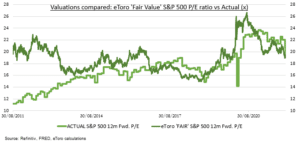

LESS-BAD: The S&P 500 January sell-off, combined with the continued solid earnings outlook, has cut valuation and therefore market risks. The forward price/earnings (P/E) valuation is down 10% to under 20x, and 25% from its 2020 high, as Fed turns hawkish. P/E’s are still above the five (18.5x) and ten-year (16.7x) averages, as they should be. Company profitability is near records and bond yields low. Our ‘fair value’ P/E ratio (see chart) supports this, at over 19x. We focus on cheaper sectors and overseas markets, for re-rating upside and protection from valuation pressures, and are positive markets.

FAIR-VALUE: We use 10-year bond yields, corporate profitability, and long-term GDP growth forecasts to estimate a ‘fair value’ S&P 500 (SPY) P/E. Its 19x is high vs history but close to current level. We see gradually higher bond yields part offset by still high corporate profitability and GDP. A 0.5% higher 10-year bond yield cuts our P/E by 10%. A return to the long-term GDP outlook a decade ago (2.6% vs 1.9%) would raise it 20%.

DOUBLE-FOCUS: We focus on cheaper sectors and markets. They have the most room for valuations to rise. They are also an ‘insurance’ to further valuation pressures, as central banks turn more hawkish. Energy (XLE) and financials (XLF) are the two cheapest global sectors. Whilst Europe (EZU), UK (ISF.L), and China (MCHI) are on near record 30-45% P/E valuation discounts to the US. Big tech FAANGM’s offer strong value within tech, with their decent growth, big ‘moats’, and fortress balance sheets.

All data, figures & charts are valid as of 01/02/2022