The Daily Breakdown takes a deeper dive into Booking Holdings, shares of which have come under pressure so far in 2026.

Before we dive in, let’s make sure you’re set to receive The Daily Breakdown each morning. To keep getting our daily insights, all you need to do is log in to your eToro account.

Deep Dive

Booking Holdings runs online travel and dining reservation marketplaces, helping consumers search, compare, and book accommodations, flights, rental cars, and restaurant tables. Its major platforms include Booking.com, Priceline, Agoda, KAYAK, Rentalcars.com, and OpenTable.

The company recently reported its fourth-quarter results, but the stock did not react well to the news — falling 6.2% in the first session after the report. That’s despite the firm beating revenue expectations, reporting in-line earnings growth of 17%, announcing a 25-for-1 stock split, and showcasing 16% bookings growth.

While Booking Holdings has had a very successful run — up 74% over the last five years and up 211% in the last decade — the stock has struggled lately, now down more than 31% from its record high in July.

Future Growth Projections

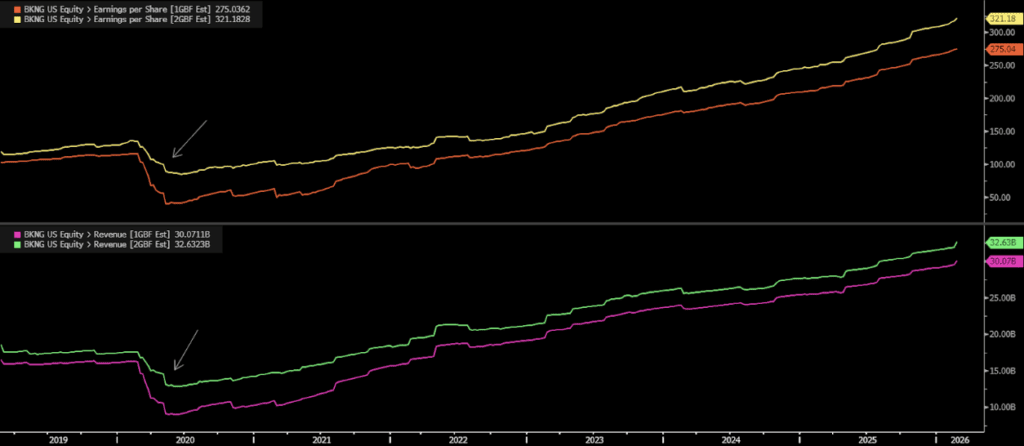

As the world continues to travel for business and pleasure, Booking keeps on growing. Notice the steadiness in the forward earnings and revenue expectations after the initial decline in 2020 due to COVID:

According to Bloomberg, analysts project the following:

- Earnings Growth: 17.8% in 2026, 17.2% in 2027, and 14.7% in 2028

- Revenue Growth: 10.4% in 2026, 8.8% in 2027, and 7.4% in 2028

Analysts currently have a consensus price target of ~$5,924 on BKNG stock — or about $237 post-split — implying about 49% upside to today’s stock price.

Want to receive these insights straight to your inbox?

Diving Deeper — Valuation

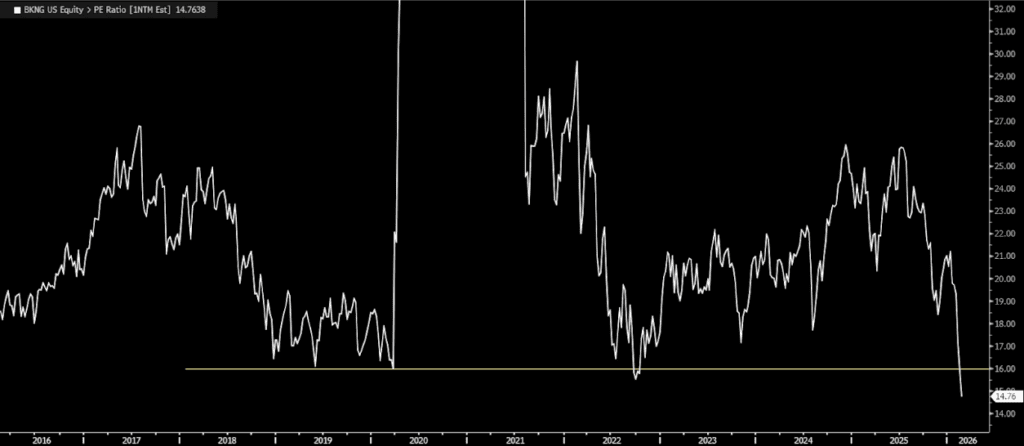

The current selloff in Booking Holdings has been intense, marking its largest decline since the 2022 bear market, where BKNG fell roughly 40%. As you can see on the chart below, the decline has brought the stock’s forward price-to-earnings ratio to its lowest level in the past decade.

Over the past few years, the 17-18x range has been supportive of the stock, although deeper declines have tested down in the 15-16x area. Now below this range, investors are wondering if it will again attract buyers or if they must prepare for the stock to garner a lower valuation for the foreseeable future.

Risks

Booking’s key risks are tied to cyclical demand and shifting distribution dynamics. A recession or consumer pullback can quickly pressure discretionary travel and lodging spend. Separately, ongoing worries about AI-driven disruption could keep the valuation discounted if investors believe generative search, AI travel agents, or platform changes at major traffic sources may weaken Booking’s customer acquisition advantages, raise paid marketing dependence, or compress margins — even if near-term fundamentals remain solid.

The Bottom Line

Booking continues to grow its earnings and revenue at a fairly healthy clip, while the latest selloff has brought its valuation down to historical trough levels. Some investors might view the recent volatility and possible valuation reset as too risky, while others may consider the selloff as an opportunity.

Disclaimer:

Please note that due to market volatility, some of the prices may have already been reached and scenarios played out.