Stocks in the UK jumped this morning after a deluge of news across the globe – both positive and negative – broke overnight. A report from pharmaceutical firm Gilead Sciences said that a Chicago hospital using an antiviral medicine to treat Covid-19 patients has seen rapid recoveries as a result, with most patients discharged in less than a week. Gilead stock jumped more than 15% in after-hours trading following the news.

China also reported its first quarter GDP figures after the US markets had closed yesterday, with a 6.8% contraction versus the same period a year ago. The result marked the first quarterly contraction since official records began in 1992 and was worse than expected.

In the US, the initial weekly jobless claims number came in at 5.2 million, bringing the total over the past four weeks to 22 million as the US economic shutdown continues to ravage the labour market. Having claimed “total authority” to decide when US states will reopen their economies, President Trump backed down from his claims on Thursday, reportedly telling state governors that “you are going to call your own shots” as he introduced new guidelines for states to begin emerging out of lockdown.

Nonetheless, markets are resolute. The UK is up 2.6% just after open, at 5,775 points, while overnight Asian markets surged. The Japanese Nikkei closed up 3.2% while Hong Kong’s Hang Seng was 1.7% higher.

Boeing soars after announcing it will restart plane production

All three major US stock indices were up on Thursday, despite dire manufacturing data. The Federal Reserve Bank of Philadelphia’s manufacturing index for April came in at -56.6, versus -12.7 for the previous month, the lowest reading since 1980. The Nasdaq Composite continued to build out its lead over the S&P 500 and Dow Jones Industrial Average, gaining 1.7% and pushed higher by 4% plus share price pops from names including Nvidia, Amazon and Kraft Heinz.

After-hours, Boeing stock soared by as much as 10% after the firm said that it will begin phasing back in airplane production at its Washington state factories, with tens of thousands of employees set to go back to work as a result. The Dow Jones Industrial Average was close to flat, with insurer UnitedHealth the biggest winner after announcing its Q1 2020 results. UnitedHealth beat profit expectations for the quarter, as the additional costs it incurred due to the coronavirus pandemic were cancelled out by members of its insurance plans cancelling elective surgeries and routine appointments which the firm would normally have to pay out claims for.

S&P 500: +0.6% Thursday, -13.4% YTD

Dow Jones Industrial Average: +0.1% Thursday, -17.5% YTD

Nasdaq Composite: +1.7% Thursday, -4.9% YTD

FTSE 100 posts modest gain, Barratt cuts executive pay

In the UK yesterday, the FTSE 100 and FTSE 250 both posted a modest gain, with each still down more than 25% year-to-date. The FTSE 100 was taken higher by names including pharmaceutical giant GlaxoSmithKline and homebuilder Barratt Developments, which both rose more than 5%. Barratt made gains after announcing that, while it expects home sales to be “very limited” during this period of disruption, the firm’s leadership team and managing directors have all agreed to a 20% reduction in salary while the crisis is ongoing.

In corporate news, the row between budget carrier easyJet and its founder Sir Stelios Haji-Ionnaou intensified, with the airline describing Haji-Ionnaou’s attempts to unseat him as “disturbing” according to The Telegraph. The airline also announced that it is planning to keep the middle seats on its planes empty when they return to the skies in order to help reduce the spread of Covid-19. easyJet stock fell 2.5% on Thursday.

Foreign secretary Dominic Raab said at a press conference yesterday that it would not be “business as usual” with China once the pandemic ends, and that there needs to be “a very, very deep dive after the event and review of the lessons, including of the outbreak of the virus.”

FTSE 100: +0.6% Thursday, -25.4% YTD

FTSE 250: +0.2% Thursday, -29.7% YTD

What to watch

Procter & Gamble: Consumer goods giant Procter & Gamble was meant to report earnings next week, but put out a press release on Tuesday announcing that the firm is moving up its announcement to Friday to provide shareholders information “as quickly and transparently as possible, and should not be construed as an indication of either positive or negative results.” The firm’s brands include Oral-B and Head & Shoulders, and the company has likely been a beneficiary of consumers stocking up. However, it will have had to deal with supply chain issues and physical retailers shutting down or restricting access. Wall Street analyst expectations for the firm’s earnings per share figure have actually increased from $1.11 three months ago to $1.12 now, with analyst ratings shifting to become more positive. Currently, 12 analysts rate the stock as a buy, one as an overweight and eight as a hold.

Schlumberger: Oil field services firm Schlumberger employs over 100,000 people worldwide and has seen its share price decimated by the oil price war and collapse in demand. The company’s stock is down 65.1% year-to-date, including 14.7% over the past five trading days. Schlumberger’s Friday earnings call will provide one of the first major windows into how the decimation of the sector is impacting company bottom lines, future plans and considerations around cost cutting. The stock has lost five buy ratings from analysts over the past three months, and earnings per share expectations for Q1 have dropped by 20%.

State Street: Following earnings releases by rivals BNY Mellon and BlackRock on Thursday, State Street — one of the main plumbers of the global asset management industry — reports its own Q1 earnings on Friday. As with many of its peers, lower interest rates will likely weigh on State Street’s earnings as this leaves less margin for it to make money on cash balances. Analysts will be watching closely for the degree to which increased revenue from higher trading and foreign exchange volumes counteract lower asset-based fees due to the stock market sell-off.

Crypto corner:

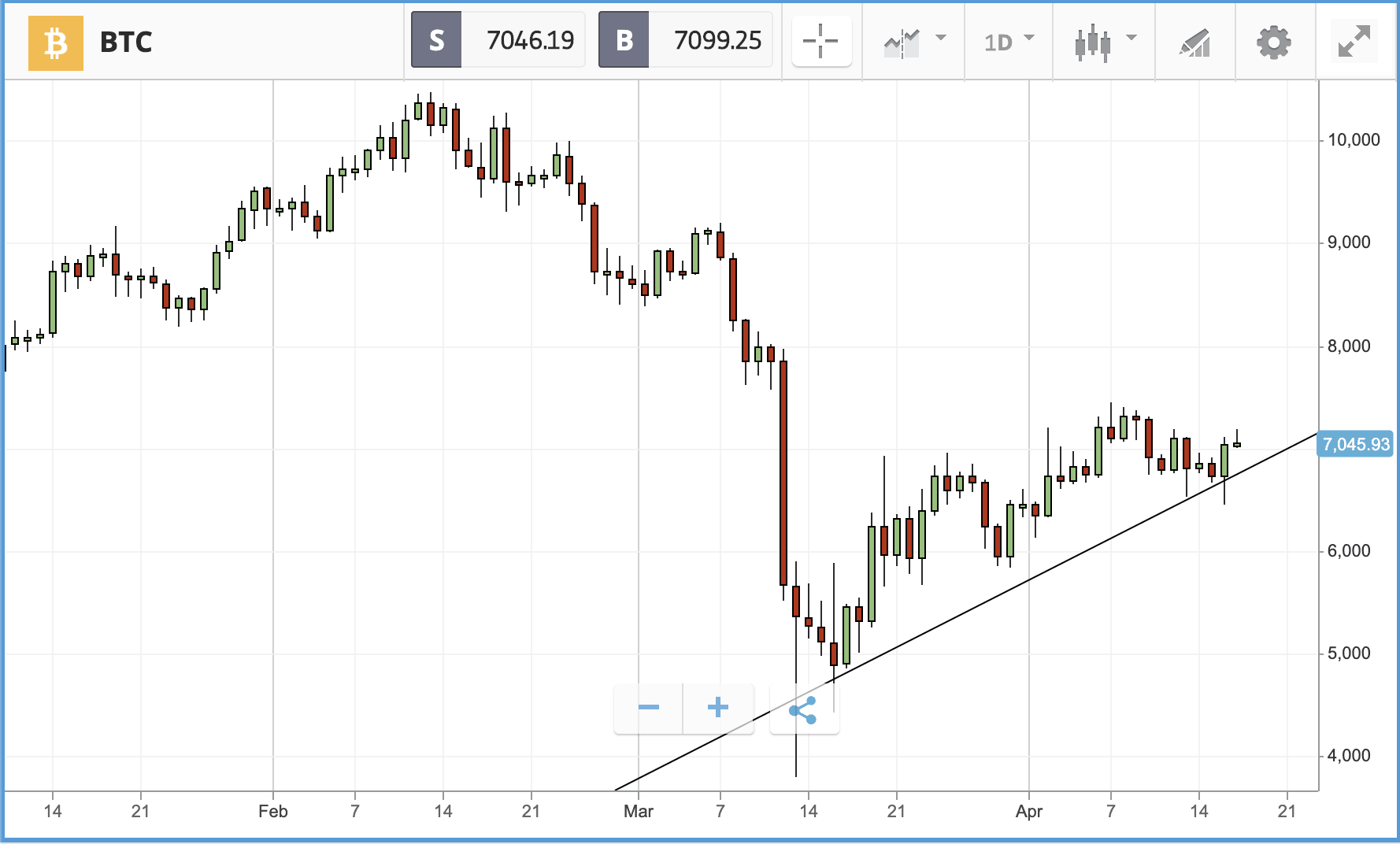

Bitcoin was off marginally in early trading, down 1.2% but above the $7,000 mark, near to its one-month peak of $7,303. The rally seems to be holding since its collapse in March, up more than 40%.

Its peers have enjoyed similar rallies; Ethereum is back near the $170 mark, having dropped as low as $108 in March, although it is off 3% today in morning trading, whilst XRP has also rebounded from a low of $0.136 to its current price of $0.185.

All data, figures & charts are valid as of 17/04/2020. All trading carries risk. Only risk capital you can afford to lose.