Summary

Focus: The green commodities boom

An accelerating carbon-transition is supporting higher-for-longer commodity prices. Demand for ‘green’ metals, from cobalt and lithium, to copper and nickel, is forecast to surge four-fold, and ultimately rival the size of the oil market. We look at the example of uranium. China is to build 150 reactors as part of its net-zero plan, but world mine supply is 25% below demand today. See the physical commodities, and related equities from Cameco (CCJ) to Albemarle (ALB), or broad @RenewableEnergy, QCLN, and LIT.

Markets resilient to surging inflation

Equity markets resilient to stubborn inflation. US prices rose 6.2% last month, a 30-year high. This boosted US 10-year bond yields, USD, bitcoin (to new high $69,000) and long-suffering gold. But also saw tech stock performance take a back seat to cheaper commodity and defensive sectors. See our latest presentation here.

The ‘everything’ rally lives on

We see more profit surprises ahead, and still low bond yields supporting high valuations. History shows 1, 3 and 12-month S&P 500 returns after new highs are all positive. A key support is the wide market ‘breadth’. This everything rally is not just in the US, but global, and a key change versus the tech-led 2020 rally.

What the huge Rivian Auto IPO tells us

The huge IPO of electric SUV maker Rivian (RIVN), reflects the booming EV outlook. Industry volumes are seen rising at least 12x by decade end. Tesla (TSLA) has shown record 30% profit margins are possible. The race to be ‘next Tesla’ is well underway and increasingly happening in publicmarkets. See @Driverless.

China ‘Singles Day’ sales relief

Sales up 16% to $133 billion a relief for Alibaba (BABA) and JD.com (JD US). Reduces concern on consumer health and limits to 50% ecommerce penetration. See @ShoppingBasket.

New bitcoin high. Asset class nears $3 trillion

A good week. Bitcoin saw a new all-time-high $69,000 and asset class nears $3 trillion market capitalisation milestone. Bitcoin taproot upgrade is imminent and positive. Litecoin (LTC) and Algorand (ALGO) led major coin performance. AMC Cinemas now takes crypto. eToro added 4 new coins: SUSHI, $CHZ, AXS, QNT.

Gold back from the doldrums

Commodities firm despite a surging USD. We see a continued asset class ‘sweet spot’. Gold rebounded from its weakness this year as inflation concerns rose. Wheat was boosted by potential Russia export restrictions.

The week ahead: Retail in spotlight

1) US retail sales is in focus as enter the holiday spending season. October growth is seen strong at +12% versus last year. 2) Retail, tech, and music stocks set to wrap up a strong Q3 earnings season in US. Walmart (WMT), Home Depot (HD), GPU-chip Nvidia (NVDA), music label Warner (WMG), and China’s Alibaba (BABA).

Our key views: All eyes on inflation

We see a positive outlook of 1) vaccine rollout and economic re-opening, and 2) still huge policy support. A more aggressive Fed is the risk, with inflation a lot less ‘transitory’ than hoped. But markets already pricing two hikes next year. We like equities, commodities, crypto, and are cautious fixed income, and the USD.

Top Index Performance

| 1 Week | 1 Month | YTD | |

| DJ30 | -0.63% | 2.28% | 17.95% |

| SPX500 | -0.31% | 4.73% | 24.67% |

| NASDAQ | -0.69% | 6.47% | 23.06% |

| UK100 | 0.60% | 1.57% | 13.74% |

| GER30 | 0.25% | 3.25% | 17.31% |

| JPN225 | -0.01% | 1.86% | 7.89% |

| HKG50 | 1.84% | -0.01% | -6.99% |

*Data accurate as of 15/11/2021

Market Views

Markets resilient to surging inflation

- Equity markets consolidating after strong gains, with the S&P 500 +8% from October lows. They have been resilient to stubbornly high inflation. US prices rose 6.2% last month, a 30-year high rate. This boosted US 10-year bond yields, the USD, bitcoin (to a new high $69,000) and long suffering gold. This also saw recent strong tech stock performance take a back seat to cheaper materials and defensive sectors. Tesla (TSLA) fell on Musk’s stock sale and Disney (DIS) on poor results. See our latest presentation here. Also, REGISTER for our year ahead webinars.

The ‘everything’ rally lives on

- Equities have set new records and been resilient to higher inflation. We are positive the fundamentals, seeing more profit surprises ahead, and still low bond yields supporting high valuations. History shows 1, 3 and 12-month S&P 500 returns after new highs are all positive.

- A key support is the market ‘breadth’. This everything rally is not just in the US, but global, and a key change versus the tech-led 2020. This reflects the broad GDP rebound, and has more to go. Near all countries and industries are still seeing positive upward earnings revisions.

What the huge Rivian Auto IPO tells us

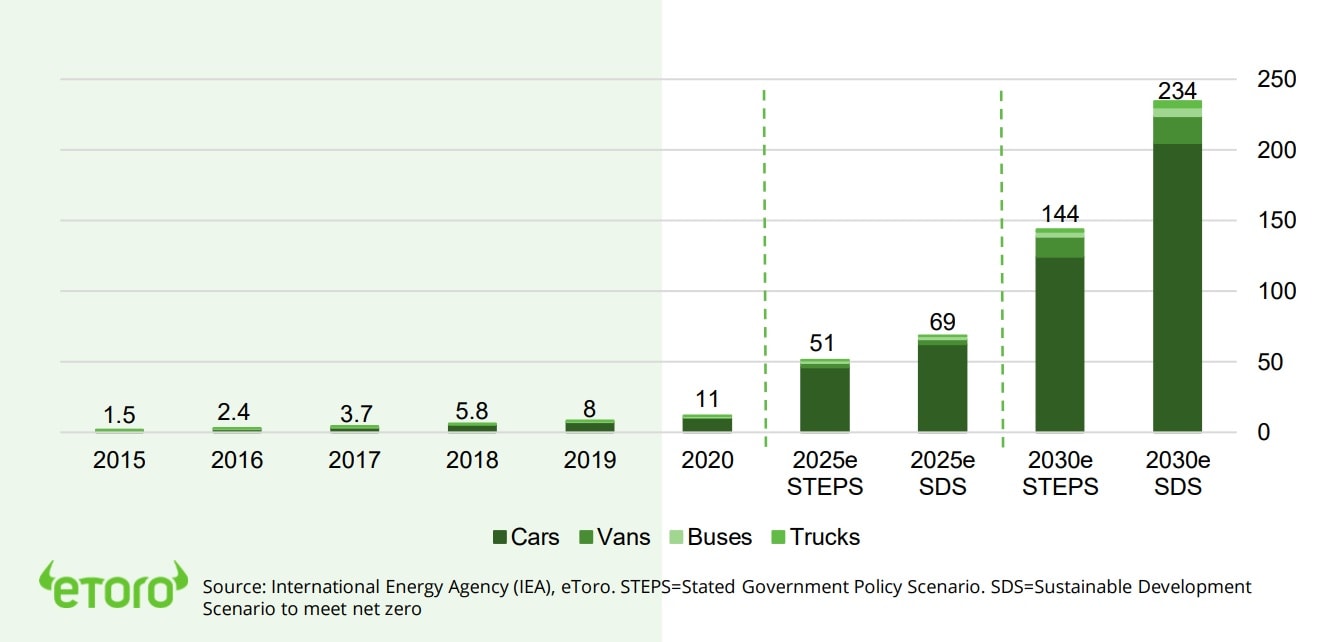

- Last week saw the year’s biggest IPO, of electric SUV maker Rivian (RIVN). The c.$100 billion valuation reflects the booming EV outlook. Industry volumes are seen rising at least 12x by decade-end (see chart). Tesla (TSLA) has shown record 30% profit margins are possible.

- Rivian also shows a broader target market, big name partners, and ‘democratised’ IPO offering. Along with recent IPO of Lucid (LCID) the race to be ‘next Tesla’ is well underway and increasingly happening in publicmarkets. See @Driverless.

A strong ‘singles day’ provides relief

- China’s 13th annual Singles Day shopping event is the world’s largest, and was bigger than ever. Sales by Alibaba (BABA) and JD.com (JD US) rose 16% to $133 billion. Despite a slowing Chinese economy and a government focused on less ostentatious ‘common prosperity’ agenda.

- Such a strong singles day was a relief to concerns over the Chinese consumer, the limits of ecommerce penetration (already at 50% in China, twice the global average), and a catalyst for depressed Chinese and global e-commerce stocks. See @ShoppingBasket and @ChinaTech.

The rise of the female CEO

- The number of female investors is growing faster than men. They invest differently, and often do better. The same is true for female CEO’s. The percentage of large US companies run by women has risen from under 1% two decades ago to over 8% today. Whilst a clear improvement, this is still very low. Today’s female CEO’s range from Mary Barra at General Motors (GM) to Jane Fraser at Citigroup (C).

- Similarly low levels can be seen globally, in UK and Germany. But stock exchange, regulatory, and investor pressures are all now combining to drive an acceleration. This is good. There is plenty of evidence female led companies and more diverse leadership helps performance.

World electric vehicle sales and projections* (millions, units)

New bitcoin high as asset class nears $3 trillion

- Another good week from crypto-assets in the seasonally strong fourth quarter, as close in on the $3 trillion overall market cap. milestone. Bitcoin (BTC) set a new all-time-high, breaking $69,000 for the first time. Litecoin (LTC) and Algorand (ALGO) led top-20 coin gains as alt coins continue to catch up with bitcoin highs.

- Bitcoin (BTC) is set to see its taproot upgrade imminently, its first major upgrade in four years. This will improve both efficiency (lower fees and better smart contract functionality) and privacy, and likely broaden its appeal.

- eToro added 4 new coins, taking the total to 40. 1) automated market maker SushiSwap (SUSHI), 2) sports and entertainment Chiliz ($CHZ), 3) blockchain video-game Axie Infinity (AXS), and 4) blockchain operating system Quant (QNT).

Gold and wheat in the performance spotlight

- Commodity prices were firm, despite a resurgent USD. Commodities are USD-priced, so a stronger USD makes them pricier for many, cutting demand. Wheat prices saw strong gains, and are now +25% this year. Biggest exporter Russia is expected to increase export taxes, to cut exports and better supply the localmarket.

- Gold woke from its negative price performance this year as inflation worries resurfaced. Gold performed well in the 1970’s ‘stagflation’ but has done poorly in less-extreme environments.

- We see commodities asset class well-supported by robust demand, tight supply, and more demand from investors looking for more diversification or increased inflation-protection.

US Equity Sectors, Themes, Crypto assets

| 1 Week | 1 Month | YTD | |

| IT | 0.37% | 9.68% | 27.88% |

| Healthcare | 0.02% | 5.94% | 15.05% |

| C Cyclicals | -2.91% | 9.27% | 20.69% |

| Small Caps | -1.04% | 7.94% | 22.12% |

| Value | 0.23% | 5.62% | 21.90% |

| Bitcoin | 5.19% | 15.19% | 123.05% |

| Ethereum | 4.35% | 33.73% | 522.46% |

Source: Refinitiv

The week ahead: Retail trends in spotlight

- US retail sales (Tue) focus as enter the seasonally strong Christmas season. October growth seen +0.7% versus last month, and still seen up a huge +12% versus last year.

- Retail, tech, and music wrap up third quarter earnings. See Walmart (WMT), Home Depot (HD), chipmaker Nvidia (NVDA), no.3 music label Warner (WMG), China’s Alibaba (BABA).

- The Los Angeles auto show, one of the world’s largest, starts Friday. Will include EV pioneers like SOLO and FSR, and new electric offerings from legacy autos like F and VOW3.DE.

Our key views: All eyes on inflation

- A positive scenario of 1) global vaccine rollout and economic re-opening, 2) still large support of low interest rates and fiscal spending.

- The main risk is Fed policy tightening, with inflation pressures broadening and proving less ‘transitory’. But markets are already pricing at least two US interest rate increases next year. We see Fed moving slowly and transparently.

- We focus on cyclical assets that benefit most from the rebound: commodities, crypto, small cap, and value. We are more cautious on fixed income, the USD, defensive equities and China.

Fixed Income, Commodities, Currencies

| 1 Week | 1 Month | YTD | |

| Commod* | 0.06% | -1.84% | 31.70% |

| Brent Oil | -0.73% | -3.50% | 58.45% |

| Gold Spot | 2.62% | 5.63% | -1.78% |

| DXY USD | 0.85% | 1.24% | 5.77% |

| EUR/USD | -1.06% | -1.33% | -6.31% |

| US 10Yr Yld | 11.32% | -0.84% | 64.74% |

| VIX Vol. | -1.15% | -0.06% | -28.40% |

Source: Refinitiv. * Broad based Bloomberg commodity index

Focus of Week: The green commodities boom

Higher-for-longer commodity prices, supported by accelerating carbon transition

Commodities are seeing one of their sharpest and broadest rallies in over a decade. The broad-based Bloomberg commodity Index is up 32% this year, second only to crypto among asset classes. We see prices remaining high for an extended period given the rare ‘sweet spot’ of stronger demand, tight supply, and rising investor demand as inflation stays high. This will help individual commodities, including the 13 on the eToro platform, and support energy and materials equities. The growing impact of the carbon transition is a key difference in this rally and will be further boosted by the COP 26 net zero commitments. This is raising multi-decade demand for ‘green-transition’ metals and cutting supply for fossil fuels.

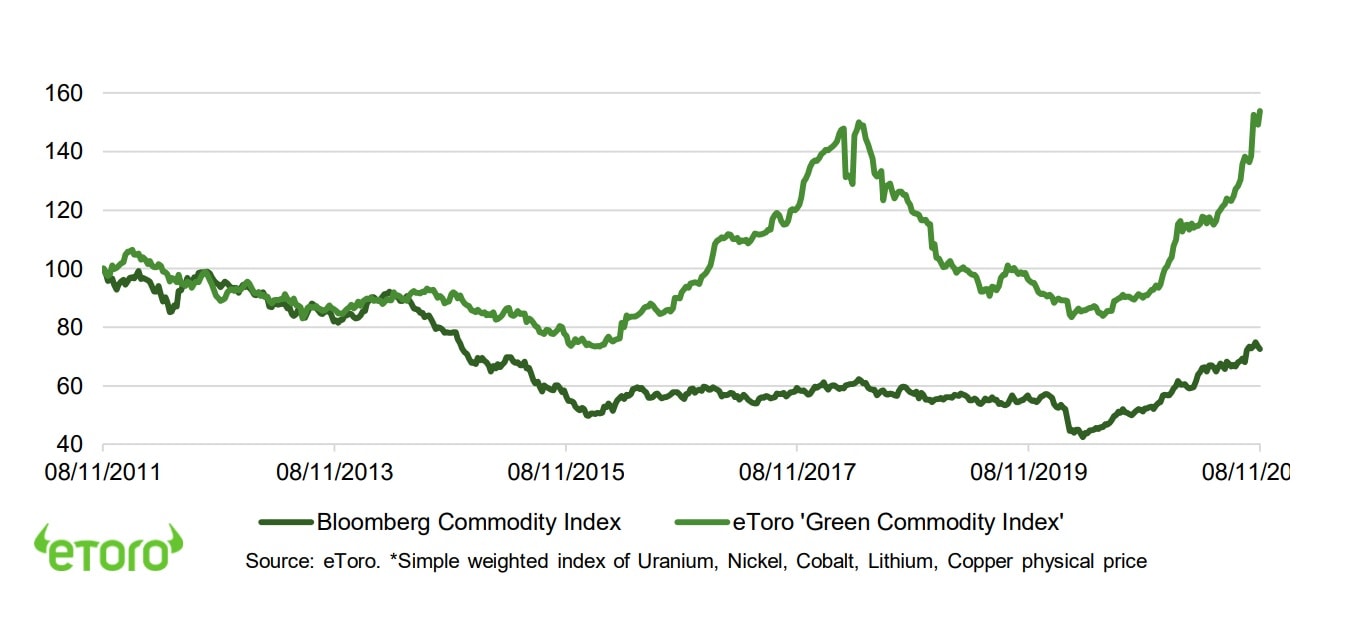

To rival the size of the oil market? The eToro ‘green-transition’ commodity index

We create a simple-weighted basket of five key commodities used in the carbon transition: lithium, nickel, and cobalt (for batteries), uranium (nuclear power), and copper (cabling). This index has dramatically outperformed broader commodity markets both long and short term (see chart). The IMF estimates these metals as a key bottleneck in the move to net-zero emissions, with prices set to stay high for a decade. The overall value of these generally ‘niche’ metals is seen rising four-fold over the next two decades to rival the size of the oil market. Of the five, only lithium is seen with relatively easily added supply. Electric vehicle units are seen growing at least 12-fold this decade, and each needs five times more of these metals than a conventional car. China alone is pledging 150 new reactors in the next 15 years to meet its net-zero goals.

The uranium example of strong reactor and investor demand, but tight supply

Uranium’s dominant use is as fuel for nuclear power reactors which is seeing a re-appraisal as part of the solution to getting to net-zero. It has no carbon emissions, is constant unlike wind or solar, and time tested, making up 10% of global electricity production. A 40% nuclear power plant expansion is underway, led by China and India. Investor access has also recently improved with the launch of the Sprott Physical Uranium Trust, that is also boosting prices with its buy-and-hold strategy. Low historic prices have cut exploration and supply. Mine production is 25% below reactor demand now, and highly concentrated in Kazakhstan, Australia, and Namibia. Prices are up 50% this year but remain a fraction of 2007 peak levels.

Investments through the physical or related equities. Cameco to Albemarle and Glencore

Physical copper and nickel commodities are widely traded, and indirect exposure is available through leading producer equities like Vale (VALE) and Norilsk (MNODL.L) for nickel, and BHP (BHP), Freeport (FCX), and Antofagasta (ANTO.L) for copper. The other commodities are less directly traded, with the focus on indirect exposed equities, like Cameco (CCJ) for uranium, Glencore (GLNE.L) for cobalt, or Albemarle (ALB), Livent (LTHM) and SQM (SQM) for lithium. Broader exposure is possible via smart portfolio @RenewableEnergy, and the QCLN green energy or LIT lithium and battery tech exchange traded funds.

‘Green commodities’* versus all-commodity index (10-years)

Key Views

| The eToro Market Strategy View | |

| Global Overview | Positive scenario of 1) global vaccine rollout and economic re-opening, 2) support from low interest rates and government spending. Main risk is from US Fed monetary policy tightening, but will be well-signalled and very gradual. Economies are increasingly resilient new virus case ‘waves’. Focus on most growth sensitive assets: equities, commodities, crypto, small cap and value. Relative caution on fixed income, USD, defensive equities and China. |

| Traffic lights* | Equity Market Outlook |

| United States | World’s largest equity market (55% of total) seeing strongest GDP recovery in 30-years driving earnings upside ‘surprise’, and a rare third consecutive year of 10%+ equity market returns. Valuations at 21x P/E are 25% above historic levels but supported by still low bond yields and strong earnings growth outlook. See further cyclicals and value catch-up, after a decade of underperformance, whilst tech is well supported by its structural growth outlook. |

| Europe & UK | Latest to benefit from vaccination surge and much more economic re-opening to go. Equity markets helped by 1) a greater weight of cyclical sectors, and lack of tech, 2) 25% cheaper valuations vs US, 3) decade of under performance made under-owned by global investors. A robust EUR a help for investors, as is multi-year €750bn ‘Next Generation’ fiscal support. With 50%+ company revenues from overseas is exposed to global trends. |

| Emerging Markets (EM) | China, Korea, Taiwan dominate EM, with 60% weight, and is more tech-centric than US. China equities hurt by tech regulation crackdown, property sector debt, and slower GDP growth. But this is increasingly well-priced. LatAm and Eastern Europe have more upside to global growth recovery, a weaker USD, and higher commodities. |

| Other International (JP, AUS, CN) | Canada and Australia benefit from strong equity market weight in commodities and financials, as global growth rebounds and bond yields set to rise. Japanese equities among cheapest of any major market and vaccination rates accelerating, but has structural headwinds of low GDP growth, an ageing population, and world’s highest debt. |

| Traffic lights* | Equity Sector & Themes Outlook |

| Tech | The broad ‘tech’ sector of IT, communications, and parts of consumer discretionary (Amazon, Tesla), dominates US and Chinese markets. Expect a more subdued 2021 after dramatic 2020 rally. But are structural stories with good growth, high profitability, and clean balance sheets that justify high valuations, and should continue to rise. |

| Defensives | Healthcare, consumer staples, utilities, and real estate sectors traditionally offer more defensive cash flows, less exposed to changes in economic growth. This has also made them more sensitive to rising bond yields. We expect them to relatively underperform in a more cyclicals focused environment with earnings strong and yields rising. |

| Cyclicals | We expect cyclicals – consumer discretionary (autos, apparel, restaurants), industrials, energy, and materials, to lead market performance. They are most sensitive to the sharp economic recovery and higher bond yield outlook, with more sensitive businesses, depressed earnings, cheaper valuations, and have been out-of-favour for many years. |

| Financials | Financials will benefit from the GDP growth recovery, with higher loan demand and lower defaults. Similarly, they benefit from higher bond yields outlook, charging more for loans than they pay for deposits. Sector has cheapest P/E valuation of any, and regulators recently giving flexibility to pay large 8-10% dividend and buyback yields. |

| Themes | We favour small cap vs large, on more GDP growth exposure, earnings upside, and domestic focus. Similarly, value over growth on GDP recovery, lower valuations, under-ownership after decade under-performance. Dividends and buybacks recovering with cash flows. Power of dividends under-estimated, at up to 1/2 of total long term return. |

| Traffic lights* | Other Assets |

| Currencies | We see recent USD strength easing as the rest-of-world GDP growth recovery accelerates, and fears over a virus ‘third wave’ ease. A stable or weaker USD traditionally supports Emerging Markets, commodities, and large US foreign earners, such as the tech sector, and could be a modest headwind to large exporters, such as Europe. |

| Fixed Income | US 10-year bond yields to rise modestly as inflation above 2% average Fed target, ‘real’ inflation-adjusted yields negative, Fed to gradually tighten policy. Will be modest as inflation expectations already high, wide spread to other market bond yields, and structural headwinds of all-time high debt, poor demographics, and low productivity. |

| Commodities | Supported by GDP growth rebound, ‘green’ industry demand, years of supply under-investment. China GDP and property sector are short term concerns. Industrial metals and battery materials seem best positioned, whilst oil price supported by only slow return of OPEC+ supply. Gold hurt by outlook for higher bond yields. |

| Crypto | Institutionalization of bitcoin market barely begun, as asset class benefits from very strong risk-adjusted returns and low correlations with other assets. Altcoins have outperformed as see broader interest and use cases. Clear supply rules a benefit as inflation rises. Volatility remains very high, with the 15th -50% pullback of the last decade. |

| *Methodology: | Our guide to where we see better risk-adjusted outlook. Not investment advice. |

| Positive | Overall positive view, and expected to outperform the asset class on a 12-month view. |

| Neutral | Overall neutral view, with elements of strength and weakness on a 12-month view |

| Cautious | Overall cautious view, and expected to underperform the asset class on a 12-month view |

Source: eToro

Analyst Team

| Global Analyst Team | |

| CIO | Gil Shapira |

| Global Markets Strategist | Ben Laidler |

| United Kingdom | Adam Vettese Mark Crouch Simon Peters |

| France | Antoine Fraysse Soulier David Derhy |

| Iberia/LatAm | Javier Molina |

| Poland | Pawel Majtkowski |

| Romania | Bogdan Maioreanu |

| Asia | Nemo Qin Marco Ma |

| Australia | Josh Gilbert |

COMPLIANCE DISCLAIMER

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.