Analyst Weekly, April 20, 2026

Markets got a bit of relief last week. Reports that the Strait of Hormuz will be opened sent oil sharply lower, with Brent dropping back toward below $90 (although recent news suggests that the situation in the region is still volatile).

Inventories are the real issue

Even if flows resume, we are not starting from a comfortable place.

- Recent disruption has already drained inventories

- Pre-conflict shipments have largely cleared

- Replacement supply has not fully arrived

Financial markets adjust fast. Unfortunately, physical supply doesn’t.

Even in a smooth reopening scenario:

- It takes weeks for production to ramp

- Longer for tankers to normalize

- Even longer for inventories to rebuild

Hence, prices can fall quickly, but supply tightness can linger.

At the peak of disruption, the global market was effectively short ~15 to 16 million barrels per day which is a massive gap.

If disruptions persist:

- Inventories could approach operational minimums

- Prices would likely spike again

- Demand destruction becomes the balancing mechanism

The US is relatively better insulated, but Europe and Asia are more exposed.

Investment Takeaway: Near-term risks have eased, with oil pulling back and growth data holding up, which supports a constructive backdrop for risk assets.Stability in energy prices, rather than further declines, will be needed to keep the current expansion on track. Market’s focus now shifts to whether improving sentiment is confirmed by data, particularly consumer activity and services momentum.

Q1’26 Banks Earnings Call Synthesis: What Matters

We reviewed Q1’26 earnings calls across Goldman Sachs, JPMorgan, Citi, Bank of America, Morgan Stanley,Wells Fargo, PNC, M&T, and BlackRock.

Stepping back from the noise, the message is fairly clear: the system is holding up better than sentiment suggests. Activity remains solid, credit is still clean, and several key earnings drivers have quietly turned positive. That gap between resilient data and cautious expectations is where the opportunity sits.

The economy is softer in surveys than in reality

Across JPMorgan, Bank of America, Goldman Sachs, and Wells Fargo, the read-through is consistent: clients are still active.

Spending, borrowing, and deal pipelines are not behaving as if a recession is imminent. Bank of America framed it best; there is a growing disconnect between weak confidence data and resilient transactional activity.

Investment Takeaway: This matters because markets tend to trade narratives. Banks operate on real flows. Near-term downside risk to earnings from a macro shock still looks limited.

Private credit: contained, but not irrelevant

There is a tendency in the market to frame private credit as either benign or systemic. The reality sits in between.

Banks are generally comfortable with their exposure, which is largely senior, structured, and relationship-driven. However, they are more cautious on the broader ecosystem, where underwriting standards are less consistent.

The risk is less about direct bank losses and more about second-order effects: liquidity, sentiment, and refinancing dynamics.

Regulation is shifting from headwind to tailwind

One of the more underappreciated developments is the evolving regulatory backdrop.

Potential adjustments to Basel III and capital frameworks are directionally supportive, with implications for:

- Lower capital requirements

- Higher buybacks

- Improved returns on equity

Investment Takeaway: Capital relief could become a meaningful medium-term earnings lever, particularly for lower-risk balance sheet models.

Credit remains benign but risk is building beneath the surface

Current credit metrics are, by most measures, still very strong:

- Low charge-offs

- Stable reserves

- Limited signs of stress

But management teams are increasingly aligned on the medium-term risk: the next credit cycle may be sharper than consensus expects.

The drivers are:

- Elevated rates for longer

- Refinancing pressure

- Pockets of looser underwriting (notably in private credit)

Investment Takeaway: Credit is not a current earnings issue, but it is the key variable for 2026-2027.

Revenue quality is improving, but unevenly

Net interest income is still supportive, but the drivers have evolved. It’s now more about asset mix, repricing, and deployment than simply rate direction.

The key distinction is that not all banks are equally positioned. The firms with diversified revenue streams are capturing more of the upside.

Investment Takeaway: This is a stock-picker’s environment, not a blanket sector trade.

Loan growth has inflected

One of the more important shifts this quarter is that loan growth is no longer hypothetical.

- Broad-based expansion at Bank of America

- Strong client-driven growth at Wells Fargo

- A three-year high in organic lending at PNC

Crucially, underwriting standards remain disciplined.

Investment Takeaway: If loan growth persists without margin compression, the sector is entering a positive operating leverage phase, which supports earnings revisions higher.

Investment takeaways

- Prefer diversified franchises: Banks with exposure to fees, markets, and wealth alongside lending are better positioned to navigate both resilience and volatility.

- Watch loan growth as the key signal: Sustained, broad-based lending growth would confirm a durable earnings upcycle.

- Treat credit as a lagging risk, not a current problem: Markets may be early in pricing a downturn that is not yet visible in the data.

- Focus on funding quality, not just growth: Deposit mix and client depth will increasingly separate winners from laggards.

- Don’t ignore capital optionality: Regulatory easing could unlock incremental returns via buybacks and balance sheet efficiency.

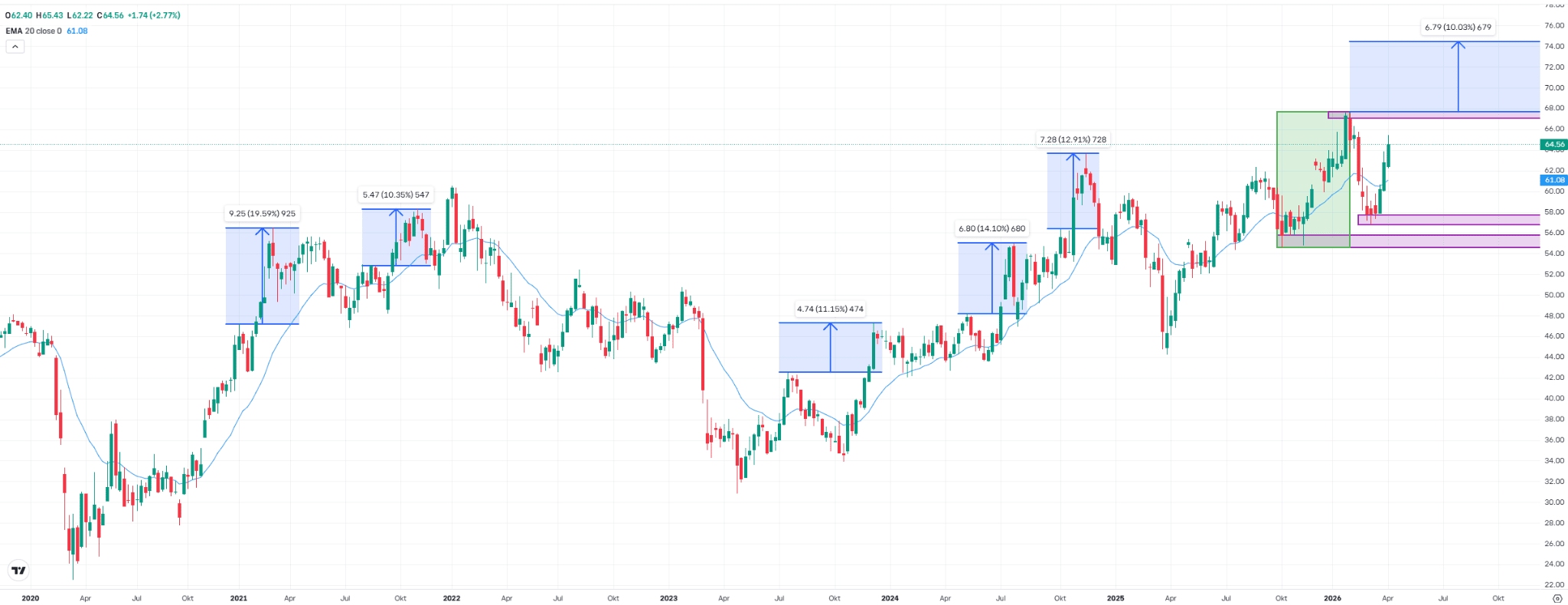

Third consecutive week of gains: Bank ETF approaches record high

The SPDR S&P Bank ETF (KBE) extended its recovery last week, marking its third straight week of gains. It rose by another 2.8% to $65.50. This has reduced the gap to the February record high of $67.60 to less than 5%. The reversal in recent weeks suggests the beginning of a new upward impulse in the broader picture, following a stronger corrective move.

From a technical standpoint, attention is now shifting to a potential breakout to the upside, which would confirm the long-term uptrend. In the past, such breakouts have often been followed by moves of 10% or more (see blue rectangles), implying upside potential toward the $74 area. In the event of short-term pullbacks, the 20-week moving average at $61.10 and the March low at $56.80 are likely to act as key support levels.

KBE, weekly chart. Source: eToro

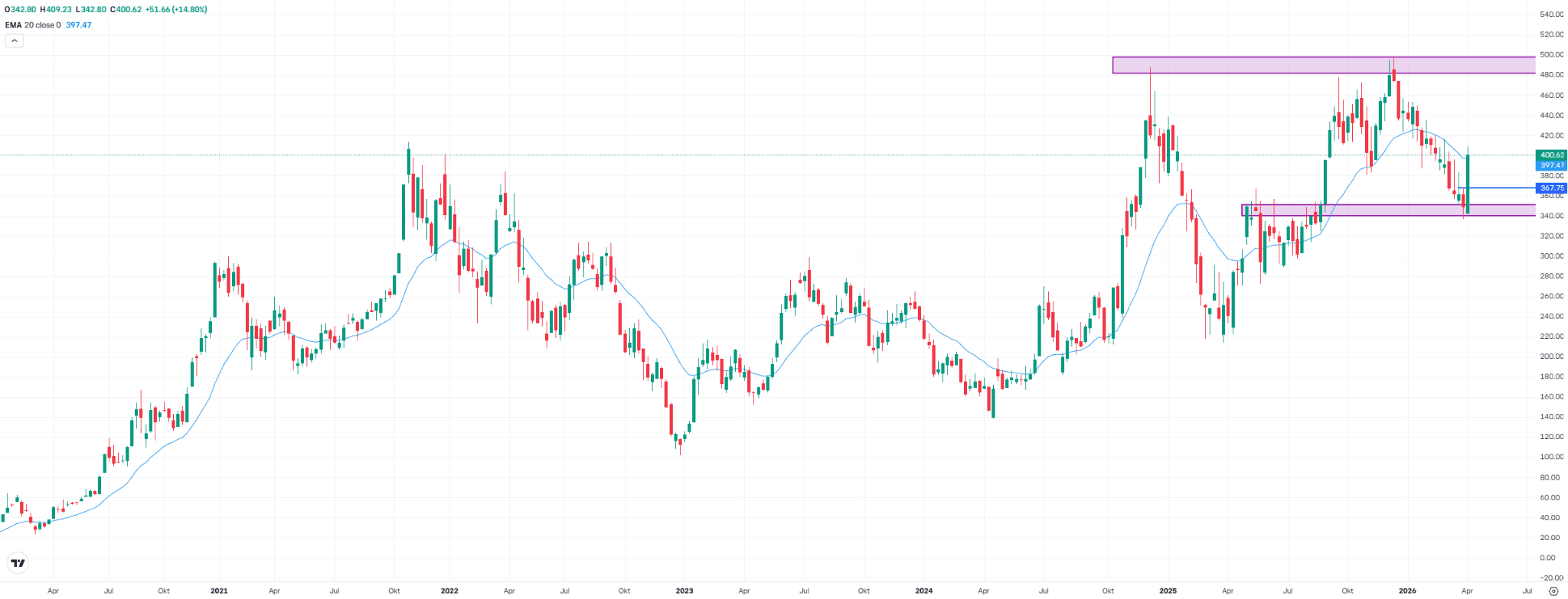

Tesla stock with a strong comeback: Is this the turning point?

Tesla shares rallied sharply last week, gaining 14.8% to close at $400.60 – the strongest weekly increase in nearly a year. From a technical perspective, this is notable. The former resistance zone between $340 and $350 (formed between May and September 2025) has now acted as support and served as a springboard for the recovery. In addition, both the high from two weeks ago at $367.80 and the 20-week moving average at $397.50 were broken to the upside.

This points to a potential turning point in the medium-term trend. Whether the move proves sustainable and the stock continues toward the December record high of $498, or first gives back some of its recent gains, will largely depend on the quarterly results due on Wednesday. The outlook will be key, particularly regarding the impact of the Iran conflict and persistently high oil prices.

Tesla, weekly chart. Source: eToro

Crypto: Squeeze Without Follow-Through

The market has begun the move, but has not yet completed it. Friday’s rally responded to mechanical logic rather than a structural shift: extreme short positioning, an external catalyst, and a technical breakout that forced massive liquidations. Nearly $600M in shorts were eliminated, but the system was not left clean.

Since then, price has lost continuity. Not from an absence of demand, but because the environment has reasserted itself. Geopolitics has reintroduced a binary component that displaces any market-driven narrative. In this regime, assets don’t anticipate: they react.

Even so, there are signals worth not ignoring. Institutional flow has been decisive at these moments, as shown by ETFs that recorded close to $1B in weekly inflows. This level of absorption validates that real demand exists on dips and during stress events. However, it is not yet consistent or aggressive enough to sustain a breakout.

In parallel, internal tensions are appearing. In the $76,500–$76,800 zone, on-chain data reflects distribution by long-term holders. The increase in exchange deposits suggests that part of the market is using the liquidity generated by the squeeze to unwind positions at break-even. It is, in essence, a market in unstable equilibrium: institutional demand absorbs, but structural supply limits.

Positioning remains the key element. The imbalance that triggered the move has not disappeared. Shorts persist that could fuel a second leg if the context cooperates. But that “if” no longer depends on the market.

Ethereum, meanwhile, is beginning to hint at relative strength. It is not yet a regime change, but it is an early signal. The narrative, tokenization, settlement infrastructure, remains intact, even if the price does not reflect it. Its opportunity remains a long-horizon one, not short-term.

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.