Good morning everyone,

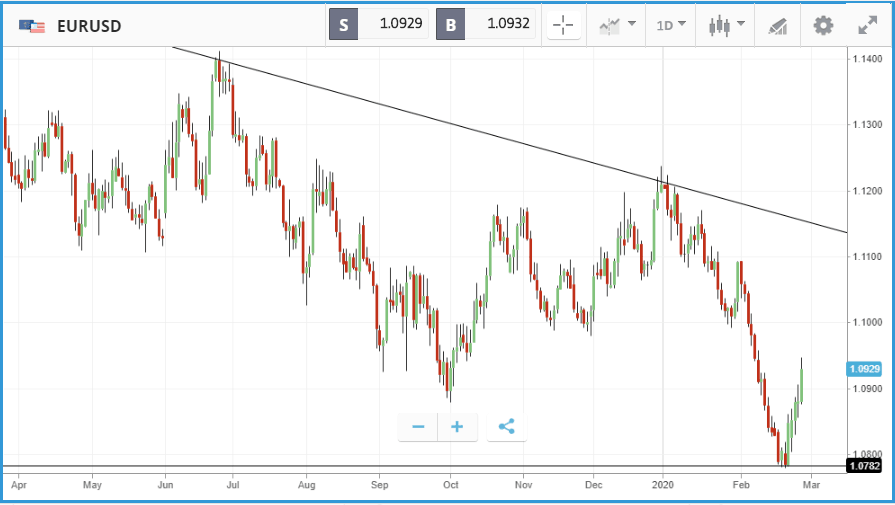

Markets are in the red again this morning but interestingly it is China which is holding up the best with the CSI 300 index in the black. However, other Asian bourses including both the Hong Kong-based Hang Seng index and the Japanese Nikkei 225 were negative yesterday. The number of new cases of coronavirus was greater outside of China for the first time yesterday, with northern Italy being particularly badly affected but also South Korea and potentially California emerging as hotspots for the virus. Oil continued its decline and the dollar also pulled back as markets called for action from the Federal Reserve to help alleviate the economic damage from the virus. The euro has gained over 1.3% on the greenback since sinking to 3 year lows earlier this month.

Major stock indices in both the US and UK pared their early losses and levelled off somewhat yesterday after two days of 3% plus falls. That said most still ended the day in the red. The Dow Jones Industrial Average ended the day 0.5% lower, with 22 of its 30 constituent stocks falling, while the S&P 500 ended the day down 0.4%. Amongst the choppy trading, some of the travel names that were hardest hit earlier in the week continued to sink like a stone. We have mentioned easyJet a couple of times already this week and it is down another 8% this morning. The spread of the coronavirus epidemic outside of China is stoking fears of more widespread travel restrictions which would hit the bottom line of firms ranging from airlines to booking services. Royal Caribbean Cruises, Norwegian Cruise Line, Carnival and Expedia fell the furthest among S&P 500 stocks, each losing more than 7%. The Nasdaq Composite was a bright spot yesterday, climbing 0.2%, with a 5.3% pop for Netflix helping drive the index higher.

Changing of the Bobs at Disney, while Microsoft warns virus will hit revenue

Yesterday, Microsoft stock sank 2% in after-hours trading, following the announcement that it expects to miss its quarterly revenue guidance for its Windows and Surface units, due to supply chain issues caused by the coronavirus epidemic. While investors were focused on virus headlines, it was a day of change at the top of some of America’s leading companies. Late on Tuesday The Walt Disney Company surprised investors by announcing that CEO Bob Iger was leaving the top seat, with head of parks and resorts Bob Chapek taking over the role immediately. The firm’s share price has lagged the broader market over the past five years, and has had a poor start to 2020. At the same time as Disney’s news, Salesforce announced that co-CEO Keith Block is stepping down after less than two years in the role. Lastly, the world’s largest asset manager BlackRock, announced that co-founder and public policy lead Barbara Novick is stepping down. In a note yesterday, BlackRock CEO Larry Fink said that “much of the post-financial crisis policy work that Barbara led is largely implemented”, referring to her role in helping the fund giant avoid the kinds of regulation faced by the major banks.

S&P 500: -0.4% Wednesday, -3.5% YTD

Dow Jones Industrial Average: -0.5% Wednesday, -5.5% YTD

Nasdaq Composite: +0.2% Wednesday, +0.1% YTD

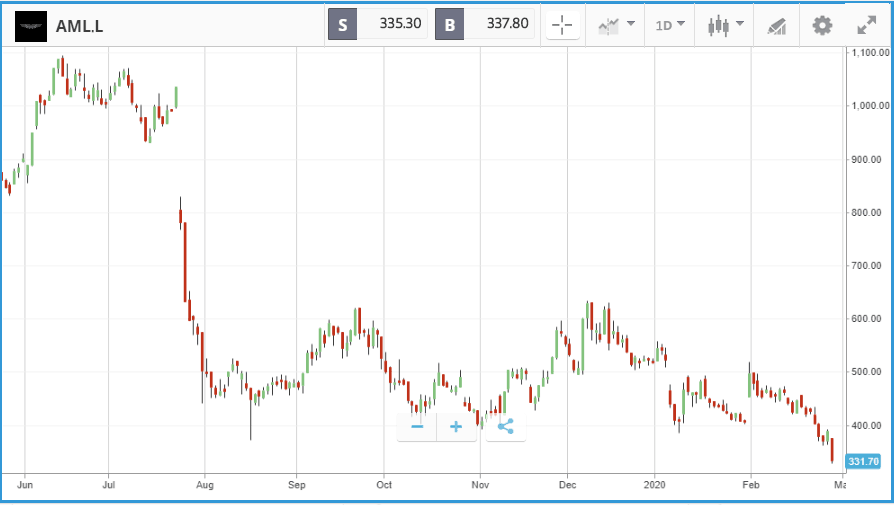

Aston Martin CFO steps down amid concerning update

The past 18 months has been nothing short of a car crash for Aston Martin. However, while the luxury car maker warned on profits in January, its full-year results may well shock a lot of investors. A £100 million loss, an alarming slump in sales, a sharp increase in net debt and a fresh rights issue to repair its balance sheet are not the sort of things they wanted to see in Aston’s results approaching 18 months on from its much-hyped IPO. The much-loved James Bond automaker has promised to ‘reset’ this year, with the need to cut costs and normalise their stock levels. Performance in China was perhaps the highlight in the update, up 28% although a continuation of this is clearly now a concern in light of coronavirus.

Yesterday was a mixed day for UK stocks, but the FTSE 100 closed 0.4% higher. The index was led by NMC Health, Evraz and Smurfit Kappa Group, which closed 6.6%, 4.7% and 3.6% up respectively. HSBC also helped take the index higher, gaining 2%. The banking giant’s share price is roughly flat since announcing 35,000 job cuts early last week. The bank currently offers a dividend of around 7% after losing a third of its value over the past two years. Smaller London-listed stocks faced a more difficult day, with the FTSE 250 sinking 0.5% and the FTSE AIM All-Share index dropping 0.2%. Wagamama owner Restaurant Group was the biggest loser in the FTSE 250, closing 7.2% down after suspending its dividend and announcing plans to cut the number of restaurants. The casual dining group has now lost more than 35% in 2020 so far, and 80% over the past five years. In crossover US-UK news, it was reported yesterday that Walmart is in talks to sell a majority stake in Asda, a year after UK regulators shut down an attempt to merge the supermarket chain with Sainsbury’s.

FTSE 100: +0.4% Wednesday, -6.6% YTD

FTSE 250: -0.5% Wednesday, -5.8% YTD

Stocks to watch

Keurig Dr Pepper: Keurig Green Mountain bought Dr Pepper Snapple Group in an $18.7bn deal two years ago, creating a firm that controls brands including Krispy Kreme, Schweppes and Evian. Over the past 12 months, Keurig Dr Pepper stock has climbed 6.6%, well behind the broader market, but it has held up well in the face of the coronavirus-linked sell off. The firm reports earnings this morning, when analysts will likely be focusing on new segments the company has been entering into. Currently, Wall Street analysts have an average 12-month price target on the stock of $31.50, versus its $28.73 at Wednesday’s close, with a range between $26 and $35.

Baidu: Nasdaq-listed Chinese internet search giant Baidu reports its latest quarterly earnings on this evening New York-time, after a difficult period which has seen the firm lose more than 50% of its value since summer 2018. The past six months have been more positive however, with the stock up around 20%. It has held up well against the coronavirus epidemic as its business is not as subject to logistical disruption given its internet focus. Analysts overwhelmingly favour a buy rating on the stock, with 28 rating it as a buy or overweight, and eight as a hold.

International Consolidated Airlines Group: IAG has been hit hard by this week’s sell-off, with double digit losses, after a huge six months that saw its share price gain more than 50%. The potential impact of the virus will be a major focus for analysts on the company’s earnings call on Friday. Coronavirus cases in Italy have now surged past 400, threatening the potential of travel disruption in Europe. Analysts at Berenberg have warned that lower demand for travel and tourism is already beginning to harm service sector activity. easyJet’s share price has sunk more than 20% this week.

Crypto corner

The sell off in the world’s three major cryptoassets worsened yesterday. Over $190m in bitcoin was liquidated on derivatives exchange BitMEX – a further challenge to the already shaky concept of crypto as a safe haven.

Bitcoin started yesterday around $9,320 but suffered heavy losses, down to $8,490 in early trading today, before recovering to around $8,758. Ethereum similarly started Wednesday at $245 before bottoming at $208 in early trading. It has now recovered to around $223. XRP started yesterday at $0.25 before dropping to $0.22. It has since recovered more slowly to around $0.23.

We have previously mentioned the bitcoin ETF application from Wilshire Phoenix. The SEC announced yesterday that it had been rejected. They stated that Wilshire had not proven that the market was sufficiently resistant to market manipulation. This is another one to add to the pile of rejections with the volatility mechanisms Wilshire put in place not enough to change the SEC’s mind that the product was different enough to those before it.

eToro (UK) Ltd is authorized and regulated by the Financial Conduct Authority. eToro (Europe) Ltd is authorized and regulated by the Cyprus Securities and Exchange Commission. eToro AUS Capital Limited is regulated by the Australian Securities and Investments Commission, ABN 66 612 791 803, AFSL 491139.

This is a marketing communication and should not be taken as investment advice, personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without having regard to any particular investment objectives or financial situation, and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication, which has been prepared utilizing publicly-available information.

eToro is a multi-asset platform which offers both investing in stocks and cryptoassets, as well as trading CFDs.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 62% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work, and whether you can afford to take the high risk of losing your money.

Cryptoassets are volatile instruments which can fluctuate widely in a very short timeframe and therefore are not appropriate for all investors. Other than via CFDs, trading cryptoassets is unregulated and therefore is not supervised by any EU regulatory framework. Your capital is at risk.