The Daily Breakdown takes a closer look at Palo Alto Networks as shares have lost one-third of their value from the recent highs.

Before we dive in, let’s make sure you’re set to receive The Daily Breakdown each morning. To keep getting our daily insights, all you need to do is log in to your eToro account.

Deep Dive

We’ve spent a lot of time on the AI-driven selloff in software — and it’s now spilling into areas like credit card networks, rating agencies, and cybersecurity. The irony is that many bulls view AI as a catalyst for cybersecurity, not a threat. That’s not to say AI can’t introduce new risks, but it’s a reminder that Wall Street can be short-term and emotional. With that in mind, a fresh look at the charts pushed us to take a deeper dive into Palo Alto Networks.

Palo Alto Networks provides cybersecurity products and services globally, spanning next-gen firewalls, cloud security, secure access, and threat prevention/detection. It also sells subscriptions for threat intelligence, malware protection, and data loss prevention, alongside professional services, training, and support.

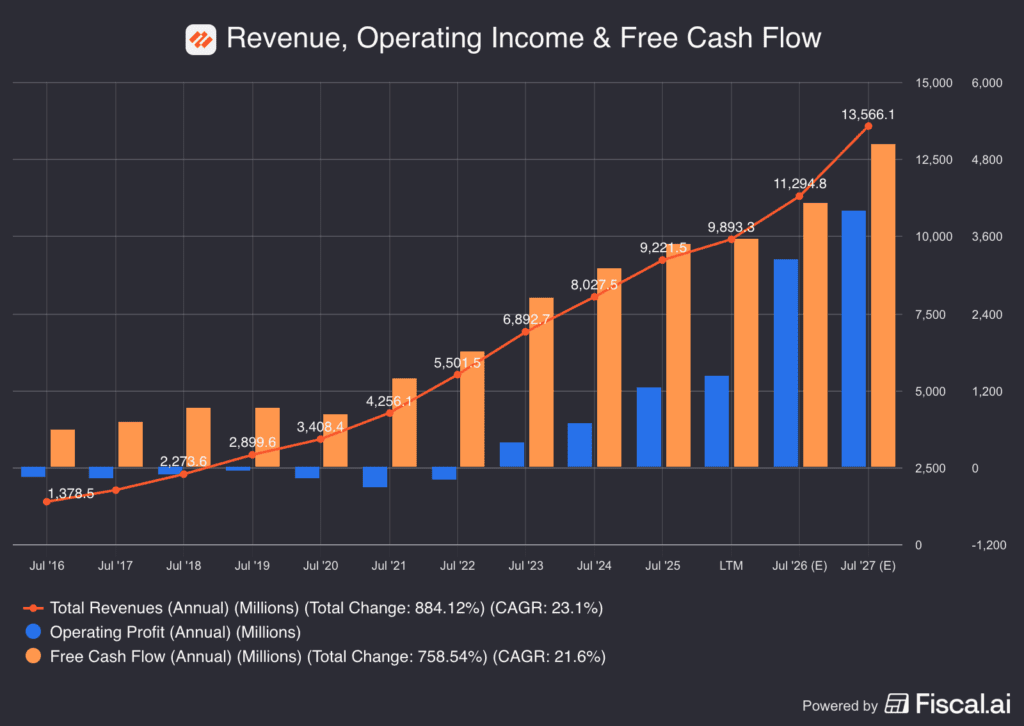

Often viewed as a blue-chip in the space, Palo Alto may not offer the same top-line growth as peers like CrowdStrike, Zscaler, or Fortinet, but it tends to bring stronger financials. The company is solidly profitable, generates consistent free cash flow, and has used that strength to invest for the long term. Most notably, it recently acquired CyberArk — a deal Palo Alto framed as a way to capitalize on key AI-driven trends.

Future Growth Projections

The company’s fiscal year ends in July (meaning fiscal 2026 ends on July 31, 2026). According to Bloomberg, analysts project the following:

- Earnings Growth: 10.8% in 2026, 7.8% in 2027, and 16.8% in 2028

- Revenue Growth: 22.2% in 2026, 19.8% in 2027, and 13.7% in 2028

- Free Cash Flow Growth: 17.4% in 2026, 23.2% in 2027, and 14.4% in 2028

Analysts currently have a consensus price target of ~$215 on PANW stock, implying about 44% upside to today’s stock price.

Want to receive these insights straight to your inbox?

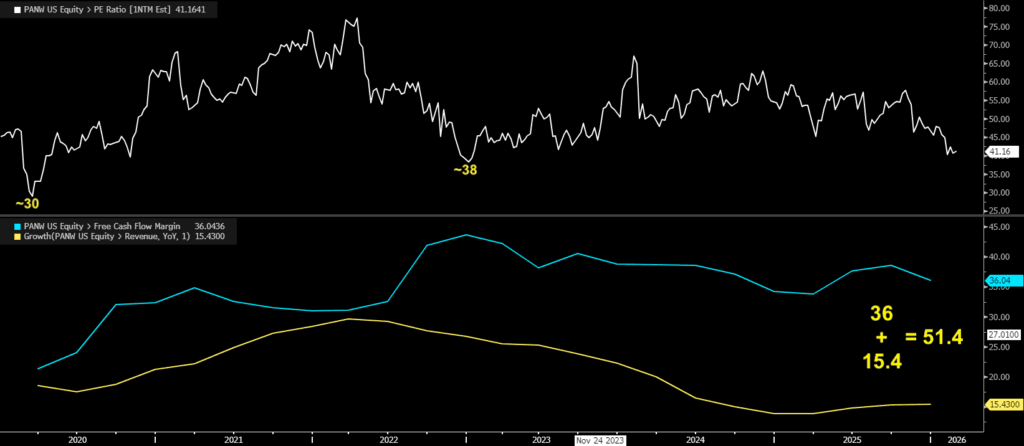

Diving Deeper — Valuation

With cybersecurity stocks often richly valued, that alone can be a hurdle for some investors. While Palo Alto doesn’t command the nosebleed multiples of some peers, it still trades at a premium to many more traditional industries.

The top chart shows PANW’s forward P/E ratio, which has fallen to its lowest level in several years. During the 2022 bear market, the multiple bottomed near 38x, while the COVID-19 selloff in 2020 pushed it down to roughly 30x.

The bottom chart highlights free cash flow margin and revenue growth. The “Rule of 40” — a key SaaS (Software as a Service) metric — says a company’s revenue growth rate plus its free cash flow margin should be at least 40%. Used by investors to evaluate company health, this formula balances rapid growth with profitability. By that measure, Palo Alto currently scores 51.4.

Risks

There are several risks for Palo Alto — and some have been on display recently. The biggest near-term overhang is AI-disruption fear; even if it proves overblown, the perception alone can pressure sentiment and the multiple. Beyond that, a broader tech selloff could weigh on shares, and intense competition could slow growth.

The Bottom Line

For some investors, the uncertainty is too high or the valuation still isn’t compelling. For others, the recent ~30% pullback may look like an attractive entry point to start building a position.

Disclaimer:

Please note that due to market volatility, some of the prices may have already been reached and scenarios played out.