Will the Fed Finally Lose its Patience?

This week, all the worries over Greece, the slowdown in China or any other economic data will be shrugged off as investors prepare for this week’s main attraction, the FOMC rate decision.

For a long while now, a majority of investors have been expecting the Fed to raise rates, possibly as early as June, and with each and every Fed meeting, that tension and the accompanying drama grows. This week, investors expect a very important change of tone in the Fed’s statement; specifically, the dropping of the word “patience.” In the last several policy statements, the Fed had replaced its pledge for low interest rates over a prolonged period of time with the word “patience,” inferring that patience is warranted before rates will rise. Yet this week, after the knockout 295K Non-farms figure of two weeks ago, the Fed is expected to finally drop its pledge for patience and thus prepare us for a rate hike that could occur, in fact, during any future meeting. If, indeed, this change does occur it will be nothing short of dramatic, because after more than seven years, the Fed, for the first time, is at last ready to tighten the screws. For FX investors this could lead to another buying spree in the Dollar, even after such hefty gains over the past several months. For Wall Street, this could blunt investors’ appetite for pushing indices higher. As for commodities, higher rates tend to lead to bearish sentiment, at least in the short term. Put another way, if this is truly what’s cooking among the Fed’s decision makers, then it’s a recipe for a higher dollar and lower everything else, at least for the short term. However, if Yellen proves to be more dovish than expected and keeps the word “patience” in the Fed statement, a sigh of relief may be heard on Wall Street and in the commodities space, while profit taking could cause the Dollar to retreat.

Sterling Cooking a Comeback?

Sterling bulls, much like Dollar bulls, seem to hang their hopes on the job market. With low inflation putting a big question mark on rate hikes, Sterling investors hope that strong jobs growth will allow wages to rise which will consequently allow inflation to rise back and, as you guessed it, put rate hikes in the UK back on the agenda. As one might expect, this is a most welcome scenario among Sterling bulls and a rather worrying prospect for Sterling bears. With Sterling bears and bulls in an intensive battle for supremacy over Sterling sentiment, volatility around Sterling is expected to rise this week as UK unemployment figures are due. If, indeed, unemployment continues to plunge even lower than 5.7% and wages grow more than 2% YoY, this will suggest that a BoE rate hike, while not imminent and perhaps not even set to occur this year, may likely still be on the horizon. If this is indeed the case, Sterling bulls could regain the upper hand and push Sterling higher against its peers, and perhaps even against the Dollar in the event the Fed is more dovish than expected. But if there is no positive surprise and the BoE minutes, which are due out at the same time, reveal an as-expected rather dovish BoE, Sterling shorts could begin to weigh and push the currency even lower against the Dollar and experience a correction vs the Euro and the Yen.

Down to Business

Patience is the name of the game. If the Fed drops the word “patience” in its policy statement this Wednesday it will ignite a shift in markets in preparation for a rate hike in the US, perhaps as early as June. This naturally tends to benefit the Dollar vs its peers, while on Wall Street, at least in the short run, it could spell profit taking. Commodities, which are already on shaky ground, will be exposed to additional short selling. If, however, the Fed does not drop the word patience it would raise estimates that the Fed is not ready to raise rates this summer, which could lead to some long awaited Dollar profit taking while Wall Street and commodities could edge higher.

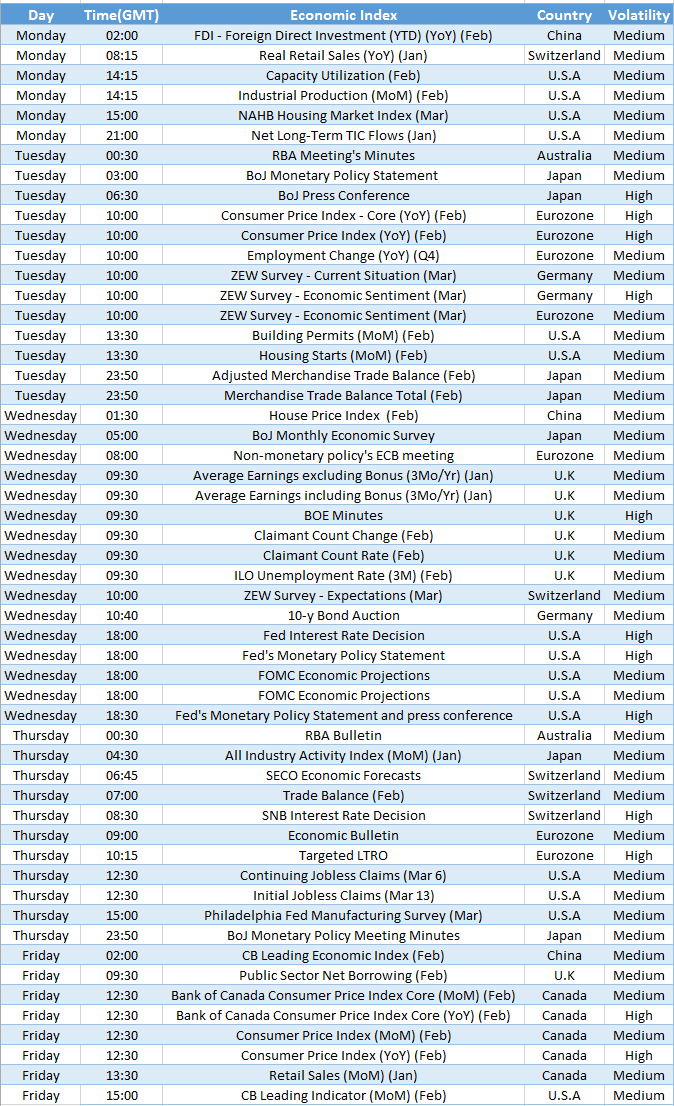

On the Plate

BoJ Rate Decision (Tuesday) – After mild results from the Japanese economy many expect more easing to come from the BoJ. If indeed the BoJ introduces even more easing in this week’s meeting, Yen pairs could surge amid a falling Yen (Yen pairs rise when the Yen falls).

Eurozone Inflation (Tuesday) – Since low Eurozone inflation is the key reason for ECB easing in the first place, the outcome could have a significant impact on Euro sentiment. If CPI (inflation) moves even lower than last month’s -0.6% YoY, more selling pressure could come for the Euro.

BoE Minutes (Wednesday) – Will the BoE become more dovish or hawkish? After rather dovish minutes last month, another round of dovishness could derail Sterling appetite.

UK Unemployment(Wednesday) – IF UK unemployment will fall below 5.7% and closer to full employment , combined with a more upbeat BoE the Sterling could recover.

FOMC Rate Decision (Wednesday) – Undoubtedly the most important event of the week. If the Fed decides to lose the word patience it could signal rate hikes are getting close and thus ignite more dollar appetite.

SNB Rate Decision (Thursday) – Will the Swiss National Bank cut rates to -1%? If indeed the SNB cuts rates once more, the CHF could be hit hard especially versus the US Dollar.

Chart of the Week – Gold