Analyst Weekly, February 22, 2026

The US Supreme Court ruled that the earlier use of emergency powers (IEEPA) to impose sweeping “reciprocal” tariffs was unlawful. Instead of backing down, the administration moved quickly, swapping legal tools and pushing the rate to the ceiling: less than 24 hours after announcing a 10% global tariff under a new legal authority, the US administration raised it to 15%, the maximum allowed under Section 122 of the 1974 Trade Act.

Section 122 allows the president to impose tariffs for up to 150 days without congressional approval. That makes this a short-term framework, but at the highest possible level under this statute. This acts as a bridge policy while longer-term authorities are pursued.

After the rate was lifted to 15%, the UK government, which had previously faced the lowest reciprocal tariff rate of 10%, said it expected its “privileged trading position” with the US to continue and would work with Washington to understand how the ruling affects tariffs going forward. That response underscores that country-level negotiations may now intensify.

Step Two: Section 301 & 232 Escalation

The administration plans to:

- Use Section 301 (unfair trade practices) for country-specific tariffs.

- Continue expanding Section 232 (national security) tariffs across sectors such as steel, autos, semiconductors, pharmaceuticals and critical minerals.

Section 301 probes require country-specific investigations and findings of trade violations before tariffs can be imposed. These measures could eventually replace the temporary 15% baseline rate with more targeted actions.

Autos are already back in focus. The administration is weighing 15% to 30% tariffs on foreign cars, which would directly affect global automakers and suppliers.

Investment & Market Implications: Policy continuity remains the central theme. Tariffs stay in place despite the legal setback and potentially broaden.

Notably, USMCA-compliant goods from Canada and Mexico remain exempt from the universal tariff for now. That keeps North American supply chains relatively insulated compared to Asia and Europe.

Markets now have two major themes to price in:

1) Legal uncertainty. The Supreme Court decision raises fresh questions about revenue already collected under the prior tariff regime. More than 1,500 companies had filed lawsuits in trade court ahead of the ruling. The Court did not clarify whether importers are entitled to refunds, leaving that issue to lower courts, creating potential exposure of up to $170 billion. While the President criticized the justices for not providing guidance, Treasury Secretary Scott Bessent said tariff revenue is expected to remain “virtually unchanged” in 2026 despite the ruling. The gap between legal uncertainty and fiscal expectations adds an ongoing policy overhang.

2) Political timing. The move comes just ahead of the State of the Union address, where trade policy is expected to feature prominently. Additional announcements, particularly around autos or China, could add further volatility.

For investors, that means staying alert to sector-level sensitivity. Autos, industrials, semiconductors, pharma, and global consumer names are likely to react to headlines. Companies with North American production footprints may be relatively better positioned, assuming USMCA exemptions hold.

Crypto’s Holding Pattern: Institutions Hesitate, Macro Dominates

The crypto market is not in euphoria. Nor is it in panic. It is in balance.

Bitcoin trades around $68,500 and ethereum near $2,050 after a correction that has been absorbed without structural disorder. Total market capitalization has stabilized, but flows tell a more nuanced story.

BTC spot ETFs recorded net weekly outflows (–$285M). There were attempts at inflows, but institutions are not accumulating with conviction yet. Ethereum, by contrast, shows relative resilience: +$78M net inflows this week, supported by staking yields and its ongoing technological narrative.

In derivatives, leverage remains moderate. Open interest has rebounded but is far from previous cycle excesses. Funding is neutral, volatility contained, and max pain levels aligned with current spot prices. There is no immediate technical pressure.

That reduces short-term systemic risk.

But the decisive factor is not technical, it is macro.

Correlation with the Nasdaq remains elevated. The Fed still sets the tempo. Without a clear expansion in global liquidity, risk multiples do not expand. The market consolidates rather than accelerates.

As things stand, the most probable scenario is range-bound price action: BTC between $65,000 and $72,000; ETH between $1,950 and $2,200 — absent a clear catalyst.

Institutionalization continues. Structural volatility declines. The industry matures.

But without liquidity, there is no new expansión leg. And today, more than narrative, balance sheets rule.

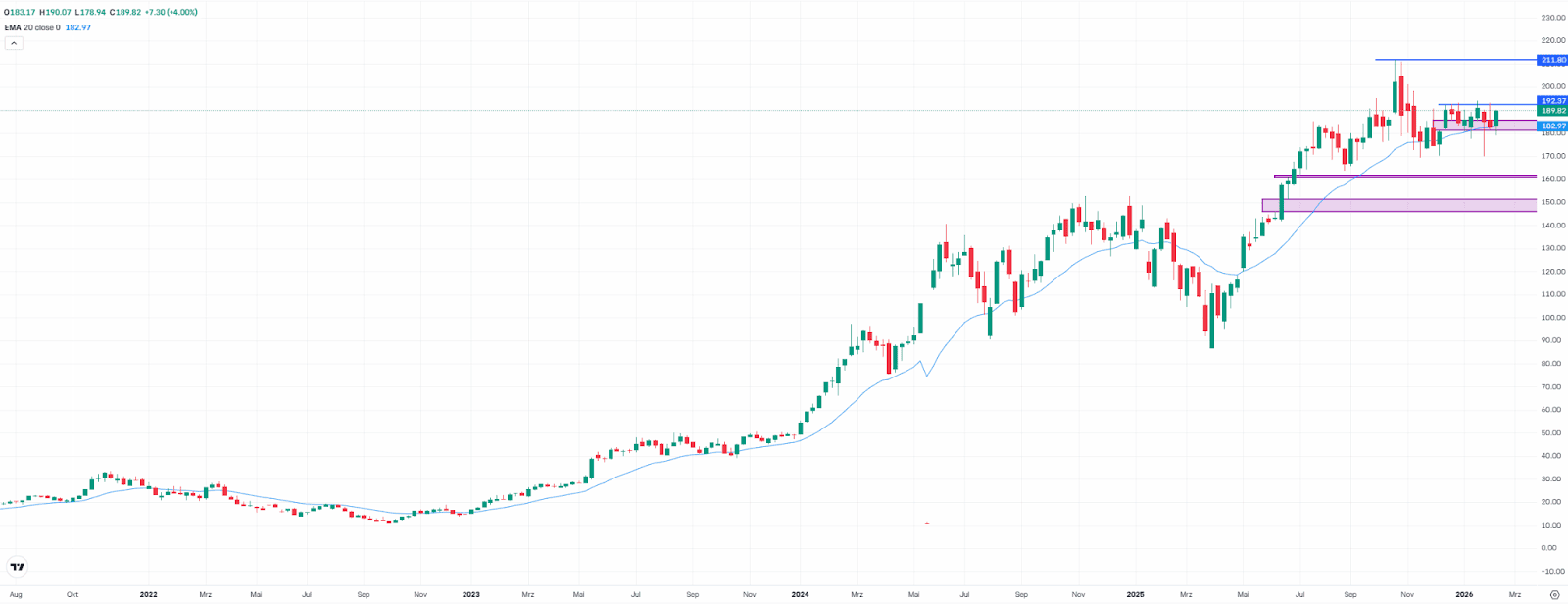

Sideways Phase at Nvidia: Is a Breakout Coming?

Nvidia shares rebounded by 4% last week to $189.82. However, since mid-December, the stock has been trading within a range.

The fair value gap between $180.78 and $185.67 has repeatedly prevented a sharper decline. Meanwhile, the high at $192.39 has repeatedly capped the upside.

From a technical perspective, the setup remains tense. Only a breakout to the upside or downside is likely to bring more momentum. If the stock breaks higher, it could approach its record high — currently about 10% away. A move above that level would confirm the long-term uptrend, which remains intact.

On the downside, the next stronger support (fair value gap) lies between $160.72 and $161.81. Below that, another support zone follows between $145.94 and $151.28.

Nvidia, weekly chart. Source: eToro

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.