Summary

Focus: Exposure to crypto through equities

Getting exposure to crypto through equities may suit some. They have a record of beating the S&P 500, a decent relationship with the bitcoin price, but often with much lower volatility. The number of crypto-related equities is small but growing. It ranges from crypto investors (like MSTR), miners (RIOT), and exchanges (COIN), through to larger and more diversified suppliers (NVDA), adopters (SQ), and banks (STAN.L). Smart Portfolios give some broader options, like @BitcoinWorldWide, @FuturePayments, and @Chip-Tech.

Markets getting nervy

It was a nervous week for markets with back-to school seasonality, and more virus-driven growth concerns after prior week US payrolls shock. We see markets well-supported, with some pick up in volatility to be expected, but growth concerns to ease. Global new virus cases have been falling for 3 weeks now. Japanese equities surged on political hopes, whilst China’s tech crackdown spread to gaming, and UK equities were hit by new tax hikes. See our global markets summary presentation here for background.

Chances of a new Fed Chair

President Biden is to decide soon on Jerome Powell’s re-appointment at the Fed. Not doing so is low probability, would shock markets, but also likely be a buying opportunity.

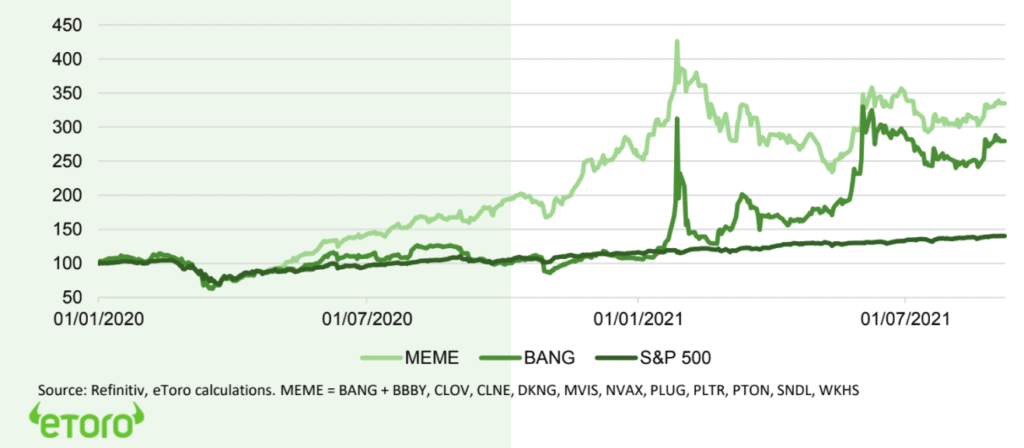

Meme stocks not going away

Our Meme stock index, led by GME, is still well above January levels, as broad retail equity interest stays high. 17% of investors own, per our survey, for many diverse reasons.

Real estate resurgence

Real estate is the 2nd best performing asset this year, after crypto. Surging residential (like AVB), retail (KIM), and industrial (PLD) segments have offset weak office (ARE) and hotels (HST). Low bond yields make their cash flows more valuable and dividends attractive. The tax advantaged REIT structure is defensive to hikes.

Bitcoin ‘flash crash’ and ALGO rally

Bitcoin (BTC) plunged 20%, before a partial recovery, on teething problems with El Salvador launch of legal tender and the SEC’s regulatory face-off with crypto exchange Coinbase (COIN). Algorand (ALGO) soared, becoming one of the top-20 largest coins, as it is being used for El Salvador digital infrastructure rollout.

Hurricane Ida drives new natural gas highs

Hurricane Ida shutdown 75% US Gulf of Mexico oil production, or 1.5% of global total, supporting oil and boosting soaring natural gas prices; now +98% this year. This storm season has seen 3 of an estimated 7-9 hurricanes so far

The week ahead: inflation spotlight

1) US inflation (Tue) with investors looking for further stabilization at last month’s 5.4% rate, as Fed considers tightening. 2) China monthly data, from industrial production to retail sales. Weakness may trigger stronger policy support. 3) Four-time annual ‘quadruple witching’ (Fri). Stock and index futures and options all expire, and this often generates some volatility.

Our key views: Staying the course

We see a positive outlook of 1) vaccine rollout and economic re-opening, and 2) still huge policy support, offsetting virus third wave and Fed tightening risks. We like assets helped by this growth: equities, commodities, crypto, and are cautious fixed income, and the USD.

Top Index Performance

| 1 Week | 1 Month | YTD | |

| DJ30 | -2.15% | -2.56% | 13.07% |

| NASDAQ | -1.69% | -0.21% | 18.70% |

| SPX500 | -1.61% | 1.97% | 17.28% |

| UK100 | -1.53% | -2.63% | 8.80% |

| GER30 | -1.09% | -2.30% | 13.78% |

| JPN225 | 4.30% | 8.60% | 10.70% |

| HKG50 | 1.17% | -0.70% | -3.76% |

*Data accurate as of 13/09/2021

Market Views

Markets getting nervy

- It was a nervous week for markets. The S&P 500 fell 1.5% with poor back-to-school seasonality, and more virus-driven growth concerns after prior week US payrolls shock. We see markets well-supported, with some pick up in volatility expected after huge rally, but growth concerns to ease. Global new virus cases have been falling for 3 weeks. Japanese equities surged on political hopes, whilst China’s tech crackdown spread to gaming, and UK equities were hit by new tax hikes. See our latest global markets summary presentation here for background.

Three election nail-biters

- Coming weeks see elections in 3 of the world’s top economies. We see more spending from new governments in Germany (September 26 election with centre-left SPD leading polls) and Japan (youthful vaccine czar Taro Kano leads polls in ruling LDP party election on September 29) helping their markets. But likelihood of more sector intervention is a concern in Canada (vote on September 20 with Liberals favourite).

Chances of a new Fed chair

- President Biden is to soon decide on re appointing Jerome Powell as US Federal Reserve chair. His 5-year term ends in February. Markets are overwhelmingly expecting his re appointment versus other candidates, led by Fed governor Lael Brainard. Not re-appointing Powell is a low probability risk that would shock markets. This would be a buying opportunity.

Meme stocks not going away

- January’s Meme stock phenomena has not gone away. Our two meme stock baskets (see chart) are off their highs but still well-above January levels. GameStop (GME) is 10x higher. R/Wallstreetbets added 1.5 million more subscribers since March. Further meme stock ETFs have launched. More broadly, US household equity investments are at a record, and US equity funds saw $900 billion of inflows in first half alone, a 30-year record.

- Our global retail investor survey showed 17% of polled investors owned meme stocks, less than perceived but still a lot, and with a wide spread between countries, from 30% in Romania to 10% in Australia. The reasons for owning were also balanced, led by to ‘make money’ (35%), then ‘believe in the fundamentals’ (27%), and followed by ‘entertainment’ (26%).

Real Estate resurgence

- REITS Real estate investment trusts (like ETF’s XLRE, IYR) are the 2nd best stock market performer among all 30 industries this year. This may seem surprising given return-to-work office issues, and tourism struggles for hotels. These segments have lagged, but are more than offset by surging residential (stocks like AVB), retail (KIM), and industrials (PLD), highlighting the diversification available within the sector.

- This also makes listed real-estate the 2nd best performing asset class this year, behind only crypto, and a big rebound from bottom-of-the asset-class -5% last year. REITs benefit from low for longer bond yields, making their long-term cash flows more valuable, and high dividends more attractive. Their tax-advantaged structure is also defensive to corporate tax hikes.

Meme stocks vs the S&P 500 (Jan. 1, 2020 = 100)

Bitcoin ‘flash’ crash and ALGO rally

- Bitcoin (BTC) saw a ‘flash’ crash last week, down 20% at one point before partially recovering. The sell-off was driven by teething problems as El Salvador became the first country globally to launch bitcoin as legal tender, and we saw further signs of a SEC regulatory crackdown, now against leading exchange Coinbase (COIN).

- Algorand (ALGO) was among the exceptions to the crypto sell-off, able to rally further, and is now the 20th largest market capitalisation coin. Algorand is the blockchain being used to build out El Salvador’s digital infrastructure.

Energy helped by hurricane Ida

- The broad-based Bloomberg commodity index rose 0.5% last week, resilient to the stronger USD and with China moving to sell oil from its strategic reserve to contain rising prices.

- Oil prices have been supported by the big impact from recent hurricane Ida which has shutdown ¾ of Gulf of Mexico oil production, equivalent to 1.5% of global production. The hurricane season ‘officially’ ends November 30, with forecasts for an above-average season with 7-9 hurricanes vs the 3 seen so-far.

- Natural gas is the strongest energy performer, up 98% this year, and boosted 6% last week. Strength has been driven by robust domestic demand, competition for US LNG exports and, now production cuts caused by Hurricane Ida.

US Equity Sectors, Themes, Crypto assets

| 1 Week | 1 Month | YTD | |

| IT | -1.78% | 2.35% | 21.68% |

| Healthcare | -2.63% | 0.34% | 15.09% |

| C Cyclicals | -0.50% | 0.83% | 12.37% |

| Small Caps | -2.81% | -0.53% | 12.80% |

| Value | -2.02% | -1.35% | 15.96% |

| Bitcoin | -9.48% | 0.37% | 58.75% |

| Ethereum | -15.79% | 5.90% | 342.72% |

Source: Refinitiv

The week ahead: Inflation spotlight

- Latest US inflation numbers (Tue), with investors looking for stable (5.4% vs last year) or lower number, to allow Fed to keep going slow on its journey to tighten monetary policy.

- See China’s data dump (Wed), from industrial production to retail sales, after recent signs of macro slowdown. Any bad news may be good news here, with the amount of new stimulus the authorities could launch if needed.

- Four-times annually ‘quadruple witching’, (Fri) with stock and index futures and options all expiring, and often generating volatility.

- A very light earnings week with only $250 billion market cap. cloud computer Oracle (ORCL) of major companies reporting.

Our key views: Staying the course

- We see a positive scenario of 1) global vaccine rollout and economic re-opening, 2) still large policy support of low interest rates and fiscal expansion. This is resilient to current volatility.

- The main risk is Fed monetary policy tightening, which we see as gradual and well-flagged, alongside growth risks from the third Covid virus wave, which we see as peaking soon.

- We focus on so-called reflation and cyclical assets that benefit most from the growth rebound: commodities, crypto, small cap, and value equities. We are more cautious on fixed income, the USD, defensive equities and China.

Fixed Income, Commodities, Currencies

| 1 Week | 1 Month | YTD | |

| Commod* | -0.01% | 2.03% | 24.41% |

| Brent Oil | 0.65% | 3.84% | 41.05% |

| Gold Spot | -2.28% | 0.38% | -5.96% |

| DXY USD | 0.66% | -0.13% | 3.01% |

| EUR/USD | -0.57% | 0.12% | -3.32% |

| US 10Yr Yld | 1.54% | 5.52% | 42.21% |

| VIX Vol. | 27.67% | 35.60% | -22.03% |

Source: Refinitiv. * Broad based Bloomberg commodity index

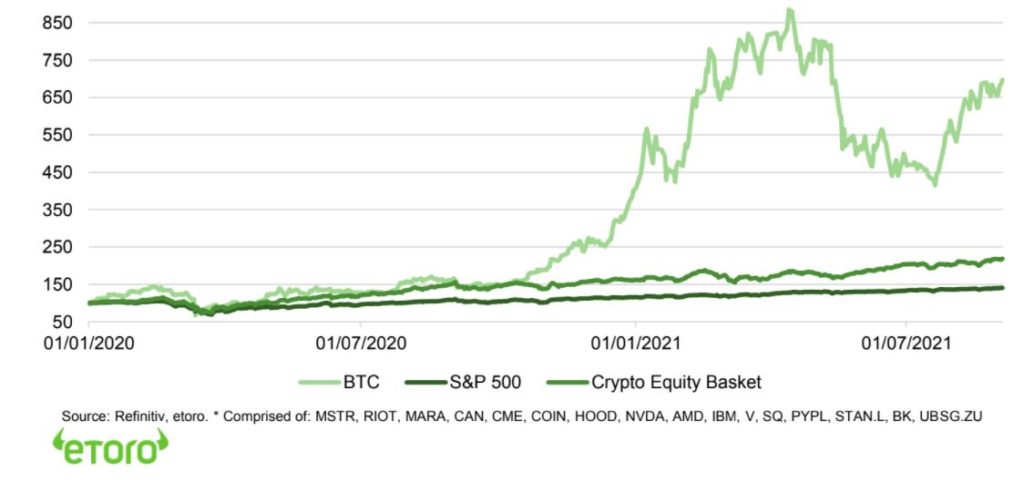

Focus of Week: Crypto equity exposure

Getting exposure to crypto through equities may suit some

We look at stocks that are exposed to crypto-assets, as 1) a lower risk alternative for equity investors looking for crypto exposure, or as 2) possible diversification for crypto-only investors. The bad news is that looking back over the last year and a half, bitcoin price performance has left equities in the dust (see chart below). Also, there are not many crypto-related equities to choose from – maybe 30 have relevant crypto exposure today, though this is rapidly increasing. The better news is that crypto-related equities have done much better than the S&P 500, no little feat given its own strong performance. They have also done this with significantly lower price volatility than bitcoin itself. Many of these equities also pay dividends, giving an attractive compounding income stream not available with proof-of-work bitcoin.

The strongest flavours, from investors to miners, and exchanges

The stocks most exposed to crypto coin prices are equity Investors, such as MicroStrategy (MSTR), whose 109,000-bitcoin holding value is equivalent to 80% its current market capitalisation. Also, Miners such as Riot Blockchain (RIOT), Marathon Digital (MARA) and related suppliers like Chinese ASIC maker Canaan (CAN). These are small companies, that are often riskier than crypto itself, but come closest to matching bitcoin huge recent performance. Exchanges is a new and growing segment, with high bitcoin exposure, led by dominant bitcoin futures exchange CME (CME), alongside recently listed crypto-exchange Coinbase (COIN), and online brokerage Robinhood (HOOD), where crypto revenues were 41% of its total last quarter.

Mid flavour from adopters, suppliers, and banks

Bigger companies that are helping grow the crypto ecosystem include suppliers such as GPU chipmakers Nvidia (NVDA) and Advanced Micro Devices (AMD) and blockchain tech integrators such as IBM (IBM). Early payment adopters like Visa (V), Square (SQ), and Paypal (PYPL) are enabling crypto usage across their platforms and merchants. Finally, several traditional banks are investing in their crypto capacities and making large outside investments, led by Standard Chartered (STAN.L), Bank of New York (BK), and UBS (UBSG.ZU). These are all very large companies that are helping facilitate and grow adoption and use cases.

Smart Portfolios go broader; @BitcoinWorldWide, @FuturePayments, @Chip-Tech

Broader exposure is available through Smart Portfolios. @BitcoinWorldWide invests 25% in bitcoin and 75% in 28 companies in the bitcoin value chain including the companies mentioned above. @FuturePayments invests 25% in top crypto coins and 75% in related mobile, wearable, and digital payments. Finally, @Chip Tech invests across 35 of the leading global semi-conductor stocks enabling the industry.

Bitcoin vs S&P 500 and Crypto Equity Basket* (100=Jan. 1, 2020)

Key Views

| The eToro Market Strategy View | |

| Global Overview | Positive scenario of 1) global vaccine rollout and economic re-opening, 2) support from low interest rates and government spending. Main risk is from US Fed monetary policy tightening, but will be well-signalled and very gradual. Economies are increasingly resilient new virus case ‘waves’. Focus on most growth sensitive assets: equities, commodities, crypto, small cap and value. Relative caution on fixed income, USD, defensive equities and China. |

| Traffic lights* | Equity Market Outlook |

| United States | World’s largest equity market (55% of total) seeing strongest GDP recovery in 30-years driving earnings upside ‘surprise’, and a rare third consecutive year of 10%+ equity market returns. Valuations at 21x P/E are 25% above historic levels but supported by still low bond yields and strong earnings growth outlook. See further cyclicals and value catch-up, after a decade of underperformance, whilst tech is well supported by its structural growth outlook. |

| Europe & UK | A big beneficiary of the global growth rebound. Helped by 1) a greater weight of sectors most sensitive to the growth rebound, and lack of tech, 2) 25% cheaper valuations than the US, 3) a decade of under performance has made under-owned by global investors. Combination of lower-for-longer ECB plus multi-year €750bn ‘Next Generation’ government spending to drive European GDP and earnings growth more than the US, for the first time in a decade. |

| Emerging Markets (EM) | China, Korea, Taiwan dominate EM, with 60% weight, and is more tech-centric than US. China has world’s strongest GDP growth, and benefitted from being ‘first in, first out’ of crisis, but its tech sector crackdown is hurting the market. LatAm and Eastern Europe have more upside to vaccine rollouts, global growth recovery and higher commodities. |

| Other International (JP, AUS, CN) | Canada and Australia benefit from strong equity market weight in commodities and financials, as global growth rebounds and bond yields set to rise. Japanese equities among cheapest of any major market and vaccination rates accelerating, but has structural headwinds of low GDP growth, an ageing population, and world’s highest debt. |

| Traffic lights* | Equity Sector & Themes Outlook |

| Tech | The broad ‘tech’ sector of IT, communications, and parts of consumer discretionary (Amazon, Tesla), dominates US and Chinese markets. Expect a more subdued 2021 after dramatic 2020 rally. But are structural stories with good growth, high profitability, and clean balance sheets that justify high valuations, and should continue to rise. |

| Defensives | Healthcare, consumer staples, utilities, and real estate sectors traditionally offer more defensive cash flows, less exposed to changes in economic growth. This has also made them more sensitive to rising bond yields. We expect them to relatively underperform in the current cyclicals focused environment with growth and earnings strong. |

| Cyclicals | We expect cyclicals – consumer discretionary (autos, apparel, restaurants), industrials, energy, and materials, to lead market performance. They are most sensitive to the sharp economic recovery and higher bond yield outlook, with more sensitive businesses, depressed earnings, cheaper valuations, and have been out-of-favour for many years. |

| Financials | Financials will benefit from the GDP growth recovery, with higher loan demand and lower defaults. Similarly, they benefit from higher bond yields outlook, charging more for loans than they pay for deposits. Sector has cheapest P/E valuation of any, and regulators recently giving flexibility to pay large 8-10% dividend and buyback yields. |

| Themes | We favour small cap vs large, on more GDP growth exposure, earnings upside, and domestic focus. Similarly, value over growth on GDP recovery, lower valuations, under-ownership after decade under-performance. Dividends and buybacks recovering with cash flows. Power of dividends under-estimated, at up to 1/2 of total long term return. |

| Traffic lights* | Other Assets |

| Currencies | We see modest USD weakness as the rest-of-world GDP growth recovery accelerates, and fears over a virus ‘third wave’ ease. A stable or weaker USD traditionally supports Emerging Markets, commodities, and large US foreign earners, such as the tech sector, and could be a modest headwind to large exporters, such as Europe. |

| Fixed Income | US 10-year bond yields to rise modestly as inflation above 2% average Fed target, ‘real’ inflation-adjusted yields negative, Fed to gradually tighten policy. Will be modest as inflation expectations already high, wide spread to other market bond yields, and structural headwinds of all-time high debt, poor demographics, and low productivity. |

| Commodities | Commodities supported by record-breaking GDP growth rebound, ‘green’ industry demand, years of supply underinvestment, and a stable or weaker USD. Industrial metals (copper) and battery materials seem best positioned, whilst oil price supported by only slow return of OPEC+ supply. Gold hurt by outlook for higher bond yields. |

| Crypto | Institutionalization of bitcoin market barely begun, as asset class benefits from very strong risk-adjusted returns and low correlations with other assets. Altcoins have outperformed as see broader interest and use cases. Clear supply rules a benefit as inflation rises. Volatility remains very high, with the 15th -50% pullback of the last decade. |

| *Methodology: | Our guide to where we see better risk-adjusted outlook. Not investment advice. |

| Positive | Overall positive view, and expected to outperform the asset class on a 12-month view. |

| Neutral | Overall neutral view, with elements of strength and weakness on a 12-month view |

| Cautious | Overall cautious view, and expected to underperform the asset class on a 12-month view |

Source: eToro

Analyst Team

| Global Analyst Team | |

| CIO | Gil Shapira |

| Global Markets Strategist | Ben Laidler |

| United Kingdom | Adam Vettese Mark Crouch Simon Peters |

| France | Antoine Fraysse Soulier David Derhy |

| Iberia/LatAm | Javier Molina |

| Italy | Edoardo Fusco Femiano |

| Poland | Pawel Majtkowski |

| Romania | Bogdan Maioreanu |

| Asia | Nemo Qin Marco Ma |

| Australia | Josh Gilbert |

COMPLIANCE DISCLAIMER

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.