Global equity markets have had a good run since the stock market crashed earlier in the year, however, not all sectors have participated in the rally. While technology and healthcare stocks have surged in recent months, other sectors have been left behind.

Banking is one sector that has underperformed the broader market in 2020. Year-to-date, plenty of bank stocks are down 30% or more. Some bank shares have fallen so far they are now trading at levels last seen during the global financial crisis.

For long-term investors, the current share price weakness across the global banking sector could represent a buying opportunity. Here’s a look at why bank stocks have underperformed in 2020 and why they could potentially bounce back.

eToro’s TheBigBanks offers investors an opportunity to invest in the world’s top 25 banking institutions according to size of AUM and market capitalisation.

Check Out TheBigBanks Portfolio

Why Have Bank Stocks Dropped?

There are a few reasons bank stocks have underperformed in 2020.

The first is that bank profitability is linked to macroeconomic conditions. When economic conditions are strong, lending activity increases and bank profits rise. In contrast, when economic conditions are weak, lending activity decreases and banks see an increase in loan defaults. This reduces profits.

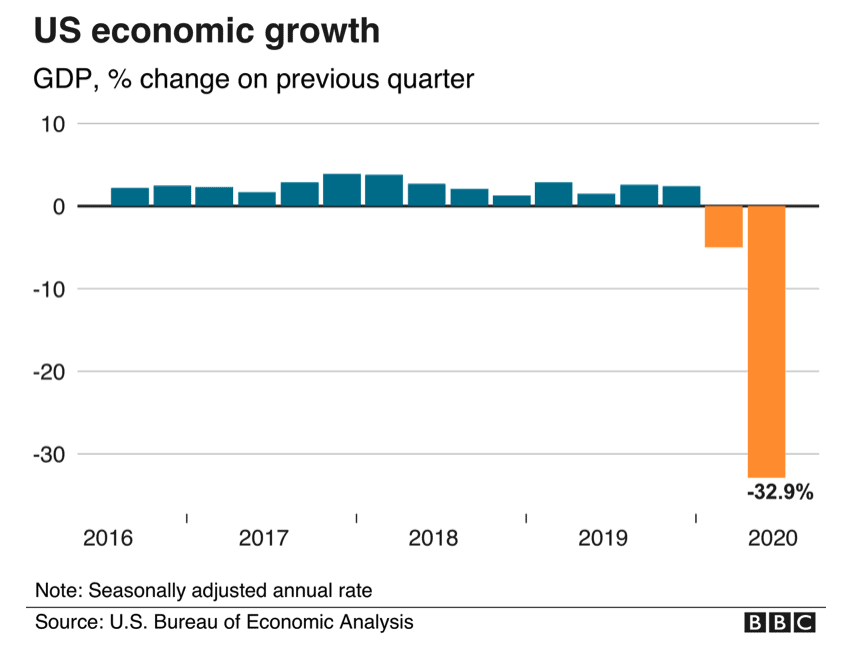

It is no secret that this year, economic conditions have been terrible. As a result of the coronavirus pandemic, the US economy shrank at an annual rate of 33% between April and June. This was the steepest decline since the government began keeping records in 1947¹.

Source: BBC

It was a similar story in Europe and the UK. The Eurozone suffered its largest contraction on record in the second quarter of 2020, with its GDP falling 11.9%². Meanwhile, the UK suffered a 20.4%³ contraction as the sovereign country grappled with lockdowns and spending cutbacks.

These economic conditions have taken their toll on banks’ profitability. Businesses have struggled to repay their loans and as a result, banks have faced a sharp increase in credit impairments.

Bank of America, for example, set aside $9.9 billion to cover credit losses in the first half of 2020. That compares to $1.9 billion for the same period last year. Meanwhile, Lloyds Bank — the UK’s largest lender — registered £3.8 billion in impairment charges in the first half of 2020.

Another reason bank shares have underperformed this year is that interest rates have fallen. Low interest rates are not good for banks. This is because they earn a large amount of their income from the spread between the interest rates they charge to lend money and the interest rates they offer to borrow money. This spread is called the net interest margin (NIM). If interest rates are high, banks have the opportunity to earn a larger NIM. If rates are low, there is less opportunity to profit.

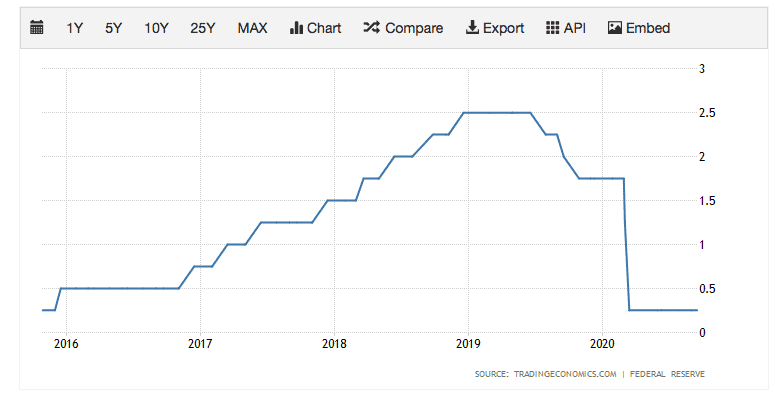

In the US, the Federal Reserve cut interest rates to near zero in March in an effort to bolster the economy. The central bank has kept rates unchanged since then. Rates could remain very low for years to come.

US Interest Rates

Source: Trading Economics

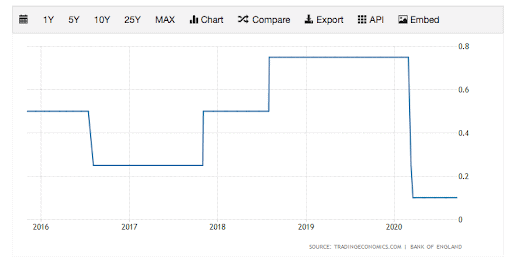

It is a similar story in the UK. Earlier in the year, the Bank of England slashed interest rates to 0.10%.

UK Interest Rates

Source: Trading Economics

These rock-bottom interest rates have crimped banks’ net interest margins and hampered their ability to grow revenues.

Overall, this combination of weak economic conditions and low interest rates has hit bank profitability hard. Wells Fargo, for example, recently reported a 57% decrease in net income for the third quarter of 2020. Citigroup, meanwhile, reported a 35% decrease in net income for Q3.

It is also worth pointing out that in Europe and the UK, regulators have banned banks from paying dividends this year. The reason for this is that the regulators want to ensure that banks have the financial capacity to support their economies. These dividend bans have decreased the appeal of holding bank stocks, resulting in capital flowing out of the sector.

Why Bank Shares Could Rebound

When you consider the challenging environment banks face right now, it is not hard to see why bank stocks have underperformed in 2020.

The thing is, though, these challenging conditions are unlikely to last forever. A Covid-19 vaccine — which may not be far off now — could be a game changer. The International Monetary Fund (IMF) believes that strong international cooperation on vaccines could potentially add $9 trillion to global income by 2025⁴. This would almost certainly boost banks’ profitability.

“The availability of a vaccine, or therapies with proven success in treating Covid-19, will materially lift the global outlook” – IMF Managing Director Kristalina Georgieva

While interest rates could remain low for a while, it is unlikely that they will remain at the current ‘emergency’ levels forever. When economies begin to pick up, central banks are likely to lift interest rates. This would enable banks to earn a larger NIM.

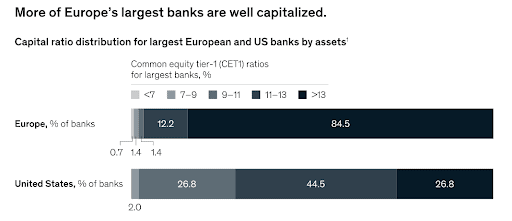

Importantly, the major banks have the financial strength to withstand short-term challenges. This is due to the fact that after the global financial crisis, regulators imposed strict new capital requirements on banks, which enhanced their resilience.

Entering the coronavirus crisis, major banks were in a strong position financially. Common Equity Tier 1 (CET1) ratios – a measure of bank solvency and capital strength — were 13% in Europe, 14% in the UK, and 12% in the US⁵, well above the minimum 4.5% level required under Basel III standards.

Bank CET1 Ratios Entering Covid-19

Source: McKinsey

It is worth pointing out that the financial market volatility that we have seen this year has actually been a boon to some of the banks. In the same way that eToro customers have upped their trading this year in order to capitalise on opportunities, institutional investors have been trading more. In the second quarter of the year, a number of major Wall Street banks, including JP Morgan Chase, Citigroup, and Bank of America, saw double-digit spikes in trading revenues as investors reacted to the pandemic. At JP Morgan, trading helped push the bank’s quarterly revenue to a record high. This boost in trading income could help offset losses in other areas.

Of course, overall, 2020 is likely to be a poor year for the banks in terms of profitability. Earnings across the sector are likely to be well down from last year. However, looking at future forecasts, analysts expect earnings to increase significantly in 2021. For example, analysts expect Wells Fargo’s earnings per share (EPS) to jump from $0.42 this year to $1.08 next year — an increase of 329%.

Bank EPS Forecasts

| Bank | FY2020 | FY2021 | EPS increase |

| JP Morgan Chase ($) | 7.45 | 8.69 | 17% |

| Bank of America ($) | 1.74 | 2.00 | 15% |

| Wells Fargo ($) | 0.42 | 1.80 | 329% |

| Citigroup ($) | 4.15 | 5.37 | 29% |

| HSBC ($) | 0.24 | 0.44 | 83% |

| Lloyds Bank (p) | 1.03 | 3.40 | 230% |

| Barclays (p) | 4.84 | 13.50 | 179% |

Source: NASDAQ and Thomson Reuters

Meanwhile, on the dividend front, the ban on dividends in Europe and the UK could be lifted as early as next year. This could increase the appeal of bank stocks among income investors, pushing their share prices higher.

What this all means is that there could be an opportunity for investors right now. In the same way that many bank stocks recovered after the global financial crisis, bank stocks could recover in the next few years as economic conditions improve and earnings pick up.

Those who bought bank shares in the aftermath of the global financial crisis were rewarded well. For example, between March 1st, 2009 and March 1st, 2012, JP Morgan Chase & Co’s share price jumped from $23 to $43 — an increase of 87%.

Could those buying bank shares now, while they are out of favour, see similar gains? It is certainly possible.

Check Out TheBigBanks Portfolio

Are Bank Stocks Undervalued?

Examining valuations across the sector, bank shares appear to be undervalued. Using next year’s EPS forecasts, valuations are very low. Citigroup, for example, currently trades on a forward-looking price to earnings (P/E) ratio of just 8.0. Barclays currently sports a P/E ratio of just 7.6. These valuations indicate that bank stocks are cheap right now.

Bank P/E Ratios

| Bank | P/E FY2020 | P/E FY2021 |

| JP Morgan Chase ($) | 13.6 | 11.6 |

| Bank of America ($) | 13.8 | 12.0 |

| Wells Fargo ($) | 54.8 | 12.8 |

| Citigroup ($) | 10.4 | 8.0 |

| HSBC ($) | 16.8 | 9.2 |

| Lloyds Bank (p) | 26.2 | 7.9 |

| Barclays (p) | 21.3 | 7.6 |

Source: NASDAQ and Thomson Reuters

Attractive Risk/Reward Proposition

Of course, there are risks to the investment case.

One risk is that a Covid-19 vaccine does not eventuate in the near-term and economic conditions get worse. Another is that interest rates remain low for a long period of time.

Other risks to consider include regulatory fines and competition from the FinTech sector.

Overall, however, bank stocks appear to offer an attractive risk/reward proposition.

For long-term investors, share price weakness across the banking sector could represent a buying opportunity.

Check Out TheBigBanks Portfolio

Sources:

- https://www.bbc.co.uk/news/business-53574953

- https://www.bbc.co.uk/news/business-53606101

- https://www.bbc.co.uk/news/business-53918568

- https://abcnews.go.com/Business/faster-development-covid-19-vaccine-raise-global-incomes/story?id=73653732

- https://www.mckinsey.com/industries/financial-services/our-insights/banking-system-resilience-in-the-time-of-covid-19#

This is a marketing communication and should not be taken as investment advice, personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking any particular recipient’s investment objectives or financial situation into account, and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication, which has been prepared utilising publicly available information.