Do you know how much time you spent watching TV this past week? I’ll tell you precisely. You spent two hours a day just on Netflix, and probably some more on YouTube too. Most companies can do one of two things well. They can grow fast, or they can make a lot of money. Doing both, year after year, is rare. The way Netflix manages the battle for your attention is the reason I am not just a long-time subscriber, but a long-time shareholder too.

How does Netflix do it? It has one of the deepest customer lock-in effects in the world. Netflix raises its prices. Subscribers grumble, a few cancel, and then almost all of them stay, because for the money there is nothing else like it.

The company takes that money and reinvests it into making the platform more valuable with more content, and that allows it to raise prices again in a virtuous cycle. Then it does it again the next year.

This translates beautifully to operating metrics. Operating margin has gone from 27% to nearly 30% to a guided 31.5%, roughly two points a year, three years running. That is pricing power and operating discipline working together, and it is the heart of why I think Netflix is a quality business. But there is a key question that is scaring investors away. Netflix guided for lower revenue growth this year than the year before.

If growth is slowing from its golden era, does the stock price reflect a future that is no longer real?

After Netflix’s recent fall, I believe it does. But it’s not that simple.

If you find this kind of analysis useful, consider subscribing. I publish new posts every week.

What Netflix Actually Does

Netflix sells entertainment. To be precise, it sells streaming entertainment to more than 325 million paying households, reaching an audience approaching a billion people. You pay a monthly fee, you get a vast library of films and series in dozens of languages, and increasingly you can pay less if you accept some ads.

The money comes in three ways.

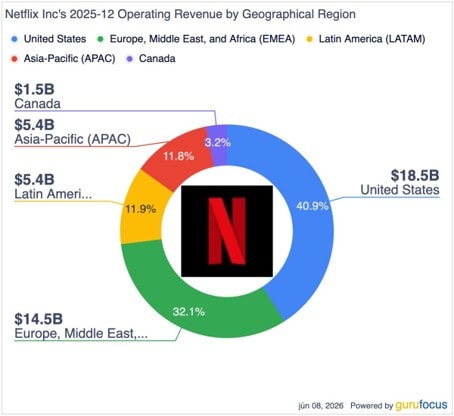

Most of it is subscriptions, split across four regions: the US and Canada (the biggest by revenue), Europe (the biggest by members), and the faster-growing Latin America and Asia-Pacific.

The second stream, still small but growing fast, is advertising on the cheaper ad-supported plan. The third, newer still, is live events: NFL games, big boxing matches, the World Baseball Classic, weekly WWE.

Did the number at the beginning shock you? It’s true. The average member watches about two hours a day, and in late 2025 Netflix reached its highest-ever share of TV time in the US, at 8.6%. This shows how fierce the competition for your attention is, and it also shows how much runway Netflix has ahead of it.

Why I’m Writing About Netflix Now

Netflix was enjoying a massive bull run, but that all changed with a surprising management decision. The usually prudent, underpromising and overdelivering management tried to acquire WBD, a legacy movie studio with massive real-world assets. Exactly the kind of firm Netflix has been putting out of business.

Investors punished the company immediately. The stock fell from $130 to $75. The bull thesis looked broken. Until something unexpected happened. Paramount joined the fight, and eventually won the bidding war and acquired WBD.

The result? Not only did Netflix walk away from an unpopular acquisition, but it also received a $2.8 billion break-up fee. The question is, now that the elephant in the room has been addressed, what is still keeping the stock price depressed?

Netflix is quietly shifting its narrative. It used to be a subscriber-growth story. In 2025, Netflix stopped reporting that number entirely. It was clear Netflix wanted to redefine itself, and for investors to look at revenue, profit, and engagement as the platform matured and had to pivot to pricing and supplementary business lines to drive results, not just subscriber growth. That means growth now comes as much from raising prices and scaling ads as from adding members. The ad business doubled in 2024, grew about two and a half times in 2025, and is targeted to roughly double again to around $3 billion in 2026.

The Numbers That Matter

Revenue grew about 16% in 2025 to $45 billion, and is guided to roughly $51 billion in 2026. That is slower than Netflix’s hypergrowth past, but it is on a much bigger base. What matters is that Netflix has been consistently expanding its margins.

Netflix is also good at generating cash. Free cash flow went from about $6.9 billion in 2024 to about $9.5 billion in 2025, up 37%. Almost all of that cash goes toward buying back stock.

The Moat

Netflix’s competitive advantage comes from its sheer scale of content. Pricing power is the proof. Netflix can raise prices even in a weaker consumer environment because, for the money, it delivers the most entertainment per hour. That gap between value and price is the moat.

The other moat mechanism is scale. Netflix spreads a content budget of roughly $16 billion across 325 million households. That lets it both outspend competitors on hits and still expand its margin. Better economics bring better content, which drives engagement, which funds more content.

Is the moat durable? I think Netflix can widen its content moat, but it is contested on total attention share, where it competes not only with YouTube but also with other platforms like Disney+ and Prime Video.

The Competitive Landscape

The streaming industry, with Disney, Amazon, Apple, and the newly merging legacy players, poses a real threat. But thanks to a years-long first-mover advantage, Netflix has entrenched itself across the majority of the addressable market.

Netflix has to win on content breadth, because its competitors have inherent advantages on quality, such as Disney movies and HBO shows. But so far, the company has managed this well.

Dividends & Buybacks

Netflix does not pay a dividend, by choice, and has been clear it has no plans to start. Instead it returns essentially all of its free cash flow through share repurchases: about $6.3 billion in 2024 and $9.1 billion in 2025, steadily shrinking the share count. With free cash flow growing and a $2.8 billion one-time fee in the bank, I expect the buyback to continue.

Bull Case / Bear Case

The Bull Case

The bull case assumes Netflix would compound on every axis at once. It would grow revenue in the mid-teens, continue raising prices while keeping retention steady, scale the high-margin ad business, and expand operating margin further on better cost economics. The bull’s honest risk is price: the quality is well known.

The Bear Case

The bear case rests on growth expectations. Netflix’s valuation rests on the assumption that it will be able to grow and expand margins. There is already a slowdown in revenue growth, and since Netflix stopped reporting subscriber numbers, we can deduce that subscriber growth is probably slowing too. However, at this price, Netflix is priced for low single-digit growth, something I consider unlikely.

If you know someone who’d find this useful, sharing goes a long way.

Valuation & What the Street Thinks

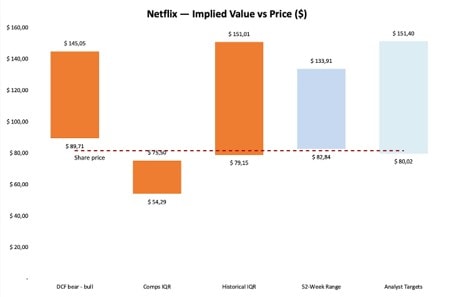

Netflix has historically traded at a premium valuation, which is why looking purely at historical valuation can be misleading.

I value portfolio companies based on three lenses. The historical valuation, if one were to expect the firm to revert to its long-term median. The peer valuation, looking at how the market values similar companies, adjusted to reflect the interquartile range to strip away extremes. And a custom DCF model, where I model the financials against my expectations of future performance.

I use Wall Street analyst targets and the 52-week trading range as a sanity check.

As you can see, Netflix is now trading at the low end of its historical valuations, analyst estimates, and its trading range.

Its peers trade cheaper, but the reason is that Netflix lacks real pure-play streaming peers to compare against. My DCF valuation suggests a floor of $90 if the business continues to perform in line with expectations.

In investing, it is important to use a margin of safety, and for a higher-risk name like Netflix, I like that margin to be 20% below fair value. That brings us to a fair value estimate of $101, representing a 24% upside from the current price.

The downside I would consider a real risk is a reversal to the $75 support, where I would revisit the thesis.

From a quick technical perspective, Netflix is currently sitting at an important support level. If this breaks, we can expect another down leg to $75, at which point, if the thesis and the economy have not shifted dramatically, I would consider adding significantly.

Netflix has already shown it has the momentum to recover toward a more reasonable price, but that fizzled out after the latest earnings report.

My Take

I recently bought more Netflix stock. It currently makes up around 7% of my portfolio. Netflix has what I look for: a strong business, pricing power, and a management team that likes to underpromise and overdeliver.

On the downside, I would reassess my thesis if margin expansion stalls or a price increase finally drives subscribers away.

Bottom Line

Netflix grows in the mid-teens, raises prices without losing customers, expands its margins every year, and generates close to $10 billion in cash it hands back to shareholders. The business is firing on every cylinder. The only real debate is what it is worth. Whether it belongs in your portfolio depends on the price you pay and your time horizon, but I think the machine itself is worth keeping an eye on.

I share all my moves in real time on eToro, where over 1 500 investors follow my portfolio. If you’re curious how this fits into the bigger picture, come find me there: https://www.etoro.com/people/thedividendfund

Thanks for reading R² Investment Club! Subscribe for free to receive new posts and support my work.