The largest initial public offering ever hit the market last Friday, and within a single session, it had rewritten the leaderboard of Elon Musk’s empire, and reportedly made Musk the world’s first trillionaire. SpaceX priced at USD$135 a share, raised USD$75 billion and closed its debut up 19% at USD$160.95. After another few solid days of trading, the rocket and AI company is sitting on a market capitalisation of roughly USD$2.5 trillion and ranking as the sixth most valuable listed company on the planet.

Quite simply, the scale of this listing is unprecedented by capital raised . It has been orchestrated by the most closely followed entrepreneur of his generation. But, on debut, this is a company posting a multi-billion-dollar quarterly loss while being valued north of two trillion dollars, with soaring interest from retail investors. With the SpaceX IPO now complete, investors are asking a different question: not just can you buy SpaceX stock, but what are you actually buying? Let’s find out.

- Until last week, SpaceX was locked away for institutions and insiders. Now, anyone can own a slice of Musk’s rocket, satellite and AI empire.

- Underneath one ticker sit three very different businesses: a dominant rocket launcher, a profitable, fast-growing Starlink network, and a cash-hungry AI arm that is driving the group’s losses.

- At around 135 times sales, SpaceX is the most expensive stock in the Nasdaq 100 by a wide margin, which means the question for investors isn’t whether SpaceX is a great company, but whether it’s worth the price.

View SpaceX Shares

Past performance is not a reliable indicator of future performance. Your capital is at risk. This information is general in nature and does not take into account your personal objectives, financial situation or needs. Consider whether it is appropriate for you before acting on it.

Three businesses, one ticker

SpaceX, formally Space Exploration Technologies Corp., is the company Musk founded in 2002 with the long-running goal of driving life beyond Earth, and it has spent the better part of two decades turning that ambition into the dominant force in the global orbital launch market, first with its workhorse Falcon rockets and now with Starship, the giant next-generation vehicle it sees as its future. The business that listed on the Nasdaq on Friday, however, is more than rockets alone. The SpaceX stock symbol is SPCX, with SpaceX shares now trading on the Nasdaq.

Its Starlink satellite broadband network, which began offering service in 2019, has become a genuine commercial engine. If you have flown Qatar Airways, United, British Airways, or Hawaiian recently and used in-flight Wi-Fi, there is a good chance you were already a Starlink customer at 35,000 feet, and that consumer and enterprise revenue funds the rockets rather than the other way around.

On top of that, the company folded Musk’s artificial intelligence startup xAI into the group earlier this year, along with the social network X. That combination is the key to understanding both the valuation and the frenzy, because investors are no longer buying a launch company, they are buying a bet on space, satellite internet, and AI bundled into a single company.

The proceeds from the IPO are all expected to contribute to expanding Starlink, scaling up AI computing resources, and funding technologies that do not yet exist, such as solar-powered data centres in orbit. The company recently unveiled AI1, its first compute satellite, repurposing Starlink’s existing power, cooling and laser-link technology into an orbiting AI platform, which gives you a sense of where management wants to take the story next.

No SpaceX discussion is complete without the Tesla angle, because the two companies are already financially entangled and the merger speculation is unlikely to go away. One common question is whether SpaceX is part of Tesla stock. It isn’t — Tesla and SpaceX are separate companies.

Tesla holds a stake in SpaceX after its earlier investment in xAI converted into SpaceX shares, and there is a school of thought that the two could eventually combine given the overlapping ambitions in AI, robotics and mobility. The counter-view is that two separately listed Musk companies risk competing for the same investor capital, which is one reason a tie-up further down the track cannot be ruled out.

It’s also worth noting that the S&P 500 cannot even consider SpaceX for at least a year after listing, but the Nasdaq 100 and Russell 1000 can add it within days, which could mean a wave of near-automatic buying at the index level.

Fun Fact: Musk’s fortune now stands at around USD$1.1 trillion on the Bloomberg Billionaires Index, more than three times that of the world’s second-richest person, and more than the entire GDP of Switzerland.

Competition, risks, and the Musk premium

In its core launch business, SpaceX does not really have a peer, which is precisely why it commands the position it does, but that dominance is also the source of the risk, because a valuation this large prices in success across several frontiers at once rather than just the one the company has already won.

SpaceX accounted for roughly four out of every five large rocket launches outside China and Russia in 2025, a level of dominance built on reusability that no rival has come close to matching. Its most direct heavyweight competitor is Blue Origin, the space company owned by Amazon founder Jeff Bezos, but its New Glenn rocket suffered a failure in early 2026 that only widened SpaceX’s lead. Smaller players like Rocket Lab have built solid niches launching smaller satellites, and Europe is now trying to engineer its own answer to SpaceX through a proposed Airbus-led satellite venture, which tells you just how uncomfortable its dominance has made the rest of the industry.

In connectivity, where Starlink sits, the competition is heating up far more quickly. Starlink is the clear leader with more than 10 million subscribers across more than 160 countries, but Amazon’s Kuiper network is a serious challenger, backed by Amazon’s balance sheet and distribution reach. Beyond Kuiper, a handful of smaller satellite players and the traditional telcos like Telstra and Vodafone are all defending the same broadband customers. This is the segment most exposed to genuine competition over the next few years, even as it remains the group’s profit engine today.

In AI, SpaceX is the underdog rather than the leader. Its xAI arm and Grok model sit behind the likes of OpenAI’s ChatGPT, Anthropic’s Claude and Google’s Gemini, and on compute it is fighting for the same enterprise budgets as far larger, better-capitalised players like AWS and Microsoft Azure. The difference, though, is that SpaceX is also a supplier to its rivals, having reportedly signed computing deals with both Anthropic and Google worth well over USD$1 billion a month each, a combined run-rate in the tens of billions a year, a reminder that the line between competitor and customer in AI is unusually blurred.

One area of risk comes from governance. Musk has near-total control of the business, and with his fortune now overwhelmingly tied up in his own companies, any attempt to sell down a stake could itself dent the value of the holding. Investors who lived through his 2022 Twitter purchase, the forced sale of Tesla stock and the drama over his pay package will know how that can weigh on a share price.

Another risk is SpaceX’s bottom line. While Starlink is already profitable, the company as a whole posted a net loss of USD$4.3 billion in the first quarter of 2026 as the AI and Starship investments run well ahead of their revenue, and at a USD$2.5 trillion market cap there is a long line of sceptics who think the valuation has outrun the business.

The Financial Health Check

The SpaceX stock price has moved quickly since listing, but the bigger question is whether the company can grow into its valuation.

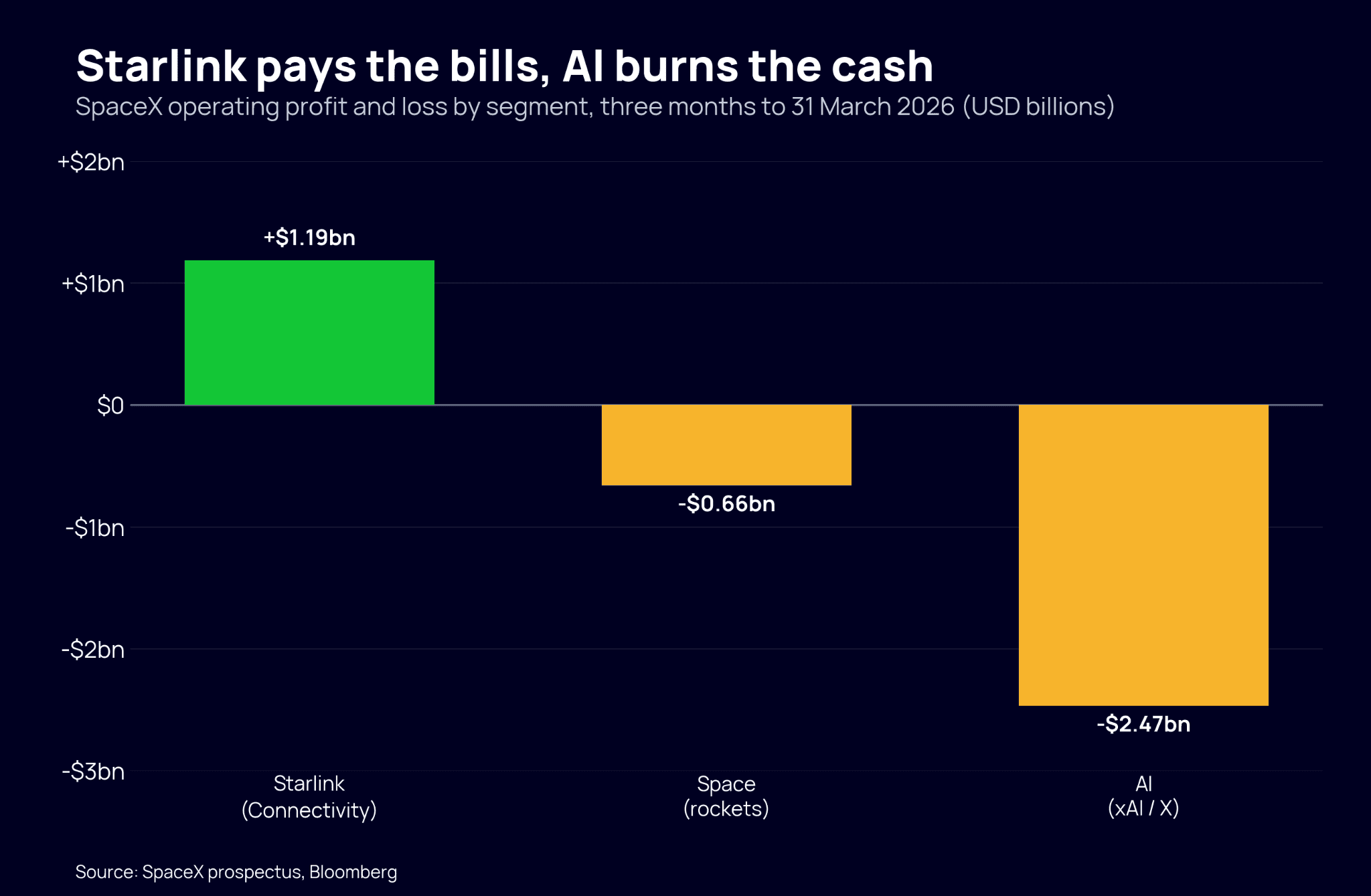

For the full 2025 year, revenue reached USD$18.7 billion, up 33% from USD$14 billion in 2024, so the top line is growing fast. In the most recent quarter ending March 31st 2026, SpaceX posted a net loss of USD$4.3 billion on revenue of USD$4.7 billion. That’s a hefty loss in the quarter and what’s interesting is where the loss is really coming from once you split the business into its three segments.

Starlink, sitting inside the Connectivity segment, is not the problem, it is the engine. It generated USD$3.3 billion of revenue in the quarter and, crucially, USD$1.2 billion of operating income, so the satellite broadband arm is already comfortably profitable at the operating level, with subscriber numbers more than doubling year on year.

The rocket business, the Space segment, brought in USD$619 million but ran a USD$662 million operating loss as the company poured money into developing Starship, the giant, fully reusable rocket designed to carry cargo and people to the Moon and Mars. Launching rockets isn’t cheap and a single Starship or Falcon failure can ground the fleet, something the regulator did after a mishap earlier this year.

It’s the AI segment, through xAI, where the red ink really shows up, with USD$818 million of revenue against a USD$2.5 billion operating loss, driven by GPU depreciation and the cost of building out data centre infrastructure.

Increasingly, SpaceX is being seen less as a rocket company and more as an AI company, with much of its future addressable market tied to AI compute rather than launch. Whether that excites you or worries you depends entirely on your view of that shift. One structural positive is that SpaceX secured investment-grade credit ratings ahead of the IPO, which lowers its borrowing costs and gives it room to fund its ambitions through debt rather than leaning entirely on equity.

Buy, Hold or Sell?

This information is general in nature and does not take into account your personal objectives, financial situation or needs. Consider whether it is appropriate for you before acting on it.

So, what are you actually buying? In one ticker, you are buying the company that dominates global rocket launch, a satellite network quietly turning a profit while connecting planes and homes around the world, and a frontier AI play that is burning billions to try to keep pace with much larger rivals. That is a genuinely unique combination, and it is why this listing has captured so much attention.

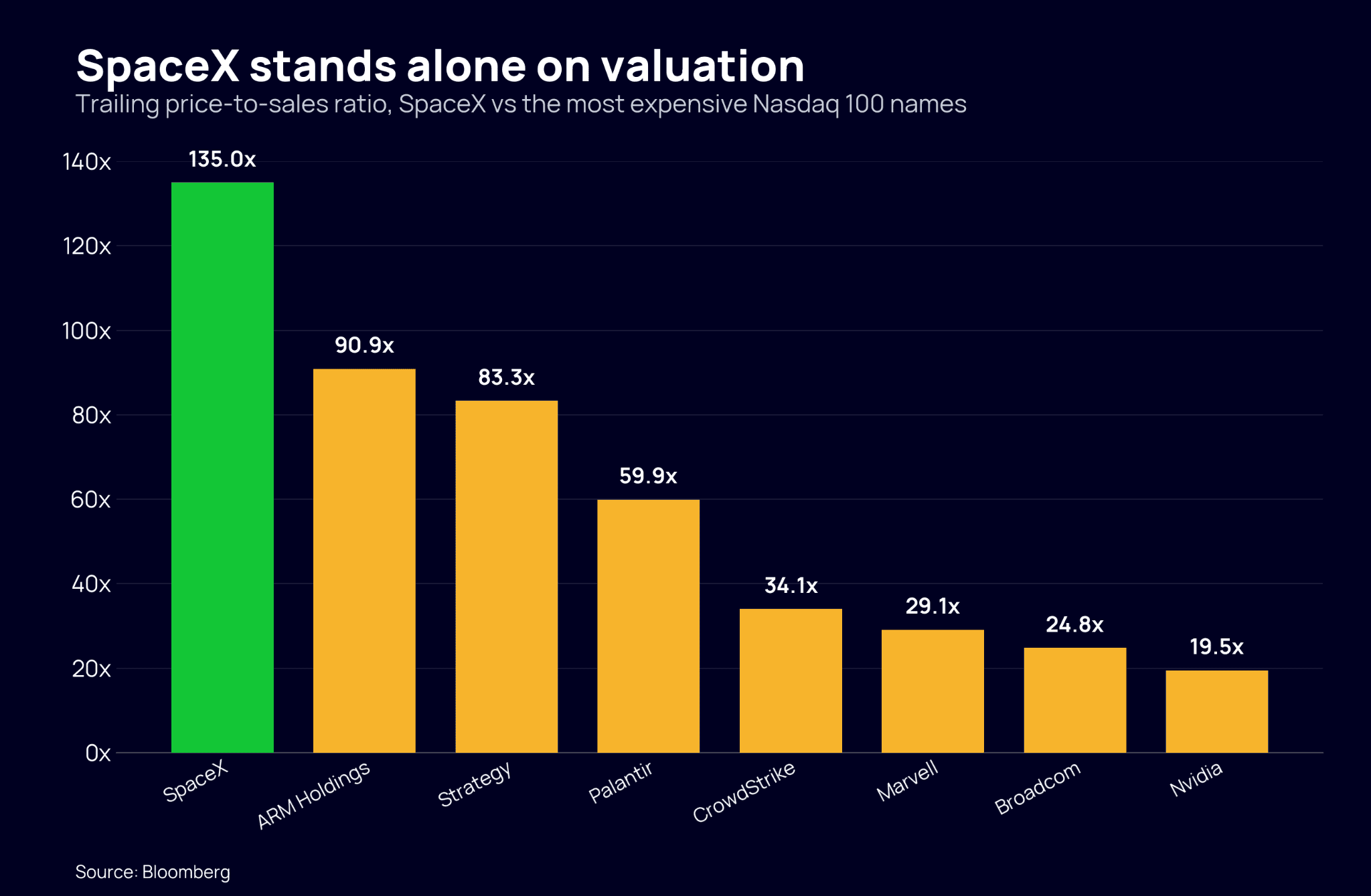

But it’s how much you have to pay for that combination which is worrying some investors. As it stands, SpaceX trades at around 135x trailing sales, putting it in a category of its own, above every other company in the Nasdaq 100, with the next-most-expensive name, ARM Holdings, at about 91x. Essentially, you’re not paying for what SpaceX earns today, you are paying for what it could become, and you’ve got to pay the Musk premium.

There are only around a dozen companies on earth worth a trillion dollars, almost all of them long-established and reliably profitable, and SpaceX is being valued above two trillion while still deep in the red. What to watch here is whether the next few quarters of public results show the beginning of growth into that valuation, or if the gap widens.

Then there is the lock-up to keep an eye on. Most insiders are restricted from selling for the first 180 days, which takes us to around December 2026, while Musk and the major backers are locked up for a full year, into mid-2027.

At more than two trillion dollars, you are being asked to back a business that is part rocket company, part internet provider, part AI moonshot, and very much driven by the eccentric vision of one man, who also happens to have the world’s biggest carmaker to run. Betting against Musk’s premium has been a losing trade for the better part of a decade, but a great company has never been the same thing as a great investment at any price. It’s been so far so good, but there are plenty of risks ahead, and the next few quarters of results will tell us whether the bulls or bears are right.

View SpaceX Shares

Past performance is not a reliable indicator of future performance. Your capital is at risk. This information is general in nature and does not take into account your personal objectives, financial situation or needs. Consider whether it is appropriate for you before acting on it.

*Data Accurate as of 18/06/2026

eToro Service ARSN 637 489 466 operated by eToro Asset Management Limited ABN 51 122 005 396 AFSL 319738 and promoted by eToro AUS Capital Limited ACN 612 791 803 AFSL 491139. Investing in shares via a managed investment scheme does not result in direct ownership of the underlying assets. The scheme has legal ownership, the investor has beneficial ownership, i.e. the shares are held on your behalf. As the scheme has legal ownership, you have no rights in the securities, including voting rights. Shares are non-transferable. Your capital is at risk. Refer to the Product Disclosure Statement and Target Market Determination (PDS and TMD) before transacting. See full disclaimer.