Fed Rate Hike Back on the Table?

This week, trade will be dominated by one question and one question only: Is the US ready for a September rate hike? With the knockout NonFarm that hit the news wires earlier this month, posting a 280K gain and smashing estimates, investors are again warming up to that idea. Indeed, many investors share the belief that the recent soft patch in the US economy was simply transitory. So, what are we on the lookout for that could support investors’ collective beliefs? Two things, specifically: The Fed’s take and the latest inflation figures.

First up this week is the Federal Reserve’s policy decision due out on Wednesday. Now, this decision won’t come as it usually does with a press conference, so investors will be relying solely on the wording of the Fed’s announcement. What investors will want are answers from Janet Yellen and the FOMC, and plenty of them. Is employment finally sufficiently high? Is inflation stabilizing? Is growth improving?

Recall that the Fed is focused primarily on three dimensions of the economy, i.e. jobs, growth and inflation. Given the last few readings, we know that the US labor situation has greatly improved. In fact, experts deem US employment levels to now be sufficiently low to warrant a rate hike. Given the recent upbeat NFP figures, the Fed should be able to provide an answer to the first question. A positive response could suggest to investors that the Fed might be on the brink of a rate hike, perhaps in September, which would support the Dollar.

The Fed may answer the question on growth with some ambiguity given that Q2 growth figures will not be released until next month. As to the third question on inflation, the Fed might be somewhat cautious there, too, given that CPI figures won’t be released until Thursday.

On the whole, investors will be trying to gauge whether the Fed sounds upbeat. If the Fed sounds guarded, investors may then draw the conclusion that a rate hike might once again be postponed. That, of course, would be negative for the Dollar, and positive (possibly) for Wall Street.

Inflation Thresholds

When it comes to the actual inflation numbers what should you be watching for when CPI is released on Thursday? Since the Fed’s “comfort zone” is 2% per year that would naturally be the first level to watch. In reality, it would be pretty farfetched for headline inflation to reach 2% seeing how it’s currently “below freezing” at -0.2. However, if we look at core inflation, which neutralizes volatile components such as food and energy prices, the last reading hit 1.8%. So, when it comes to core inflation, investors could realistically expect a nice round 2%.

The second mark to focus on is related to headline inflation. There, investors are hopeful that the inflation gauge will return to positive territory from its current -0.2%. If both hopes are validated, i.e. core and headline inflation both hit their respective target, it will be an upbeat sign for the dollar. And Wall Street, too? Not necessarily, as Wall Street has become somewhat more vulnerable over the past several weeks.

Another Bombshell from Switzerland?

Early on Thursday, Swiss Franc watchers will be focused on the SNB policy statement. Remember, back in January the SNB surprised markets by untethering the Swiss Franc’s peg to the Euro. The SNB also surprised markets with aggressive movements, lowering the benchmark rate below zero.

Naturally, investors want to know what the SNB might have up its proverbial sleeve. Thus far, despite a negative benchmark rate of -0.75%, the Swiss economy is still deep in deflationary territory. Currently, the inflation rate is set at -1.2% year-on-year. That means, essentially, that Switzerland’s inflationary outlook is deteriorating and turning risky. Thus the SNB might be forced to drop yet another bombshell. That might come in the form of additional liquidity or another rate cut or even, perhaps, both.

Although there is a chance that the SNB will take a wait-and-see stance, investors are now accustomed to surprising and drastic measures. If the SNB acts or if it uses very explicit rhetoric of aggressive measures in its statement, CHF sells would have the upper hand. That means that both the EUR and USD could gain against their Swiss peer. But, if there is no action from the SNB nor is there any hint of action, then EUR/CHF and USD/CHF could once again gravitate lower.

Down to Business

While the Swiss National Bank’s announcement will be critical for the CHF trade, markets will primarily focus on the US. On Wednesday, we have the week’s main event, the Federal Reserve policy decision. If the Fed seems generally upbeat, investors will raise their bets on a rate hike coming sooner rather than later.

If, however, the Fed sounds wary, then investors will expect the rate hike to be pushed back yet again. In the case of the former, the dollar could be supported while the case for the latter could be negative for the dollar, though it might support Wall Street equities. Thursday’s CPI release takes a back seat to the Fed announcement, of course, but investors will be able to use the data to better gauge the likelihood of a Fed rate hike. If, as we just mentioned, both headline and core inflation hit their respective thresholds, then the dollar could be, once again, on a stronger footing, as rate hike bets will surge. As Wall Street sentiment becomes shakier, an upbeat inflation reading, which would bring forward rate hike prospects, could spell trouble for stocks and indices.

On the Plate

RBA Meeting Minutes(Tuesday) – Will reveal the protocol of the RBA’s latest rate decision. If indeed the protocol reveals that there is a chance for another rate cut, the Aussie could face some downward pressure.

UK Core CPI(Tuesday)- If UK core inflation crawls closer to 1% it will signal that inflation in the UK is returning gradually and a rate hike while still distant, is now seen across the horizon, which is Sterling positive.

German ZEW Index(Tuesday)- If the German ZEW index which measures sentiment across the German economy moves higher then it will be a positive sign for the Euro and could potentially support the DAX .

ECB Non Policy Meeting(Wednesday)- Despite the meeting not being a monetary meeting , any mention of high profile subjects such as more liquidity or the manner in which the ECB would handle Greece could generate swings in the Euro rate.

BoE Meeting Minutes(Wednesday)- If the BoE meeting minutes reveals that the BoE has turned less dovish and perhaps sees inflation as stabilizing it could be a positive sign for the Sterling.

UK ILO Unemployment (Wednesday)- If UK unemployment falls below 5.5% it will be considered highly positive for the Sterling. A no change from 5.5% will have no effect, while a move higher could expose the sterling to selling pressure.

FOMC Rate Decision(Wednesday)- The main event of the week. If the Fed will use rhetoric that will suggest a rate hike in September, the dollar could gain while Wall Street could potentially slide and vice versa.

SNB Rate Decision(Thursday) – Investors will be keen to see whether the SNB will announce or at least suggest rates in Switzerland could be slashed further below -0.75% . If this will be the case the CHF could face a hefty selloff.

US CPI&Core CPI(Thursday) – If US Core inflation will move closer or even hit 2% it will be considered highly positive for the US dollar and will raise prospects of a rate hike.

BoJ Minutes(Friday)- The protocol of the BoJ on the back of governor Kuroda’s speech last week on the Yen being fairly valued , will be highly watched and could affect Yen sentiment.

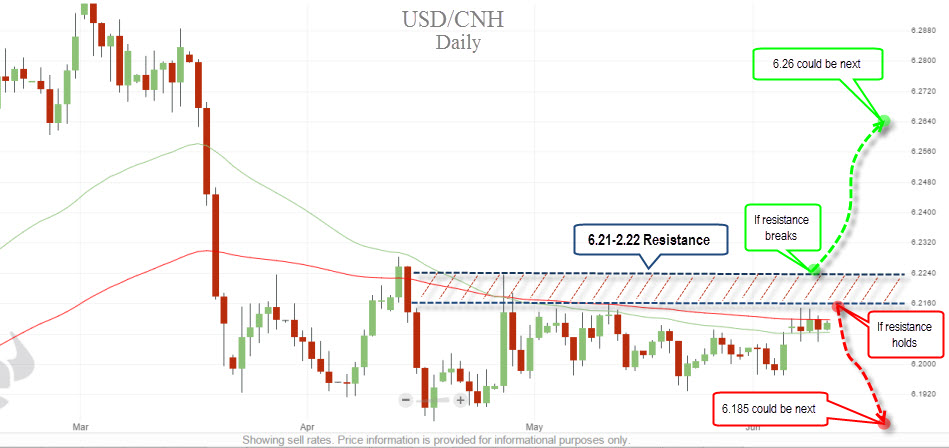

Chart of the week – USDCNY

Economic Calendar: