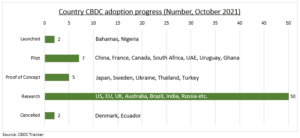

GROWTH: Digital currency (CBDC) momentum is accelerating (chart). CBDC Tracker shows launches by Bahamas (Sand dollar) and Nigeria (e-Naira). Bank for International Settlement (BIS) estimates 1/3 central banks researching them, double last year. China set pace, retail testing its e-CNY. ECB focused on technical issues. Fed has delayed its paper, given diverging opinions and with the most to lose with USD 60% of global FX reserves.

WHY?: Driven by 1) first-mover competition from $150bn market cap. stablecoins, and worries could loosen grip on monetary policy. 2) A retail CBDC could help implement monetary policy in a zero-interest rate world. 3) A response to lower cash use, down to 20% global transactions. 4) To boost financial inclusion, with c25% global population unbanked. CBDC’s could speed wholesale payments and cut cross-border fees. But also threaten traditional banks (XLF) if seen as more attractive alternatives, and help new entrants. There can also be privacy, security, cost concerns, depending on the CBDC type.

IMPACT: Central Bank ‘digital cash’, whether retail or wholesale, and the tech used, has many possible impacts. Ethereum (ETH) is the most supportive blockchain to develop CBDCs. Stablecoins like Tether (USDT) have seen calls for more regulation, but very centralised CBDC’s could stoke demand. CBDC’s may cut Visa (V), Mastercard (MA) acceptance costs, and boost Square (SQ), PayPal (PYPL) digital wallet funding sources. An early China (RMB) or EU (EUR) launch could boost their cross-border use vs USD.

All data, figures & charts are valid as of 06/12/2021