British Prime Minister Boris Johnson was admitted to hospital for further tests last night, almost two weeks after testing positive for Covid-19. A spokesperson said that the tests are precautionary due to Johnson displaying “persistent symptoms.”

Johnson’s is one of 47,806 confirmed cases in the UK, although the true number is thought to be far greater.

UK infections are expected to peak in the next few weeks, with the number of daily cases hitting its highest level so far yesterday after another 5,903 people were confirmed to be infected.

Shares are rallying this morning as expectations of the peak boost confidence. The FTSE 100 is up 3.2% at 5,589 points, following a sharp rally in Asia — Japan’s Nikkei closed up 4.2% and Hong Kong’s Hong Seng rose 2.3%.

As the US enters a key week in its progress through the coronavirus pandemic curve, investors are eyeing up a potential peak there as well, which would set the country back on a path to normality. Stock futures were higher on Sunday evening, after New York — the epicenter of Covid-19’s spread in the US — reported a drop in the number of new cases and deaths. President Trump then gave an address, saying that “in the days ahead America will endure the peak of this pandemic.” While the coming week is likely to be among the most devastating in terms of the human impact in the US, a fall in infection and mortality would start the conversation about a timeline for re-opening the economy. Normality is still a long way off but, given that the economic impact of the virus is largely dictated by its duration, any containment progress will be viewed positively.

Elsewhere, volatility shows no signs of abating in the oil market. Global oil cartel Opec and Russia postponed a meeting to negotiate supply cuts late last week, another negative in this unexpected and brutal war. The meeting is reportedly happening later in the week, but the setback is likely to cause the oil price to sink back after its 30% plus surge last week.

Deluge of economic data sinks US stocks for third week in four

A slew of negative economic numbers dragged the major US stock indices to their third negative week in the past four on Friday, with the Dow Jones Industrial Average finishing close to 3% lower. The March jobs report released on Friday showed that the US economy lost 700,000 jobs in March, but this is likely to be the tip of the iceberg as its accuracy depends on when in the month the data was collected. The figure was far worse than anticipated and followed dire initial weekly jobless claim numbers. Last week, 6.6 million people filed for unemployment benefits in the US, taking the two week total to 10 million.

As the hard data feeds through on the toll being taken on the labour market, investors have actually become less fearful. The Cboe Volatility Index, commonly referred to as the “fear index”, is sitting at below 50, well below its 80 plus peak last month.

In corporate news, Tesla reported that its Q1 vehicles delivered came in at just below expectations, with analysts noting that a rebound in China production and demand should be a driver of growth for the firm in the coming months, although the landscape the firm faces remains challenging; the major carmakers have all reported huge drop offs in sales. As companies ramp up their own efforts to combat the virus, with many transforming production lines to produce face masks and ventilators, Apple CEO Tim Cook said on Sunday that the smartphone giant has donated more than 20 million face masks worldwide and is manufacturing one million face shields a week.

S&P 500: -1.5% Friday, -23% YTD (-2.1% last week)

Dow Jones Industrial Average: -1.7% Friday, -26.2% YTD (-2.7% last week)

Nasdaq Composite: -1.5% Friday, -17.8% YTD (-1.7% last week)

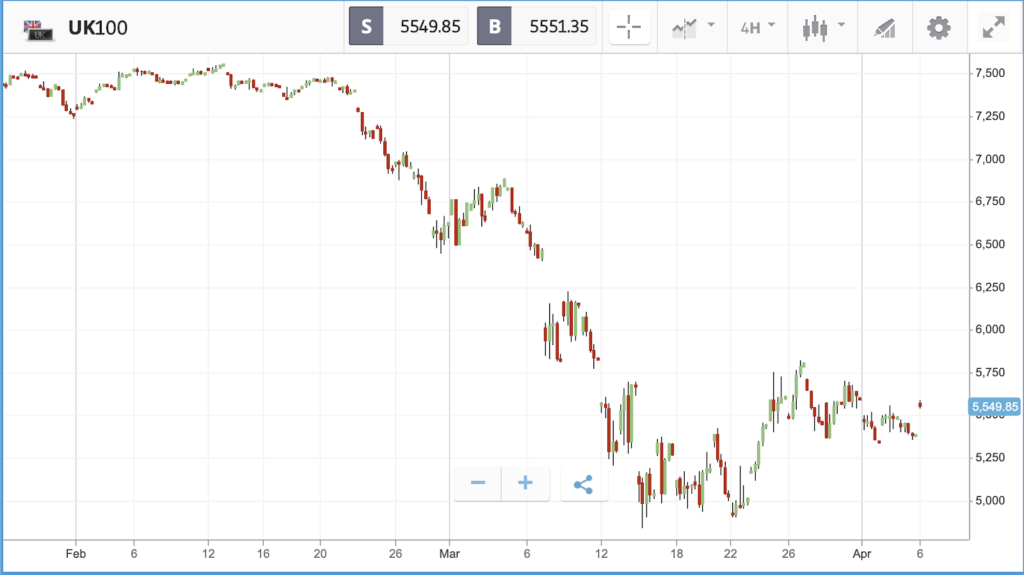

Rough week for small-cap UK stocks

Small and mid-sized London-listed stocks faced a far tougher week than their large cap counterparts last week, with the FTSE 250 index sinking 4.5% to the FTSE 100’s 1.2% drop. After UK banks were forced to scrap billions in dividend payments, we’ve seen a corresponding impact on company plans to reward shareholders across a variety of industries. On Sunday, it was reported that aero-engine maker Rolls-Royce is planning to ditch profit targets and suspend its dividend, as the near total shutdown of the airline industry leaves its mark. The firm was one of the biggest losers in the FTSE 100 on Friday, falling 9.6% and helping to take the index to a 1.2% daily loss. The FTSE 250 fell 2.3%. The other biggest losers in the FTSE 100 on Friday were Legal & General, Pearson and Whitbread, which fell 10.1%, 9% and 8.8% respectively.

As UK infections surge, new Bank of England governor Andrew Bailey wrote in a newspaper column that the central bank will “not hesitate to take all necessary actions to support British businesses and households through this period of uncertainty and to ensure inflation is consistent with the two per cent target in the medium term”.

FTSE 100: -1.2% Friday, -28.2% YTD (-1.7% last week)

FTSE 250: -2.3% Friday, -35.6% YTD (-4.5% last week)

What to watch

Oil stocks: Oil and energy stocks look to be in for another rough week. After the oil price gained more than 30% on the final two days of last week, names including Chevron and BP rallied, with those two stocks gaining 9.2% and 10.4% respectively. That rally was driven by hopes of Russia and Opec sitting down and hammering out a supply cut deal to bring an end to the oil price war. The delay of the meeting, scheduled for today, throws a spanner into the works; continued uncertainty will stoke investor fears that a supply cut is not forthcoming. Expect the situation to develop as the week progresses, with volatility in store for oil and energy names.

UK construction PMI: Monday is a quiet day both in corporate earnings announcements and economic data, but one datapoint that is being released is the purchasing managers index for the UK construction in March. The survey offers a window into the health of the UK construction sector, with a reading above 50 indicating expansion and a value below indicating contraction of the sector. Last month, the reading came in at 52.6, with the expectation being for it to sink well below 50 today. The sector stands to be impacted both by the pandemic-related lockdown in the UK preventing projects from progressing, and the knock-on effects of companies going bankrupt and reigning in spending as they attempt to navigate the pandemic — which may impact demand for commercial development.

What will it take for US markets to stabilise?

Goldman Sachs analysts have set out three key criteria that must be met in the United States before investors can be confident that markets have found the bottom. Firstly, the viral spread in the US must begin to slow so that the full economic impact can begin to be unpicked — something currently impossible to do without an end date in sight. Secondly, there has to be evidence that the fiscal and monetary measures taken by the Federal Reserve and lawmakers to shore up the economy are sufficient in terms of limiting bankruptcies and layoffs. Finally, investor sentiment and positioning have to bottom out, with Goldman noting that its US equity sentiment indicator is still some way off the negative levels seen in other recent market corrections.

Crypto corner:

Bitcoin and the other cryptoassets continue to regain lost ground, with Bitcoin up 3.3% at $6,988, and Ethereum jumping 4.5% to $148.

XRP, the third largest asset, is also up 3.6% at $0.18, with the space increasingly attracting investor attention following the heavy sell-off it endured earlier in the month.

On Friday a barrage of lawsuits were filed against some of the most prominent crypto exchanges including Binance and Bitmex. The lawsuits allege a number of securities violations and will undoubtedly be contested, however, there are complexities in that many of the defendants are not based in the US where the case has been filed.

eToro (UK) Ltd is authorized and regulated by the Financial Conduct Authority. eToro (Europe) Ltd is authorized and regulated by the Cyprus Securities and Exchange Commission. eToro AUS Capital Limited is regulated by the Australian Securities and Investments Commission, ABN 66 612 791 803, AFSL 491139.

This is a marketing communication and should not be taken as investment advice, personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without having regard to any particular investment objectives or financial situation, and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication, which has been prepared utilizing publicly-available information.

eToro is a multi-asset platform which offers both investing in stocks and cryptoassets, as well as trading CFDs.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 62% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work, and whether you can afford to take the high risk of losing your money.

Cryptoassets are volatile instruments which can fluctuate widely in a very short timeframe and therefore are not appropriate for all investors. Other than via CFDs, trading cryptoassets is unregulated and therefore is not supervised by any EU regulatory framework. Your capital is at risk.