Last night UK Prime Minister Boris Johnson was admitted to intensive care after his coronavirus symptoms worsened. Foreign Secretary Dominic Raab will deputise for the Prime Minister where needed as he receives treatment. Despite this concerning news, markets have continued their rally this morning with the UK’s FTSE100 up over 3% and Germany’s Dax up 4.5%. US futures point towards a firmer open between 2 and 3%.

Global stocks soared on Monday, driven by optimism that the spread of Covid-19 in the US and other key markets may be passing through its peak. In New York, the epicenter of the US coronavirus outbreak, Governor Andrew Cuomo said on Monday that there had been two consecutive days of falling hospitalisations and intensive care admissions.

However, despite the positivity — which sent the major US stock indices more than 7% higher — some analysts are warning investors to be cautious. Matt Maley, chief market strategist at trading firm Miller Tabak, cautioned that in the decade-long bull market many firms “loaded up to the gills in terms of debt” and as they deleverage themselves “that is going to keep the economy from picking back up the way it did following the 2018 deep correction.”

Currently, economic data and warnings from industry leaders are playing second fiddle to sentiment surrounding the spread of the virus. It is worth noting that bear markets often feature so-called “bear trap” rallies. On Monday, JPMorgan CEO Jamie Dimon predicted that a “bad recession” is incoming, with US unemployment reaching as high as 14% in a severe scenario. While investors appear to be glossing over worse-than-expected unemployment numbers, corporate earnings season kicks off next Tuesday when JPMorgan, Johnson & Johnson and Wells Fargo all report their Q1 2020 (calendar) results. Company-by-company earnings data and details from firm leaders will be closely watched.

Hardest hit stocks lead Monday’s rally

The Dow Jones Industrial Average posted the biggest day of the three major US stock indices yesterday, gaining 7.7%. It was led by Boeing and American Express, both of which were hammered last week. All 30 of the Dow’s constituent stocks were in the green, with all of them gaining more than 2%.

In the S&P 500, which gained 7%, it was the information technology, utilities and consumer discretionary sectors that posted the best start to the week. The biggest winners on Monday were many of the retail and travel names that have been hardest hit by the bear market. Grocery giant Kohls popped 22.9%, while hotel heavyweight Marriott International gained 19.5%. The two stocks are still down 72.2% and 53.4% year-to-date respectively. Oil names also posted a positive day, with Chevron and ExxonMobil gaining 7% and 3.2% respectively, after President Trump said on Monday that US oil output is expected to fall due to market forces as demand drops off, implying that the US could be part of a broad international production cut deal. Russia and Saudi Arabia-led Opec are expected to meet later this week, having delayed the meeting once already, although terse public exchanges between the parties involved imply any deal hangs on a knife edge.

S&P 500: +7% Monday, -17.6% YTD

Dow Jones Industrial Average: +7.7% Monday, -20.5% YTD

Nasdaq Composite: +7.3% Monday, -11.8% YTD

easyJet founder attacks airline over £4.5bn plane order, hints at bribery and threatens to sue

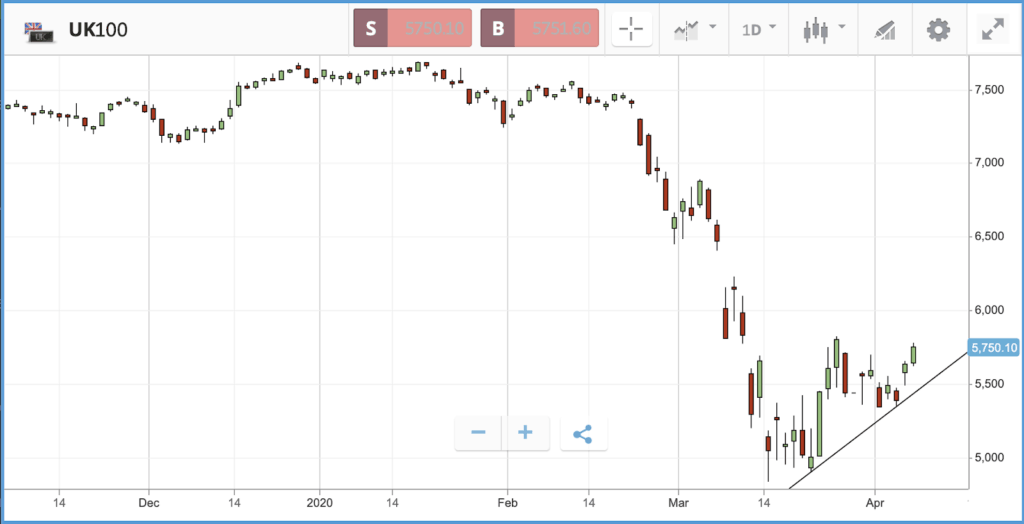

London-listed small cap stocks partially closed the gap to the UK’s biggest companies yesterday, with the FTSE 250 gaining 5.1% to the FTSE 100’s 3.1%. The FTSE 250 was led higher by double digit gains from constituents including gambling company William Hill, security firm G4S and serviced office space provider IWG. In the FTSE 100, Rolls Royce, turnaround specialist Melrose Industries, and Legal & Group, were the biggest winners, all gaining more than 15% — along with cruise firm Carnival, easyJet and more. It was far from a smooth day for easyJet, however, after the company’s founder and biggest investor Sir Stelios Haji-Ioannou attacked the firm in an open letter, warning that he might sue the company’s directors for a breach of their fiduciary duty over recent cash burn. He said that his main goal is to terminate a £4.5bn order of “107 additional useless aircraft” from Airbus, which he said “is the only way to preserve the value for all shareholders and all the bond holders, too.” The damning letter describes Airbus as a company “that has been convicted of bribing airline executives around the world” and said that easyJet could run out of money by August if the order is not cancelled. Sir Stelios described assumptions that the easyJet fleet will return to the skies in June as “wildly optimistic”.

FTSE 100: +3.1% Monday, -26% YTD

FTSE 250: +5.1% Monday, -32.3% YTD

What to watch

Levi Strauss & Co: Clothing firm Levi Strauss & Co is reporting its first quarter 2020 earnings on Tuesday, providing one of the first glimpses into how a retail business that relies on discretionary consumer spending has held up amid the economic shutdown and disruption to supply chains induced by the pandemic. The firm has essentially been online only since mid-March, and investors will be watching closely for whether there has been any uptick in online sales to offset the damage done by the physical store closures. Levi’s share price is down 43.3% year-to-date, a much steeper fall than the wider market, with its $10.94 share price well below its $17 IPO price of a year ago.

Samsung: On Tuesday South Korea-time, technology goliath Samsung announced its Q1 earnings, facing fears that the pandemic disruption to its operations and the impact on demand for consumer electronics, would hamstring the company. However, with more people working from home and shopping online, demand for Samsung’s memory chips has picked up in order to keep data centers running. First quarter profit of $5.2bn came in ahead of expectations, and was an increase on Q1 2019. The company also makes only a small portion of its smartphones in China, which hurt key rival Apple. Samsung’s US competitor said in February that it does not expect to meet revenue targets, in part due to supply constraints.

Job openings: This data point is one to watch more as a reference point for next month as Tuesday’s release is for February and won’t include the worst days of the coronavirus pandemic in the US. The data will reveal the number of unfilled jobs in the US on the last day of February, as calculated by the Labor Department. For December, that figure came in at 7.48 million, followed by 7.58 million for January. This statistic will be an interesting one to watch in the coming months; in the middle of large numbers of layoffs and furloughed workers, companies including Amazon and Walmart are looking to take on huge numbers of staff to deal with pandemic-induced demand.

Crypto corner:

The world’s three major cryptoassets all continued an upward grind on Monday, with little to slow their march.

Bitcoin started the day below $6800 but reached above $7400 before trading back down to around $7274 this morning. Ethereum likewise surged, peaking at $175.74 before trending back below $170 this morning. Finally, XRP grew across the day before surging around midnight to $0.2025 before falling away to $0.1957 this morning.

The Bank of England will be hosting a webinar today discussing the potential merits of a Central Bank Digital Currency (CBDC). The webinar will be hosted by the bank’s Director of Fintech and will feature opinions of industry experts as the central bank looks to explore the risks and benefits of launching their own digital currency.

eToro (UK) Ltd is authorized and regulated by the Financial Conduct Authority. eToro (Europe) Ltd is authorized and regulated by the Cyprus Securities and Exchange Commission. eToro AUS Capital Limited is regulated by the Australian Securities and Investments Commission, ABN 66 612 791 803, AFSL 491139.

This is a marketing communication and should not be taken as investment advice, personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without having regard to any particular investment objectives or financial situation, and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication, which has been prepared utilizing publicly-available information.

eToro is a multi-asset platform which offers both investing in stocks and cryptoassets, as well as trading CFDs.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 62% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work, and whether you can afford to take the high risk of losing your money.

Cryptoassets are volatile instruments which can fluctuate widely in a very short timeframe and therefore are not appropriate for all investors. Other than via CFDs, trading cryptoassets is unregulated and therefore is not supervised by any EU regulatory framework. Your capital is at risk.