SPINOFFS: Announced breakups by GE (GE), Johnson & Johnson (JNJ) and Japan’s Toshiba highlight for many the ‘death of the conglomerate’. We are not so sure. Spin-offs have not performed well (see chart). Berkshire Hathaway (BRK) is still largest non-tech US stock. ‘Big-tech’ is looking more-and-more like conglomerates. Whilst private equity may also be ‘new conglomerates’, and with $3 trillion to invest. Different, yes. dead, no.

IN VOGUE: Latest announcements follow other big spin offs this year from the likes of Vivendi (VIV.PA), of world’s largest record label Universal (UMG), and cloud computing VMware (VMW) by Dell (DELL). The benefits of synergies, size, and diversification have become increasingly questioned. Investors are more willing to pay for growth and focus, whilst capital has also been both cheap and plentiful in a zero-interest rate world.

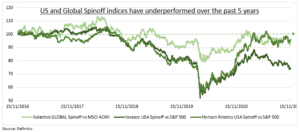

PERFORMANCE: Yet spinoff indices have underperformed (see chart), calling into question the conventional wisdom. This is blamed on everything from passive investing (leaving smaller spin offs as orphans) to activists (the spinning off of weak businesses).

‘NEW’ CONGLOMERATES: We are also seeing ‘new ‘conglomerates’ emerge. Many ‘big tech’ stocks own a wide range of businesses, and increasingly have conglomerate structures. See Alphabet (GOOGL) and most recently Meta Platforms (FB) decision. GE ex-CEO Jeffrey Immelt was also the first to call private equity the ‘conglomerates of this era’, given their huge growth and owning a wide swathe of companies in diverse sectors.

All data, figures & charts are valid as of 17/11/2021