Summary

High dividend yield stocks set for a comeback

They are defensive to inflation and uncertainty. 2022 saw strong 9% dividend growth and record $1 trillion of US share buybacks. 2023 to be more muted as profit pressures rise, but still positive. Pay-out ratios are below average. Major payers, energy and banks, doing well. US share buybacks off to a strong start. Dividends are over half of total long term returns in many markets. We look to ‘make money while you sleep’.

A reality check for stock markets

Global stock markets saw a price fall reality check after recent big gains. Inflation expectations and bond yields continued to rise, as the EU and UK led global PMIs up. The US dollar hit a 7-week high. WMT and HD warned on the consumer outlook, whilst NVDA soared on its results and AI view. BHP, RIO, and INTC all slashed their dividends. See our 2023 Year Ahead HERE. See video updates, twitter @laidler_ben.

The next China catalyst

China and HK stock rally come off the boil. But is a marathon after years of under performance. The economy is reopening, valuations cheap, ‘two sessions’ looms. @ChinaTech.

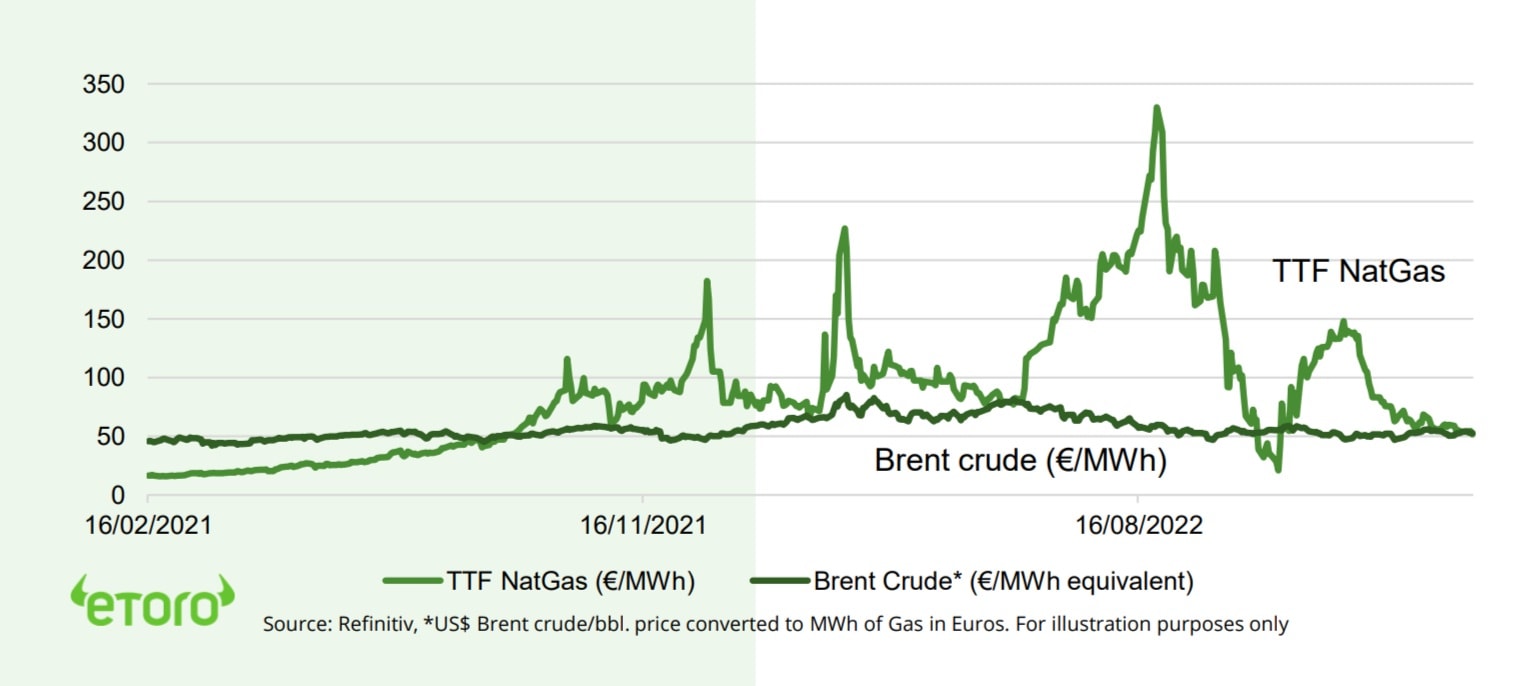

Europe’s gas price plunge has limits

EU natgas prices plunged 85% since peak. Been a huge relief to region. But prices need to stay ‘high-for-longer’ to incentivize demand savings and pull in LNG vs China re-opening.

Defence stocks back in the spotlight

Geopolitical risk has returned. Defence stocks have outperformed and valuations rerated. But growth rates have doubled and there is room for more, especially in Europe.

Coming voting season and investor activism

Attention shifts to annual general meeting proxy voting season. Focus dividend policy, executive pay, and ESG. Retail to vote more.

Crypto resilient to volatility

Bitcoin pullback after leading gains this year, as global markets volatility rose. DOT and LINK bucked the downtrend on strong development and adoption statistics. The world’s no.2 asset manager BLK launched an metaverse ETF. Whilst the BIS showed retail investors bought the 2022 crypto crash, whilst institutions sold.

Commodity pressures continue

Another down week with 7-week high dollar and rising bond yields. Oil fell on demand concerns and US natgas saw 2.5 year low $2.0/ MMBTU. Lower lithium a warning on China EV demand. Coffee up on supply risk in no.1 arabica producer Brazil. Big base metals stocks BHP and RTZ cut dividend on costs and lower iron ore.

The week ahead: Inflation, Tesla, month end

1) EU inflation (Thu) set for a 4th fall, and ECB minutes insight into 0.5% hiking pace. 2) China reopening pace with NBS and Caixin PMI. 3) CRM, AVGO, COST, BUD results and TSLA investor day (Wed). 4) Lacklustre February month end (Tue) and DAX and FTSE index change.

Our key views: A clear but gradual recovery

See gradual recovery with plenty bumps in road. The inflation and interest rate shock is slowly easing, and global recession risks have faded. Short term momentum to ease with sentiment less bad and bond yields higher. Focus cheap and defensive assets. Higher risk crypto, tech, small cap as inflation fall picks up.

Top Index Performance

| 1 Week | 1 Month | YTD | |

| DJ30 | -2.99% | -3.42% | -1.00% |

| SPX500 | -2.67% | -2.47% | 3.40% |

| NASDAQ | -3.33% | -1.95% | 8.87% |

| UK100 | -1.57% | 1.46% | 5.73% |

| GER30 | -1.76% | 0.39% | 9.24% |

| JPN225 | -0.88% | 0.33% | 5.21% |

| HKG50 | -3.43% | -11.81% | 1.16% |

*Data accurate as of 27/02/2023

Market Views

Modest reality check for stock markets

- Global stock markets saw a price fall reality check after recent big gains. Inflation expectations and bond yields continued to rise, as the EU and UK led global PMIs up. The US dollar hit a 7-week high. WMT and HD warned on the consumer outlook, whilst NVDA soared on its results and AI view. BHP, RIO, and INTC all slashed their dividends. See our 2023 Year Ahead View HERE.

The next China catalyst

- The China and HK stock rally has come off the boil. This is unsurprising after the dramatic c.60% October-January reopening rally, with local stocks now the ‘most crowded’ in BAML’s institutional investor survey. But we see this as an investing marathon not a short sprint, especially after a multi-year period of underperformance.

- Valuations are still low. The economic rebound is just starting. And March’s coming ‘two sessions’’ event a catalyst. This will show redoubled authorities effort to accelerate economy and support huge property sector. With impact from Germany to Australia, and luxury to commodities. @ChinaTech, @ChinaCar.

Europe’s gas price plunge has limits

- EU natgas prices plunged 85% since the summer. They are back to parity with Brent oil equivalent prices. This has delivered huge relief to region’s economic outlook and stoked its world-leading stock market performance. PMI’s have risen for four months, headline inflation similarly fallen, and many stock markets are at all-time-highs.

- But TTF natgas price is still three times 2020 levels and an economic drag. It needs to stay ‘high-for longer’. To incentivize demand savings and pull in LNG vs China re-opening. And Russia to potentially cut off its remaining EU flows.

Defence stocks back in the spotlight

- Geopolitical risk has returned. With anniversary of Ukraine invasion, Russia withdrawing from START nuclear deal, and China balloons over US. Defence stocks have strongly outperformed swooning stock markets in last year. And their valuations now trade at a 20-30% premium to the broader market.

- But these gains likely remain well supported. Global defence spending is now structurally rising at over double pre-2021 3% rates. With room for more as sluggish government arms procurement gradually cranks up, especially in Europe. Whilst the industry is benefitting from the cost cuts and consolidation of the recent leaner times.

Coming voting season and investor activism

- Q4 company earnings season is coming to an end. This shifts attention to upcoming annual general meeting proxy voting season. This will likely be focused on dividend policy, executive pay, and ESG. Newly more significant retail investors are a key actor. And one that has been under-represented by not voting as much as institutional investors.

- This comes against a backdrop of increased traditional investor activism, from Salesforce to Disney, and with ‘short-report’ writers taking on bigger stocks, like India’s Adani.

European NatGas and Brent oil equivalent price (€/MWh)

Crypto rally resilient to volatile markets

- Crypto assets saw a pullback, after their dramatic gains this year, and in the context of heightened equity market volatility and inflation concerns.

- Polkadot (DOT) and Chainlink (LINK), among the larger coins, both outperformed after showing strong development and adoption statistics.

- World’s 2nd largest asset manger Blackrock (BLK) launched a metaverse focused equity ETF (IVRS), bucking recently cautious mood on the theme.

- BIS published report showing that retail investors bought the sharp 2022 crypto asset correction, whilst institutional investors reduced positions.

Commodity pressures continue

- The asset class suffered another poor week, with the US dollar hitting a seven week high, and higher global bond yields raising demand fears.

- Energy commodities were lower on demand concerns and slow reopening of China. US natgas prices fell to a 2.5 year $2.0/MMBTU low. Lower lithium price a warning on China EV demand.

- Coffee prices rose near 10% on rising supply risks from no.1 Arabica bean producer Brazil.

- Leading base metals producers BHP (BHP) and RTZ (RIO) reported sharply lower Q4 results, on lower iron ore prices and cost inflation. This forced them to both slash their dividends.

US Equity Sectors, Themes, Crypto assets

| 1 Week | 1 Month | YTD | |

| IT | -3.09% | 0.49% | 9.37% |

| Healthcare | -2.86% | -3.88% | -4.96% |

| C Cyclicals | -4.27% | 1.33% | 11.42% |

| Small Caps | -2.87% | 0.26% | 7.34% |

| Value | -2.22% | -2.29% | -0.31% |

| Bitcoin | -6.50% | 1.11% | 40.45% |

| Ethereum | -5.72% | 0.00% | 35.08% |

Source: Refinitiv, MSCI, FTSE Russell

The week ahead: Inflation, Tesla, and month end

- Thursday’s Euro Zone inflation report is set to see a 4th decline from 8.6%. Is published same day as minutes of the last ECB meeting, with the central bank to keep its aggressive 0.50% hiking pace.

- Reopening Chinese economy to report Feb. NBS and Caixin PMIs. To show continued recovery momentum above breakeven 50-level. Comes ahead of key March 4/5 ‘two sessions’ meeting.

- Last week of ‘less bad’ US Q4 earnings includes CRM, AVGO,, ZM, COST, BUD. Plus TSLA investor day (Wed) with a focus on its new Cybertruck, Hardware 4.0, Nextgen platform, Masterplan 3.

- Tuesday is month end after a lacklustre February for many markets. DAX’s largest stock, Linde, to be replaced by Commerzbank, and in Stoxx50 by Intesa. Quarterly FTSE 100 rebalance announced.

Our key views: A clear but gradual recovery

- See gradual recovery with plenty of bumps in road. The US inflation and interest rate shock is slowly easing, and global recession risks faded with China reopening and plunged natgas. But short term equity market momentum to ease with investor sentiment now less bad and bond yields higher.

- Focus cheap and defensive assets, from high dividend yield, to healthcare, and UK. With higher risk crypto, tech, and small cap assets as the inflation fall picks up and de-risks markets. Overseas markets to lead the US. Commodities and the US dollar to take a performance back seat.

Fixed Income, Commodities, Currencies

| 1 Week | 1 Month | YTD | |

| Commod* | -0.92% | -5.43% | -6.43% |

| Brent Oil | -0.36% | -3.90% | -3.65% |

| Gold Spot | -1.80% | -5.69% | -0.66% |

| DXY USD | 1.35% | 3.27% | 1.68% |

| EUR/USD | -1.39% | -2.96% | -1.46% |

| US 10Yr Yld | 13.15% | 44.12% | 7.35% |

| VIX Vol. | 8.24% | 17.07% | 0.00% |

Source: Refinitiv. * Broad based Bloomberg commodity index

Focus of Week: Don’t forget the dividends

High dividend yield stocks set to come back into favour as market uncertainty continues

The high dividend yield investment style was the best 2022 performer, besting both equity and bond markets. But it has fallen out of favour in 2023. Firstly, as last year’s losers, from crypto to tech, led the ‘reversal rally’. Secondly, as rising profit worries stoked dividend sustainability concern, and rising bond yields increased dividend stocks competition. We see these high yield stocks as a core holding, and this underperformance an opportunity. Especially as we recently turned tactically more cautious. They are defensive to sticky inflation and an economic slowdown. And long-term they account for over 50% of total stock market returns in many markets. To quote Buffett, they allow you to ‘make money whilst you sleep’.

2022 saw strong global dividend growth, and record US buybacks, together totalling $2.6 trillion

Both dividends and share buybacks hit records last year. Global dividends rose to near $1.6 trillion, up 9%. This was led by the energy sector, and Asia. And was well ahead of the long term 5-6% growth trend. 90% companies increased or held steady their dividends. US share buybacks came in near a record $1 trillion.

2023 to see slower but still positive dividend growth, with pay-outs low and top payers resilient

Dividend growth will slow this year, in line with overall company profit pressures. But conservative pay-out ratios, at 50% globally, are below average and give a cushion to maintain or raise dividends even with these pressures. The biggest sector payers also remain well positioned. Energy is benefitting from high-for longer oil prices, and financials from rising interest rates. Emerging markets, Germany, and travel and leisure are forecast to lead dividend growth. Recent high-profile cuts are the outliers, representing sharply lower profits – from miners BHP (BHP) and RTZ (RIO) – or unique competitive challenges – like Intel (INTC).

The US stands alone in preferring share buybacks to return cash to shareholders

The US stands alone among markets in using share buybacks more than dividends to return money to shareholders. This is driven by their greater flexibility and tax efficiency. This has made US companies the traditional biggest buyers of US equities. Buybacks have got off to a surprisingly strong start to the year, with January announcements running at three times usual levels and despite the new 1% buyback tax.

Taking the long view. Dividends are over half your total stock market return

Reinvested compounding dividends have made up 40% of total US stock returns. This rises to over half in markets with higher yields. Some, like Germany’s DAX are total return indices. There are dividend focused ETFs like HDV, or smart portfolios like @DividendGrowth, which is a global set of 40 high dividend stocks.

S&P 500 Price Index vs Total Return Index (Reinvested Dividends, 20-years)

Key Views

| The eToro Market Strategy View | |

| Global Overview | Aggressive Fed interest rate hiking cycle and stubborn inflation boosted uncertainty, recession risk, and hit markets. We see this gradually fading in 2023, with global growth stressed but resilient, inflation pressure slowly easing, and valuations now more attractive. Focus on cheap and defensive assets for a gradual ‘U-shaped’ market recovery. |

| Traffic lights* | Equity Market Outlook |

| United States | World’s largest equity market (60% of total) seeing slowing but resilient GDP and earnings growth. Valuations led the market rout, and now at average levels, and are supported high company profitability and near peak bond yields. Focus on cash-flows defensives, like healthcare and high dividend. Big-tech supported by defensive growth. See gradual ‘U-shaped’ rebound as inflation slowly falls and de-risks market and tech/small cap/crypto appetite. |

| Europe & UK | Favour defensive and cheap UK (‘Economies are not stock-markets’) and continental European equities. Recession risk easing with lower natgas prices amd reopening China with still high ‘buffers’ of rising fiscal spending (defence and refugees) and still weak Euro (50%+ sales overseas). Even as ECB hikes aggressively. Equities cushioned by the lack of a big tech sector, and 30% cheaper valuations vs US. |

| Emerging Markets (EM) | China, Korea, Taiwan dominate EM (60% wt.), and more tech-centric than US. Positive on China as economy reopens, cuts interest rates, and eases tech regulation crackdown. Valuations 40% cheaper than US and market out of favour. Recovery helps global sectors from luxury to materials. Broader EM needs weaker USD and peak US rates catalyst. |

| Other International (JP, AUS, CN) | Canada and Australia benefit from strong equity market weight in commodities and financials, if global growth resilient and bond yields risen. Japanese equities among worlds cheapest but threatened by tightening monetary policy and stronger Yen with rising inflation and new BoJ governor. |

| Traffic lights* | Equity Sector & Themes Outlook |

| Tech | ‘Tech’ sectors of IT, communications, consumer discretionary (Amazon, Tesla), dominate US and China. Hurt by higher bond yields and above average valuations. But structural stories with good growth, high margins, fortress balance sheets support some. ‘Big-tech’ attractive new recession defensives. ‘Disruptive’ tech is much more vulnerable. |

| Defensives | More attractive as macro risks rise and bond yields better priced. Consumer staples, utilities, real estate attractive defensive cash flows, less exposed to rising economic growth risks, and robust dividends. Offset impact of higher bond yields. Healthcare most attractive, with cheaper valuations, more growth, some rising cost protection. |

| Cyclicals | Higher risk cyclical sectors, like discretionary (autos, apparel, restaurants), industrials, energy, and materials, are cheap and attractive if see a ‘slowdown not recession’ scenario. Are select but high risk opportunities from energy to financials stocks. With often depressed earnings, cheaper valuations, and have been out-of-favour for many years. |

| Financials | Benefits from high bond yields, charging more for loans than pay for deposits. Also one of cheapest P/E valuations, and with room for large dividend and buyback yields. But can be outweighed by high recession risks, with lower loan demand and higher defaults. Banks most exposed. Insurance and Diversifieds (like Berkshire Hathaway) the least. |

| Themes | We favour Value over Growth on GDP resilience, lower valuations, rising bond yields, under-ownership after decade under-performance. Dividends and buybacks recovering with cash flows. Power of dividends under-estimated, at up to 1/2 of total long term return. Secular growth of Renewables and Disruptive Tech investment themes. |

| Traffic lights* | Other Assets |

| Currencies | USD ‘wrecking ball’ driven by Fed interest rates and ‘safer-haven’ bid. DM currencies hurt by still low interest rates and struggling growth. Strong USD hurt EM, commodities, US foreign earners like tech. But helps big EU and Japan exporters. See a stabler USD outlook in 2023 as near top of the Fed cycle and global risks remain high. |

| Fixed Income | US 10-yr bond yields supported around 4% by higher Fed rate hike and stickier inflation expectations. Set to ease as recession risks slowly build and inflation expectations gradually fall. US has wide spread to other market bond yields, and headwinds of high debt, poor demographics, and low productivity. 5% bill yields an attrative cash alternative. |

| Commodities | Strong USD and rising recession fears hit commodities. But still above average prices helped by GDP growth, ‘green’ industry demand, supply under-investment, recovering China, Russia supply crisis. Oil helped by slow return of OPEC+ supply and Russia 10% world oil supply problems. But commodities not to repeat their 2022 performance leadership. |

| Crypto | Potential ‘surpsise’ after dramatic and early asset class sell-off and later specific risk events from Luna to FTX. See long term asset class development with small size $1 trillion, correlations low, regulation growing, development/catalysts continuing – Ethereum merge to proof-of-stake and coming BTC halving. |

| *Methodology: | Our guide to where we see better risk-adjusted outlook. Not investment advice. |

| Positive | Overall positive view, and expected to outperform the asset class on a 12-month view. |

| Neutral | Overall neutral view, with elements of strength and weakness on a 12-month view |

| Cautious | Overall cautious view, and expected to underperform the asset class on a 12-month view |

Source: eToro

Analyst Team

| Global Analyst Team | |

| CIO | Gil Shapira |

| Global Markets Strategist | Ben Laidler |

| United States | Callie Cox |

| United Kingdom | Adam Vettese Mark Crouch Simon Peters |

| France | Antoine Fraysse Soulier David Derhy |

| Holland | Jean-Paul van Oudheusden |

| Italy | Gabriel Dabach |

| Iberia/LatAm | Javier Molina |

| Nordics |

Jakob Westh Christensen |

| Poland | Pawel Majtkowski |

| Romania | Bogdan Maioreanu |

| Asia | Nemo Qin Marco Ma |

| Australia | Josh Gilbert |

Research Resources

Research Library

eToro Plus: In-Depth Analysis. Dive deeper into market insights: Read daily, weekly and quarterly summaries, catch up on the latest market trends and get the most recent, in-depth overview of markets.

Presentation

Find our twice monthly global markets presentation on the multi-asset investment outlook.

Webinars

eToro CLUB members can join our live Weekly Outlook webinars every Monday at 1pm GMT. Also see the other online courses and webinars.

Videos

Subscribe to our timely video updates on market moving events, and the ‘week ahead’ view

Follow us on twitter at @laidler_ben

COMPLIANCE DISCLAIMER

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.