still early days, but the ambition is clear.

* Past performance is not an indication of future results.

Amazon Stock Forecast 2026: Buy, Hold, or Sell?

Amazon’s CEO has said that over 85% of global IT spending still happens through companies owning and running their own servers and data centres rather than using the cloud, and expects this to reverse over the next 10 to 20 years. If that plays out, the runway ahead is massive.

The AI business already has a multi-billion dollar annual revenue run rate and is growing at triple-digit percentages, and it is still in its very early days. The commercial backlog of USD$244 billion provides strong revenue visibility, the advertising business is a high-margin growth engine, and the retail operation continues to gain share across new categories.

Amazon, like its peers, has little choice but to spend to stay competitive in the AI arms race, but the payoff remains uncertain. USD$200 billion in capex is an enormous commitment.

AWS margins are compressing as depreciation costs rise, and free cash flow is expected to turn negative in 2026. The AI arms race is forcing all hyperscalers to spend aggressively, close to USD$800 billion this year. That’s a number that’s going to leave everyone feeling a little uneasy and there is a real risk that the industry collectively over-invests. There are also macro headwinds to consider, including tariff risk on third-party sellers, with Chinese sellers accounting for a significant portion of marketplace sales, and the broader impact of higher oil prices on logistics costs.

At around 31 times forward earnings, Amazon is trading as one of the most expensive amongst the Magnificent 7, bar Tesla. Amazon’s premium valuation reflects strong AWS growth momentum and the market’s view that its cloud business justifies a higher multiple despite the lower-margin retail operations.

According to Bloomberg’s Analyst Recommendations, Amazon has 77 buy ratings, 5 holds, and 0 sells, with an average price target of USD$283.23 signalling a potential upside of 18% from its last closing price.

The long-term positioning is hard to argue with. AWS, advertising, and retail are all growing, the AI opportunity is just getting started. Amazon’s track record of capital allocation deserves the benefit of the doubt. This is a company that has consistently invested ahead of the curve, whether it was building out AWS when no one understood cloud computing, or building a logistics network that now rivals FedEx and UPS. With Amazon, you are investing in the next decade, not the next quarter.

View Amazon

*Data Accurate as of 15/04/2026

This communication is general information and education purposes only and should not be taken as financial product advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial product. It has been prepared without taking your objectives, financial situation or needs into account. Any references to past performance and future indications are not, and should not be taken as, a reliable indicator of future results.

eToro Service ARSN 637 489 466 operated by eToro Asset Management Limited ABN 51 122 005 396 AFSL 319738 and promoted by eToro AUS Capital Limited ACN 612 791 803 AFSL 491139. Investing in shares via a managed investment scheme does not result in direct ownership of the underlying assets. The scheme has legal ownership, the investor has beneficial ownership, i.e. the shares are held on your behalf. As the scheme has legal ownership, you have no rights in the securities, including voting rights. Shares are non-transferable. Your capital is at risk. Refer to the Product Disclosure Statement and Target Market Determination (PDS and TMD) before transacting. See full disclaimer.