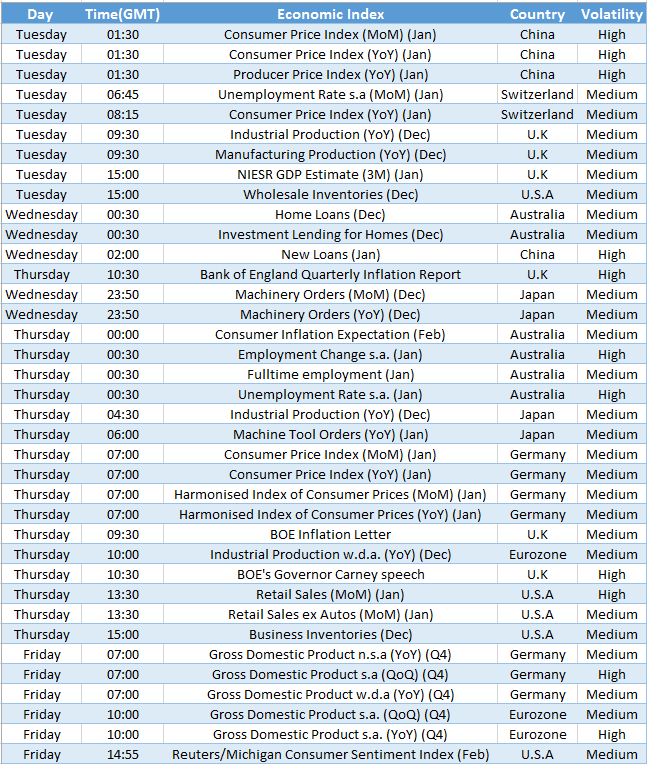

Sterling, Money Time?

This week, after several weeks of being forced to take a back seat, the Pound Sterling will finally get a chance in the driver’s seat. On the agenda will be the upcoming Bank of England Inflation Report followed by a speech from Mark Carney, the BoE Governor, due out this Thursday. For many Sterling watchers, this could be the money time for Sterling, the point at which the Pound Sterling will either rebound or won’t. Why? Investors are going to be putting a lot of weight behind the Inflation Report after a recent plunge in inflation figures, and after a soft patch in the UK’s economic growth which came about despite a better than 2.5% growth pace. What investors want to know is does the BoE think low inflation is transitory? If the answer is yes, then the MPC will signal that rate hikes plans might be still intact and, therefore, provide support for Sterling. But what if the Inflation Report shows that the MPC deems low inflation a prolonged phenomenon? Then the BoE Governor will have no choice but to voice a more dovish tune, a tune that could weigh on the Pound Sterling and postpone a potential rebound vs its American peer. However, if the Inflation Report presents inflation as transitory, Mark Carney would be free to paint a rosy picture, a picture where an improved job outlook and stable growth would drive inflation back up; a picture where rate hikes might still be on the plate. If this is the case, it could provide a fertile ground for the battered Pound Sterling to stage a comeback, even if only for a short while.

China Ready for More Easing?

Another data set that will be high on the radar will be inflation data coming from China. Chinese inflation data could, as always, have far reaching consequences beyond just the Chinese economy. If Chinese inflation cools to less than 1.5% YoY, it could pave the way to more easing from the Peoples Bank of China, perhaps in the form of a rate cut which will eventually favor commodities demand, yet could create a short term bearish selloff in the commodity space and in other China-oriented trades amid the “negative” news.” If CPI figures rise more than 1.5% YoY, however, it could mean that PBOC easing will come to a halt, at least in the near term, which could delay some of the potential gains in commodities over the long term while simultaneously making it possible for global equities to recover as it will signal that the Chinese dragon is stabilizing.

Retail Sales to Chill?

The final data set to watch for this week will be US Retail Sales figures which will be due out on Thursday. What trend will the Retail Sales figure point on? In the aftermath of the mildly disappointing US GDP figure and the release of the NFP numbers, investors will ponder how the US consumer is really faring. One must remember that this Retail Sales figure is a reading on January, after the Christmas buying spree in November and a -0.9% retreat in December. If the figure bounces back by more than 1% MoM, it will signal that the US consumer is back and spending and thus favor the US Dollar and, even more so, Wall Street.

Down to Business

Data from the US Retail Sales will mainly translate into Wall Street trading rather than the Dollar amid a growing sense among investors that it’s time to liquidate some Dollar profits and a feeling that the greenback might gravitate lower. Hence, a strong Retail Sales figure will mainly add a tail wind to the Dow and the S&P500. On the Sterling front, if rate hikes are still on the plate after the Inflation Report then Sterling may recover; however, if the Inflation Report put a big question mark on future rate hikes, then Sterling may face further weakness and dash hopes for a rebound.

On the Plate

Chinese CPI(Tuesday) – If Chinese CPI(inflation) will surge above 1.5% it could favour equities while being slightly negative for commodities. A lower reading however, could favour the commodity space on the long run.

Aussie Unemployment( Thursday) – If Aussie unemployment falls from 6.1% in the aftermath of the RBA rate cut, it could fend off some selling pressure on the Aussie.

BoE inflation report(Thursday) – One of the two major events of the week alongside the Carney speech. If the inflation report projects a recovery in inflation, sterling could rebound.

BoE Governor Speech(Thursday) – Perhaps the main event of the week. If Mark Carney will signal a U-turn in BoE policy by moving away from rate hikes, it could hit the Sterling. If Carney remains hawkish , this could assist a sterling rebound.

US Retail Sales (Thursday) – While dollar sentiment is expected to be subdued this week, a strong retail sales figure could still somewhat favour the currency. Nevertheless a rebound in retail sales of 1% MoM or higher, is expected to mainly benefit Wall Street.

Eurozone GDP(Friday) – In the 4th quarter GDP of the Eurozone investors rather than seek growth will seek to find just how severe the crisis is. If growth YoY is below 0.8%, it could weight on the Euro. A surge above 1% however, could ease selling pressure on the currency.

Chart of the Week – GBP/USD