Job Data to Pin Down Rate Hike?

In the week ahead, there are two key market-moving events that traders will want to zero in on. The first is Thursday’s release of the Bank of England’s rate decision and then on Friday, the Non-farms Payroll figures for July from the U.S. In terms of their importance to the global markets, however, Friday’s NFP outcome would assuredly eclipse the BoE decision. Why would that be the case? Simply because the NFP results and the associated labor reports could tip the scales for the Federal Reserve Bank. Along with price stability, the Fed is mandated to ensure full employment. Monetary policy, then, is supposed to be a reflection of the FOMC’s outlook of the U.S. labor market.

U.S. Wage Growth Fed’s Likely Focus

So, what we are looking for on Friday, then, is of course, new private sector jobs created in July. But, even more relevant than new jobs and the unemployment rate, is wage growth and the overall participation rate. First, the Fed will want to see wages rising by more than 2% (year-over-year). Second, they would like to see an increase in the participation rate (that is the percentage of “qualified” individuals actually in the work force). Currently, the market is anticipating that the Fed could raise interest rates as soon as September. The market’s supposition could be validated by strong performance in not just the actual NFP numbers, but wages and the participation rate, as well. If the market’s expectations are, indeed, validated by a strong performance in those parameters, that would support the U.S. Dollar. Conversely, a disappointment could weigh on the greenback, depending, of course, on how big a disappointment.

Remember, we mentioned last week that Janet Yellen, the Fed Chair, seemed to be leaning toward a single rate hike in 2015. However, quite a few of the other FOMC members were pushing for more than a single one this year. If the labor data is an all around beat, we could see Ms. Yellen changing her tune and hinting on another rate hike later in the year. That would be very much in line with a number of her compatriots’ way of thinking.

Decision Time for the Bank of England

Mark Carney, the Bank of England Governor, has in recent months notched up the hawkish rhetoric. Markets wonder if he will soon be putting his money where his mouth is. On Thursday, the BoE will be announcing its monetary policy decision. At the same time, they will be releasing the BoE’s official Quarterly Inflation Report which shows the bank’s inflation outlook. For ease of reference, the BoE target for inflation is 2%.

The BoE’s Monetary Policy Committee (MPC) had previously stated that they believe inflation risk was likely to notably increase before the year’s end. Further, the MPC believes that “unusually low contributions” of some of the core factors which make up the inflation rate are disguising the reality. And that is that the inflation rate would likely be closer to 1.5%, nearing the BoE’s threshold. If the Inflation Report shows the MPC’s growing concern over the inflation risk it could help crack the code for the timing of the next rate hike. If a rate hike looks closer, given greater inflationary fears, then the Pound Sterling could find support. At the same time, the London FTSE could turn softer. A signal that the BoE will continue on with its wait-and-see stance could provide support for the FTSE even as it weighs on Pound Sterling.

Down to Business

The U.S. labor market remains key for the Fed’s decision on timing of the next rate increase. If the NFP, wage growth and participation rate are positive, it could support the Dollar even as it puts pressure on Wall Street, Gold and Oil. However, and this is a big however, if the data undershoots expectations by a wide margin, you can believe the markets will quickly dispel any notion of a September rate hike.

On the plate

RBA Rate Decision(Tuesday) – If the RBA decides to cut rates on the back of China’s woes the Aussie could be hit.

BoE Rate Decision(Thursday) – If the Bank of England suggest rate hikes are closer than previously thought , then the Sterling could move higher especially against low yielders such as the JPY or the CHF.

Nonfarm Payrolls (Friday) – If the NFP posts a gain of more than 220K jobs it will support the dollar.

Average Hourly Earnings(Friday)- If wages grow by more than 2% YoY it will be viewed as a positive sign and a signal rate hikes are moving closer.

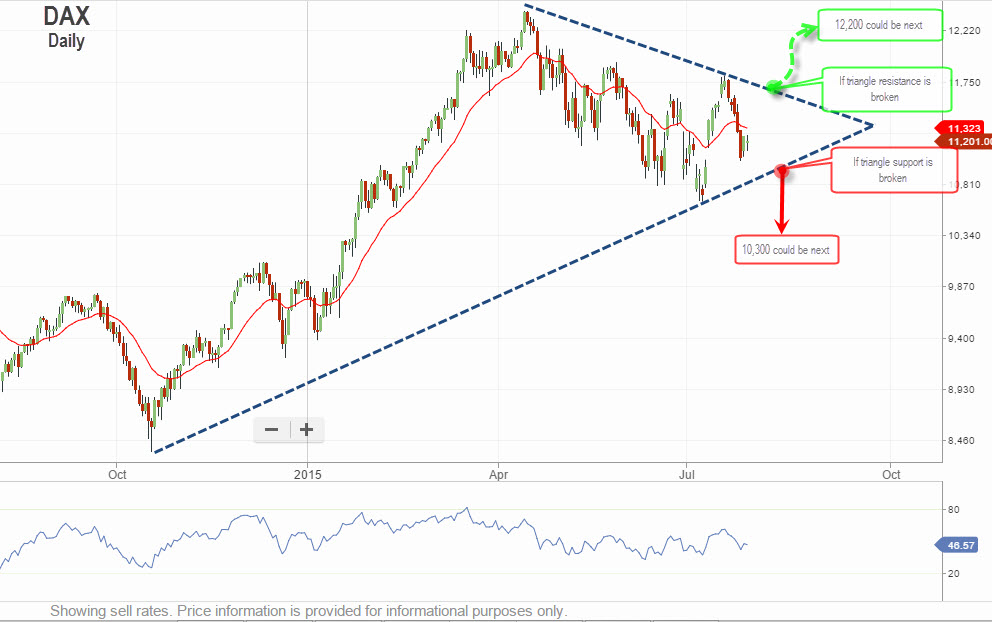

Chart of the week – DAX

Economic Calendar: