No Rate Cut in the Land of Aussie?

The week, which will end with the usual bang that comes with the US Non-farms release, is expected to have a vibrant opening with the big players in the FX arena eyeing the RBA rate decision which is due out on Tuesday. The Aussie dollar has been bruised lately, certainly against its American peer, the US Dollar, but also its weaker peers back in the Asia Pacific Rim.

The reason for that bruising? Bets have begun to mount that, amid weakness in commodity prices and softness in China, the RBA will move to cut interest rates. For investors, the inflation reading was but the latest cue for a rate cut this week. Speculation was that inflation would plunge further away from the RBA’s 2-3% range, which would pave the way for a rate cut. But as you all know, the world of FX is full of twists and turns, and as it turned out, while official inflation plunged to 1.7% YoY, the RBA trimmed Mean CPI, which is the RBA’s own measurement that pointed on inflation at 2.2%, thus dashing hopes for a rate cut among Aussie bears and allowing a sigh of relief to escape among Aussie bulls. As the time for the RBA rate decision approaches, volatility on the Aussie is expected to climb. If the RBA does confirm that rate cuts are not on the plate, Aussie bulls could take the front run and stir the Aussie higher, especially vs its Pacific peers.

BoE to Back Away?

For a while now we have been speculating that the Bank of England would make a U-turn in its policy and water down talks on a rate hike. The reason? The UK economy is losing momentum and inflation is plunging. It was only last week that the UK reported GDP growth rate of 0.5% with uneven momentum, i.e. an acceleration in the UK services sector but a sharp slowdown in UK construction and industrial output. This means the UK is growing unevenly and inflation is falling, yet the BoE rate hike talk continues to loom. If, indeed, at the next BoE meeting, the central bank’s Monetary Policy Committee signals a reversal – the long awaited U-turn – the Pound Sterling could begin to take a plunge but the FTSE100, which is weighted by relatively high rates, would be set to surge higher. If the BoE continues to hint at rate hikes, the exact opposite might occur, however.

Will Non-farms Surprise?

As the week progresses, focus will move on to the main event across the Atlantic, namely, the monthly release of US Nonfarm payrolls. Although last month’s reading of 253K was below expectations and came alongside disappointing data on falling wages, overall it was a fair reading. However, Dollar bulls have gotten used to more than “fair;” they have become accustomed to robust figures and this is what they expect from this month’s release. This month FX investors will be looking for a reading around 280K, or even closer to the 300K mark, and for unemployment to hold at 5.6%. If figures once again undershoot expectations, Dollar buying could be trimmed and investors could move to neutral while Wall Street could face selling pressure.

Down to Business

Overall the focus of this week is pretty clear; investors will look for a neutral to dovish tone from the Australian and UK central banks, and more robust jobs figures from the US to enable the Dollar to move higher. If the NFP release does, indeed, confirm an optimistic scenario that will validate the fact that the Fed is getting nearer to raising rates in contrast to the rest of the developed world, then the Dollar will rise. If, on the other hand the figures disappoint, the Dollar could move to range bound vs its European peers and might lose ground vs the Aussie.

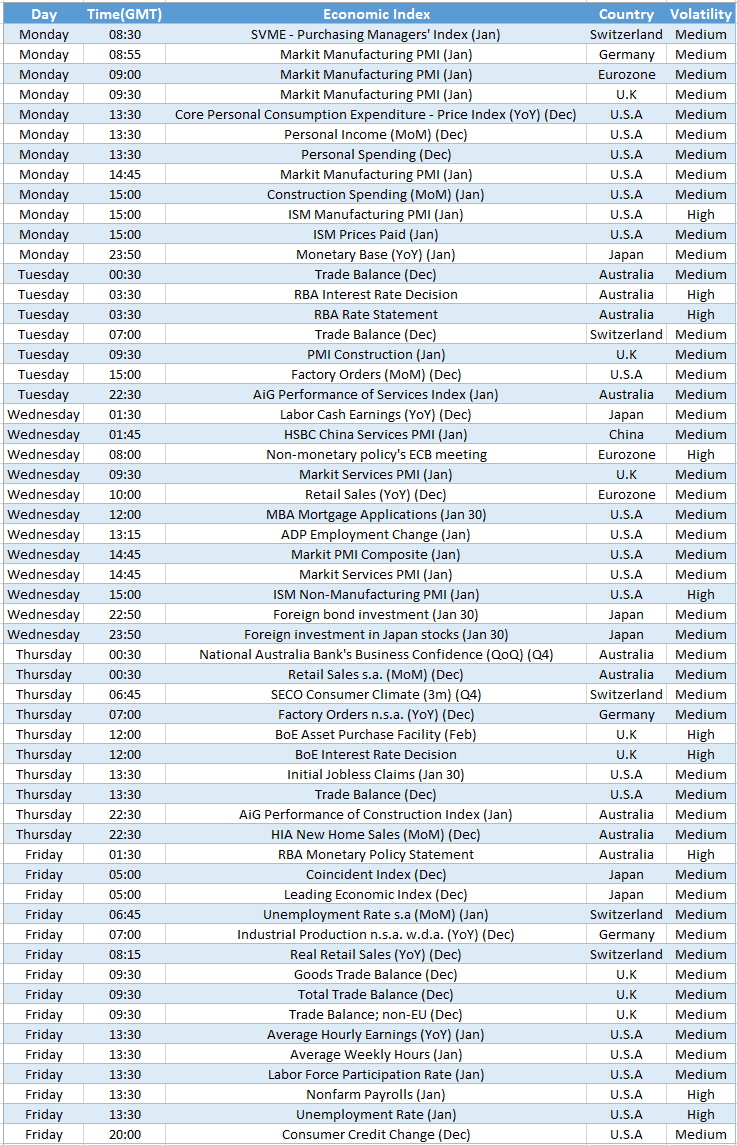

On the Plate

US Personal Spending (Monday) – Will shed some light on US consumption patterns and could indicate if US Inflation is moving higher or lower.

ISM Manufacturing PMI (Monday) – If US manufacturing PMI returns to rise it could support the dollar until Friday’s Nonfarm.

RBA Rate Decision(Tuesday) – If Indeed the RBA confirms speculations and maintains rates unchanged and pushes rate cuts from the agenda , it will favour the Aussie dollar.

ECB Non Rate Meeting(Wednesday) – Although this is not a rate meeting , there exists a slight chance that some suggestions and/or indication of future ECB policy could be declared which could strongly affect the Euro.

ISM Non-manufacturing PMI (Wednesday) – Will shed light on the US manufacturing sector.

BoE rate decision(Thursday) – If indeed the BoE will perform a U-turn from rate hikes it could hit Sterling and benefit the FTSE100.

RBA Policy statement(Thursday) – Anything that will not be released in the RBA official rate decision such in economic assessments and future policy is expected to be released in this statement and thus strongly affect the Aussie dollar.

US Nonfarm Payrolls(Friday) –The main event of the week. If US nonfarm payrolls will crawl closer to 300k and unemployment holds at 5.6% or lower, it would be positive for both the dollar and Wall Street.

Chart of the Week- FTSE100