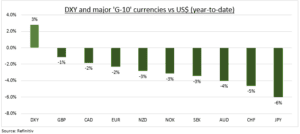

RALLY: The dollar (DXY) is near its highest since Nov. and the best performing G-10 currency this year. As markets react to more US growth strength and stickier inflation. Pushing up bond yields and widening differentials. Delaying start, and softening magnitude, of forecast US interest rate cuts this year. This US exceptionalism is now better priced, much of dollar outperformance behind us, and impacts from commodities to emerging markets have been limited. But conditions are diverging and to drive more currency dispersion. Sterling (GBP) has much in common with the dollar and has kept pace. Whilst Yen (JPY) round-tripped and has been the big laggard. New Zealand (NZD) is ready for more hikes, but Switzerland (CHF) and ECB (EUR) are early cutters.

GBP: Sterling (GBP) has been the ‘dollar of Europe’, and is similarly c.7% overvalued. The UK’s super sized consumer has cushioned its technical recession. Whilst inflation is still double target, giving the BoE plenty of ammunition to push against market hopes of early rate cuts. GBP outperformance is in stark contrast to the underperformance and bearishness on other UK assets. And has sapped the overseas sales focused FTSE 100 large caps. March 6th ‘spring budget’ the next catalyst and may be GBP positive if see well-calibrated tax cuts. Whilst October election risks are likely discounted with Labour 20 points ahead in polls and moved to centre.

JPY: Yen underperformance has resumed as US growth exceptionalism has twinned with the BoJ’s go-slow on policy normalisation. The USD/JPY has broken below the psychological 150 again, triggering verbal intervention from the authorities. But anything more forceful is unlikely. Given the fundamental drivers and with no rate hike likely until mid-year from current -0.1% level. The Yen is the world’s cheapest major currency and is approximately 25% undervalued on a real effective exchange rate basis. Weakness has given a new lease of strength to the Nikkei255, that is now closing in on its 1989 all-time-high. And fuelled near 10% export growth.

All data, figures & charts are valid as of 20/02/2024.