Analyst Weekly, April 13, 2026

If oil is the major macro driver in markets, China equities are not the obvious casualty. Historically, energy shocks have triggered rotation and repricing in Chinese markets but not fundamental deterioration, which is why positioning matters more than direction.

Resilience with a Policy Backstop

China is not insulated from global volatility. Still, we think it could be better positioned than many peers.

Several buffers stand out:

- Coal-heavy domestic energy mix

- Strategic reserves covering around 60 to 90 days of oil demand

- Interbank rates are still low

- Fund issuance has slowed but not collapsed

- EPS revisions for 2026 are holding up better than 2025

- Most importantly: state-backed liquidity support

Investment Takeaway: The state remains a key marginal buyer in China’s equity market. After stepping in heavily over the past two years, state funds have recently pulled back, suggesting dry powder exists if markets weaken again.

Oil Is the Market Driver

Oil is shaping equity outcomes more than domestic data right now.

During historical energy spikes, such as during the Arab Spring or the Russia-Ukraine war when oil pushed above $80, China equities have shown earnings resilience, with only modest forward revisions. The real adjustment has tended to come from multiple compression.

Winners in an Energy-Driven World (Defensive & Cash Flow)

From a portfolio construction perspective, energy shocks are less about reducing exposure and more about repositioning toward cash flow resilience and pricing power. In this environment, investors tend to rotate into sectors that can benefit from higher energy prices or effectively pass through rising costs, while maintaining balance sheet stability.

The focus shifts toward defensive earnings, domestic sectors, and policy alignment, rather than high-beta growth.

- Oil & shipping: Inventory gains and stronger pricing support names like China Shenhua, PetroChina, China Coal Energy, COSCO Shipping, and CNOOC.

- Renewables & power: Policy support intact for CGN Power, China Resources Power, and China Longyuan.

- Banks: Stability and state backing keep high quality names like Bank of China and China Merchants Bank in focus.

- Logistics: Pricing power helps JD Logistics pass through higher fuel costs.

But, Structural Growth Still in Play

Even in a volatile macro, long-term themes remain intact:

- Energy security: Policy-driven capex in EVs, storage, and grid infrastructure structurally supporting names such as BYD and Xpeng.

- AI and automation: State-backed investment continues to drive demand and stability of funding, with Horizon Robotics well positioned in this space.

- Selective consumption: Growth is concentrated in health and value-oriented segments, not broad discretionary recovery as consumer confidence remains subdued and ecommerce face competitive pressure.

Geopolitics: A Persistent Risk Premium

Ongoing tensions in the Middle East and US-China trade dynamics are adding a persistent risk premium to markets. Tariffs remain elevated, and while potential diplomatic meetings may support sentiment, expectations for meaningful breakthroughs remain low.

There’s also a broader strategic layer: if global conflicts shift bargaining power, trade tensions could re-intensify, particularly in key sectors like technology and industrials.

Investors should treat geopolitics as a structural overhang and expect headline volatility.

Investment Takeaway

From an investment perspective, a balanced approach makes sense: pairing structural growth areas like AI and energy transition with defensive, cash-generative sectors such as energy and banks. Oil remains the key signal for sector rotation, while policy support continues to act as a stabilizer during periods of volatility. Geopolitics may drive short-term swings, but fundamentals remain intact, making selectivity and positioning more important than outright market direction.

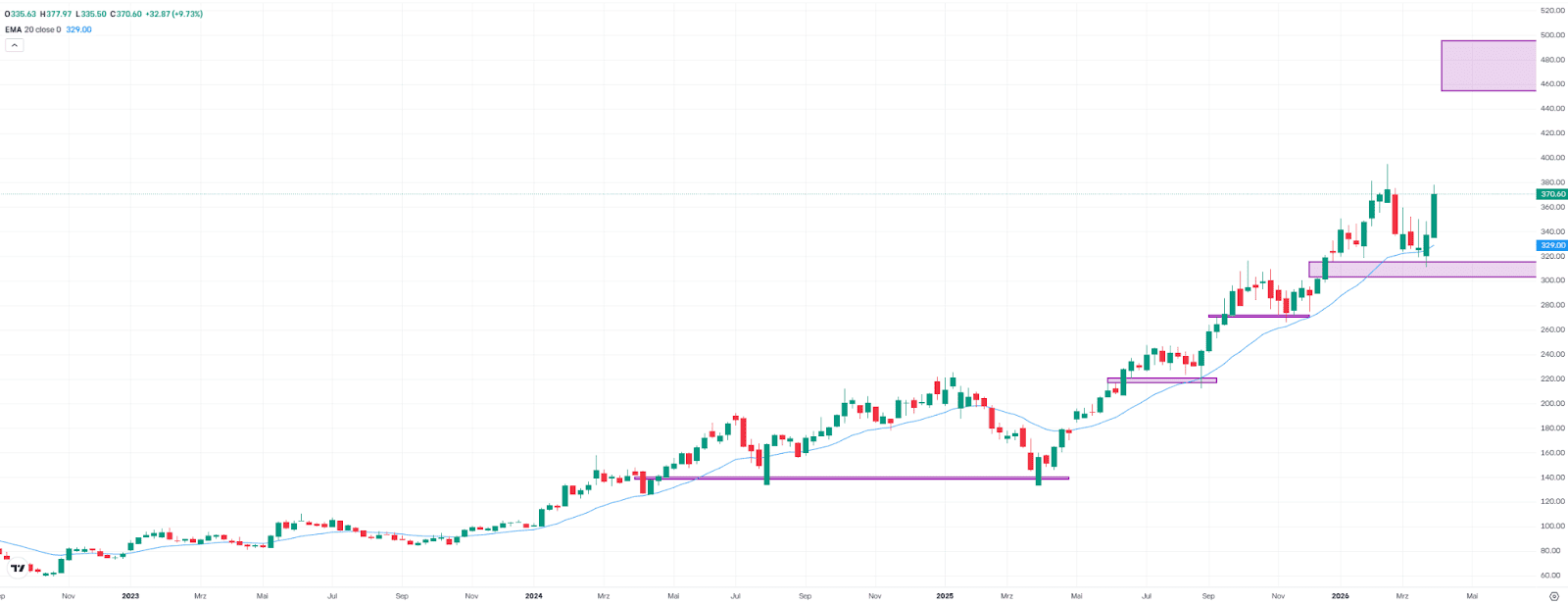

TSMC on the Verge of a Breakout? Record High Within Reach

TSMC shares closed last week 9.7% higher at $370.60, reducing the gap to the record high to around 6%. Just two weeks ago, that gap temporarily stood at 21%. Many investors appear to have viewed the rebound as a new entry opportunity, particularly after the fair value gap between $302.90 and $315.64 held successfully.

A test of the record high now seems within reach. Alongside developments in the Iran conflict, attention will turn to the upcoming quarterly results and guidance on Thursday. If an upside breakout occurs, a typical follow-through move of 15% to 25% could be possible. In a medium- to long-term scenario, the stock could therefore advance into the $455 to $497 range (see chart).

In the short term, however, the picture remains somewhat fragile. If sentiment deteriorates, there is room to the downside, especially after the recent sharp recovery. As long as the price does not fall sustainably below the 20-week moving average at $329 and break the mentioned support zone, buyers remain in control.

TSMC, weekly chart. Source: eToro

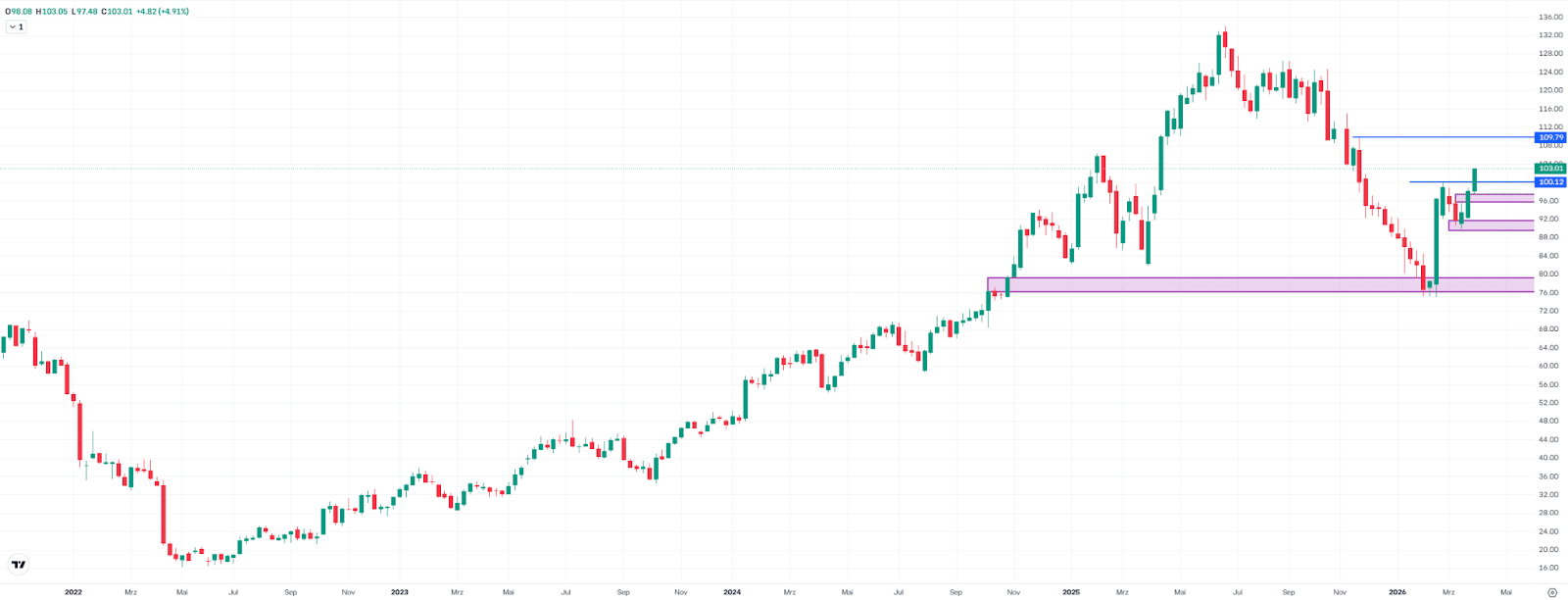

Netflix: Strong Rebound Meets Key Resistance

Netflix shares closed last week 4.9% higher at $103, reaching their highest level since early December. Since the February low, the stock has recovered by around 37%, after having dropped 44% in the preceding months. The total decline from the all-time high has thus been reduced to about 23%.

To further improve the medium-term chart outlook, a move above the high near $110 is needed. This level marked the starting point of the last major sell-off, so sellers are likely to defend it. The chances of a test look favorable, as the stock is approaching resistance with strong momentum.

Whether a breakout materializes or the move stalls will likely depend on the Q1 results and guidance, with an update expected on Thursday after the close. On the downside, the fair value gap between $95.84 and $92.48 would come into focus first. The key short-term support remains the March low at $89.75.

Netflix, weekly chart. Source: eToro

Patience over precisión

Bitcoin trades around $71.6K, but the key issue isn’t geopolitics, it’s that the structural signals that have defined every cycle bottom are still not in place. No clear supply crossover, no negative MVRV, and price remains well above key cost bases. Today, BTC is still far from the $54K aggregate cost basis and the deeper $39K on-chain level, zones where previous cycle lows have formed.

That suggests one possibility: the market may still need further adjustment before a true bottom is formed. Not a certainty, but a scenario investors should keep on the table.

At the same time, the underlying structure is improving. Long-term capital is accumulating, not exiting, and distribution is expanding through players like Morgan Stanley, pointing to a stronger foundation beneath the surface.

That’s the tension: the base may be forming, but it’s not validated.

For investors, this is less about precision and more about discipline. Maintaining exposure is reasonable. Forcing new risk is not. The edge comes from waiting until the data confirms it, until then, patience is a valid strategy.

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.